Two graphs to make you rethink higher savings interest rates

Two graphs to make you rethink higher savings interest rates

It’s easy to forget that as recently as April 2022, Australia’s cash rate target was 0.1 per cent. Most bank accounts paid no interest, and the best one-year term deposit returned less than one per cent. Even the Reserve Bank of Australia’s (RBA) Governor, Philip Lowe, issued a statement that the official cash rate would likely stay at 0.1 per cent until 2024 (as detailed in our previous article on inflation).

This environment was great for borrowers, as both individuals and businesses could leverage up their balance sheets for pennies on the dollar. However, it wasn’t so great for retirees relying on income from interest on cash deposits.

Fast forward to today and rates look attractive - even for a long-term investor - but how good are they really? Our analysis shows that purchasing power in cash or term deposits has fallen substantially in the last two years.

In this article, we look at why long-term investors should consider assets outside of cash to maintain and grow their capital base, using two simple graphs.

Setting the scene

It's been understandably easy for hesitant investors to sit on the sidelines of the market holding large amounts of cash, comfortably earning four to five per cent interest. However, the RBA’s June quarter print of six per cent Consumer Price Index (CPI) annualised reminds us that higher inflation erodes the purchasing power – or value - of money over time.

Because of this inflation effect, when savings account interest rates are lower than the inflation rate, the real value of your savings decreases.

So, should those hesitant investors be seeking higher returns elsewhere? Let’s take a closer look at why long-term investors should consider assets outside of cash to maintain and grow their capital base.

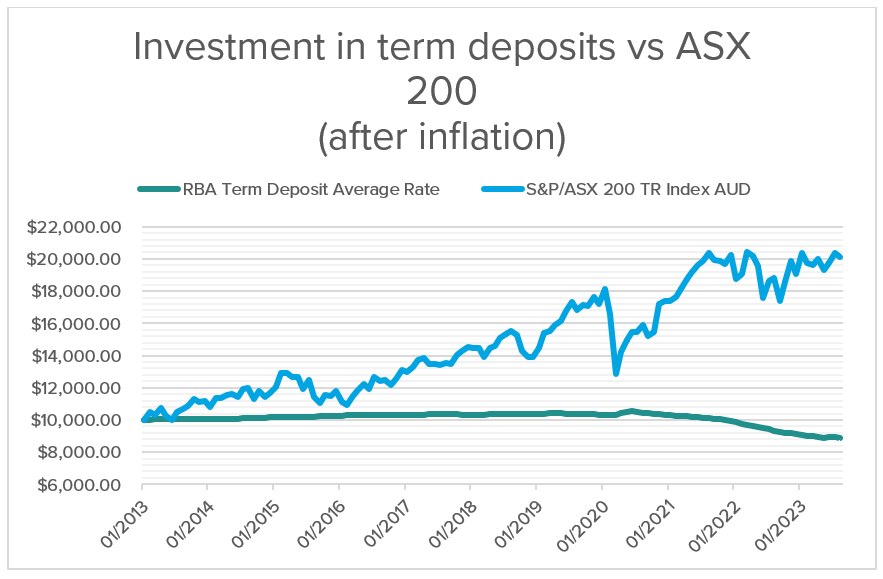

Graph 1: What would an investment of $10,000 have returned over the last ten years?

While today’s five per cent savings and term deposit rates might seem attractive, when we consider the erosion of purchasing power due to inflation and the long-term potential of investing in other asset classes - including Australian shares - the bigger picture is clear.

Comprised of the top 200 largest companies on the Australian Stock Exchange (ASX), the ASX 200 is typically used as a benchmark for investment returns. The graph below shows the journey of a $10,000 investment in the ASX 200 over the past ten years, compared to an average term deposit rate (reinvested). The effect of inflation has been subtracted to reflect ‘true’ returns.

Source: Lonsec

$10,000 invested in the ASX 200 over the last ten years will have returned over $10,000 on your original investment, or 101 per cent, even after accounting for inflation. Meanwhile, investing the same amount in term deposits will have left you $1000 worse off after accounting for inflation. It’s clear that that sticking to a long-term investment strategy in assets other than cash during this period has rewarded investors.

