Impairment testing - Can market capitalisation be used to determine fair value less costs of disposal?

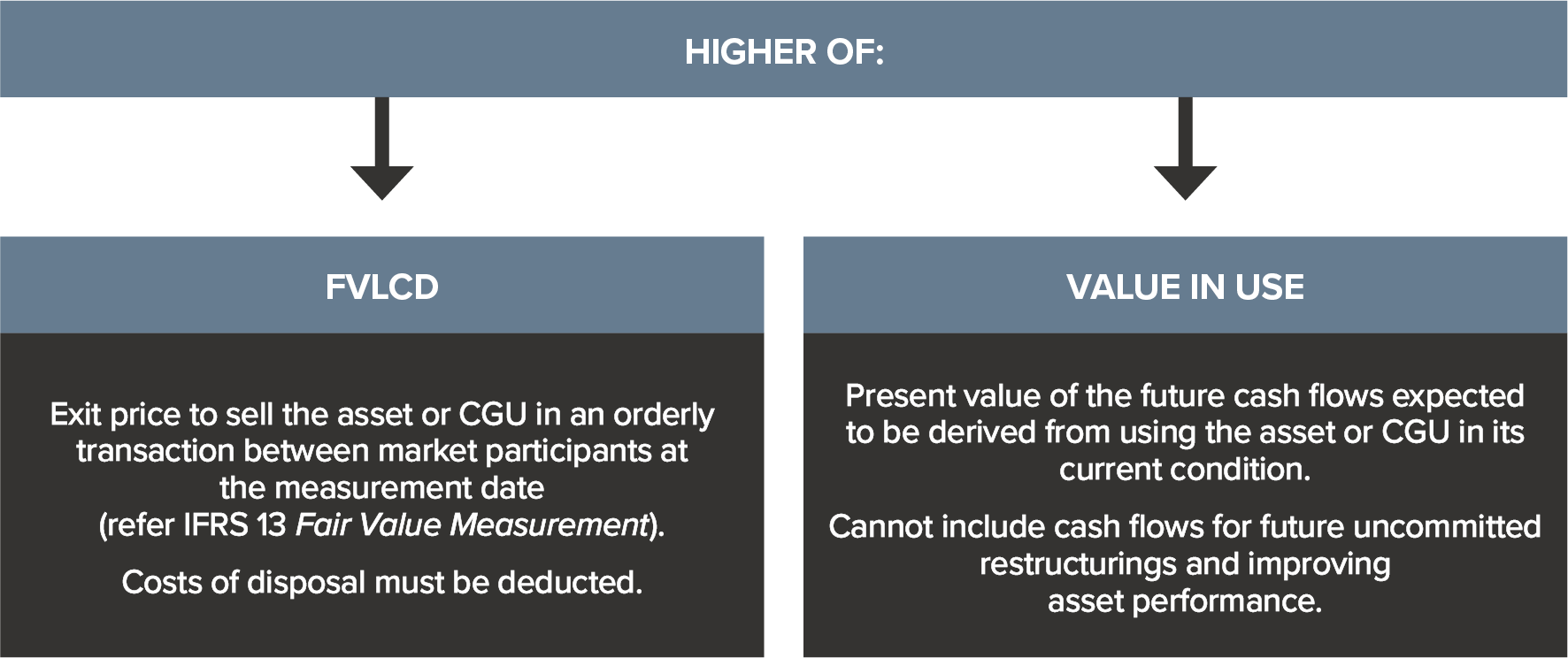

An asset or cash-generating unit (CGU) is impaired when its carrying amount exceeds its recoverable amount. Recoverable amount is the higher of the asset or CGU’s:

- Fair value less costs of disposal (FVLCD)

- Value in use.

Because of the restrictions imposed by IAS 36 on using certain cash flows in calculating value in use as noted above, some entities may prefer to determine and use FVLCD as ‘recoverable amount’. Determining FVLCD without an actual disposal event requires calculating a theoretical amount for FVLCD in accordance with IFRS 13.

Can market capitalisation be used to determine FVLCD?

No. It is not appropriate to use market capitalisation of a listed entity to determine FVLCD for impairment testing purposes. This applies even if the whole business of the entity comprises one CGU. Nevertheless, market capitalisation is an indicator of impairment.

- An entity’s market capitalisation will generally not represent an appropriate fair value estimate for its underlying business

- Transactions in a company’s shares as compared to a sale of the whole business would generally take place in different markets that have different market participant assumptions

- The market capitalisation of a company and the fair value of the underlying business can therefore differ significantly.

Listed entities must therefore still calculate either value in use, or FVLCD, using reasonable and supportable assumptions. Market capitalisation is just one data point in the recoverable amount analysis and can be used to calibrate (or compare to) the entity’s own FVLCD calculations (either using a discounted cash flow analysis, or external valuations).

More information

Please refer to our website for free access to BDO’s resources and publications to assist you when conducting your impairment tests of non-current assets. Alternatively, more in-depth eLearning materials are also available for purchase on our website.

Need help?

Please contact our IFRS & Corporate Reporting team if you require assistance conducting your impairment tests.