Effects of IFRS 9, 15 and 16 on business combinations occurring prior to effective dates of these new standards

In addition to the usual transition assessments preparers need to make with regard to the ‘triple threat’ new standards, thought is also required to determine the impact of these new standards, if any, on past business combinations accounted for under IFRS 3 Business Combinations, where ‘acquisition date’ for the combination was prior to the effective date of these standards (i.e. periods beginning on or after 1 January 2018 for the new revenue and financial instruments standards, and 1 January 2019 for the new leases standard).

While fair value is the default measurement basis for assets and liabilities acquired in a business combination in the scope of IFRS 3, certain exemptions exist which modify this requirement in certain cases. IFRS 3 was therefore amended in certain respects to address specific areas affected by the three new standards.

Impact of IFRS 9 Financial Instruments

The transitional provisions of IFRS 9 are comprehensive and address most issues that may arise relating to business combinations occurring prior to the effective date of IFRS 9. Please refer to BDO’s IFRS in Practice – IFRS 9 publication for further discussion of the transition provisions of IFRS 9.

Impact of IFRS 15 Revenue from Contracts with Customers

If an entity acquired a business prior to the effective date of IFRS 15, it would apply IFRS 3 to the transaction and recognise most assets and liabilities acquired at their fair values. In doing so, differences will arise between the carrying value of assets and liabilities and their fair values on acquisition. For example, the fair value of deferred revenue originally determined under IAS 18 Revenue (the predecessor standard to IFRS 15) would have been remeasured at fair value under IFRS 3.

If any contracts continued past the effective date of IFRS 15 (or the comparative period when the full retrospective approach is used), then the transitional provisions of IFRS 15 will be applied to such balances.

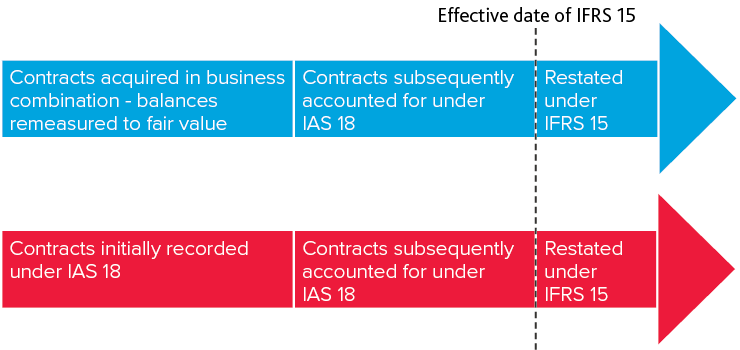

This process of multiple remeasurements to a contract can be illustrated as follows, with the acquirer’s steps in accounting for the contracts represented in blue, and the acquiree’s represented in red:

Assuming that both the acquirer and acquiree prepare IFRS compliant financial statements, then the entities may have to account for the contracts under three different bases over the contracts’ lives:

- Under IAS 18 in the records of the acquiree;

- Remeasured to fair value under IFRS 3 and then subsequently accounted for under IAS 18 in the records of the acquirer; and

- Under IFRS 15 in the records of both the acquiree and acquirer once IFRS 15 becomes effective.

The underlying calculations required to perform this restatement will differ from other contracts not previously acquired in a past business combination, therefore, such contracts will have to be segregated into discrete populations apart from other contracts. It may also be challenging to reconcile the consolidated financial statements.

Impact of IFRS 16 Leases - Off-market lease contracts acquired prior to effective date of IFRS 16

Old treatment

Under IFRS 3, favourable operating lease contracts were recognised as distinct intangible assets (or liabilities for unfavourable leases) in a business combination because the underlying lease contract was not recognised ‘on balance sheet’ prior to IFRS 16.

| Type of lease | Examples |

|---|---|

| Favourable lease (intangible asset) |

|

| Unfavourable leases (liability) |

|

New treatment under IFRS 16

The transitional provisions of IFRS 16 (paragraph C19) require any asset or liability relating to favourable or unfavourable lease terms for an operating lease acquired in a business combination to be derecognised and adjusted to the carrying value of the associated right-of-use asset.

This is consistent with the ongoing requirement in IFRS 3, paragraph 28B, to adjust the right-of-use asset at acquisition date for the effect of favourable or unfavourable terms of leases when compared with market terms.

Next month

Please look out in next month’s Accounting News for the effects of IFRS 9, 15 and 16 on business combinations occurring after the effective dates of these new standards.