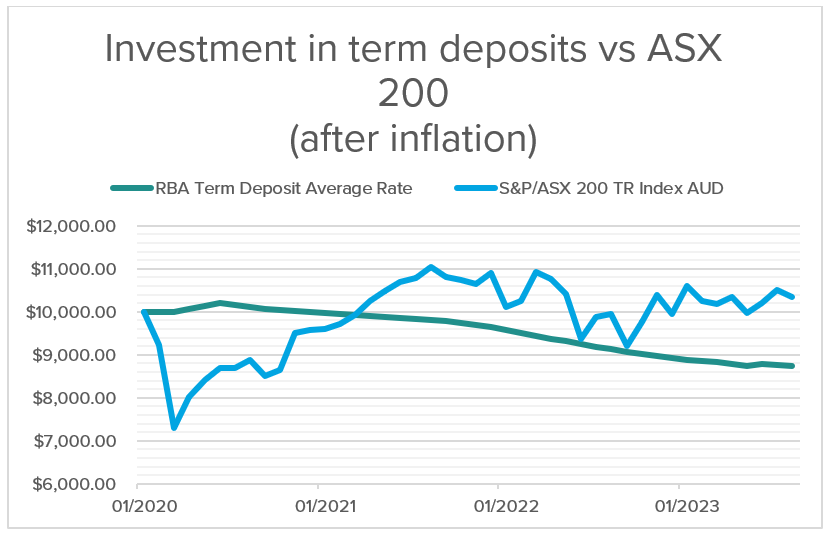

Graph 2: What about $10,000 over the short term, with higher interest rates?

In this version of the scenario, we again see the journey of the $10,000 investment in the ASX 200, compared to an average term deposit rate reinvested, with inflation subtracted to reflect true returns. However, this time we’re using a starting point of January 2020.

Source: Lonsec

Between January 2020 and September 2023, we can see that after inflation individual purchasing power has decreased by over $1,000 (or 12 per cent) had this been invested in term deposits. Meanwhile, an ASX 200 investment returned almost $350 (or 3.49 per cent) in the same period, also accounting for inflation.

For those who have shorter term needs for cash, such as for buying or renovating a home, a combination of term deposits and high interest accounts can be a great way to safely store and grow wealth while still having access when needed. However, there are clear downfalls to relying on term deposits and savings accounts - even when rates appear high - over the long term.

What to consider before investing

Be diligent about where you choose to put your money

Over the last 12 months, global inflation has risen to levels not seen for 40 years in most of the developed world. Some economists now believe a ‘regime shift’ has occurred in the dynamics of the market, which will no longer reward simply ‘buying the index’ or ‘buying low’ (or, buying low with the expectation of growth with little other thought). Moving forward, higher interest rates and increased market volatility will call for more discretion and less complacency among investors.

Ten years of relatively low rates has resulted in higher valuations of growth assets across the board, boosting returns. However, this now appears to be changing, meaning investors must be highly selective when it comes to investing, valuations of assets, and allocating funds.

Consider your personal risk appetite

It is a common investment maxim – ‘The more risk incurred, the higher the return’. However, return can be more or less important than risk to each individual investor - depending on many personal factors.

Asset allocation can account for up to 90 per cent of the performance of your investments. As we have seen, shares - while subject to short term volatility - generally achieve higher returns than cash and other typical ‘safe’ investments over the long term.

If an investor has short term needs for their cash, the reliance on a sum of money becomes more important, meaning the amount of risk they are able, or willing, to take on is lower. For example, if an individual is looking to purchase property, we would suggest leaving funds in a low-risk environment such as cash accounts or term deposits.

Alternatively, investors who are relying on income that can grow with or above inflation, such as those looking to grow their superannuation, should ensure they have a long-term investment strategy in place.

BDO Recommends

It is important to remember that this information is general in nature, and no two circumstances are the same.

When faced with concerns about your investments or superannuation, seek professional financial advice for your personal circumstances. For tailored support with decisions for your specific circumstances and help keeping on track through market highs and lows, reach out to your local BDO Private Wealth adviser.

This publication has been carefully prepared, but it has been written in general terms and should be seen as broad guidance only. The publication cannot be relied upon to cover specific situations and you should not act, or refrain from acting, upon the information contained therein without obtaining specific professional advice. Please contact the BDO member firms in Australia to discuss these matters in the context of your particular circumstances. BDO Australia Ltd and each BDO member firm in Australia, their partners and/or directors, employees and agents do not accept or assume any liability or duty of care for any loss arising from any action taken or not taken by anyone in reliance on the information in this publication or for any decision based on it.

BDO Private Wealth Advisers Pty Ltd ABN 62 805 149 677 AFS Licence No. 238280 is a member of a national association of separate member firms which are all members of BDO Australia Ltd ABN 77 050 110 275, an Australian company limited by guarantee. BDO Private Wealth Advisers Pty Ltd and BDO Australia Ltd are members of BDO International Ltd, a UK company limited by guarantee, and form part of the international BDO network of separate member firms. Liability limited by a scheme approved under Professional Standards Legislation.

BDO is the brand name for the BDO network and for each of the BDO member firms.

© 2023 BDO Private Wealth Advisers Pty Ltd. All rights reserved.