Step Five – Recognising revenue under IFRS 15 – It’s all about timing

IFRS 15 Revenue from Contracts with Customers (IFRS 15) introduces a five-step revenue recognition model as follows:

| Step 1 | Identify the contract(s) with the customer | |

| Step 2 | Identify the performance obligations in the contract | |

| Step 3 | Determine the transaction price | |

| Step 4 | Allocate the transaction price to the performance obligations | |

| Step 5 | Recognise revenue when a performance obligation is satisfied |

Since then we have published a number of articles on IFRS 15 that cover various issues from the five-step process in greater depth:

| Step | Edition… | |

| Step 1 | Identify the contract(s) with the customer | May and June 2018 |

| Step 2 | Identify the performance obligations in the contract | July and September 2018 |

| Step 3 | Determine the transaction price | November 2018, February 2019, March 2019 and May 2019 |

| Step 4 | Allocate the transaction price to the performance obligations | June and July 2019 |

In this edition, we start our examination of the final step in the five-step process – recognising revenue when a performance obligation is satisfied.

Recognising revenue

Under IFRS 15, revenue is recognised when (or as) a performance obligation is satisfied by transferring a promised good or service (i.e. an asset) to a customer. Transfer occurs when, or as, the customer obtains control of the good or service.

‘Control’ of the good or service (asset) is the ability of an entity to:

- Direct the use of the asset

- Obtain substantially all of the remaining benefits from the asset (e.g. by using the asset to produce goods or provide services, to enhance the value of other assets, or being able to sell the asset or pledge it as security for a loan), and

- Prevent others from directing the use of, and obtaining the benefits from, the asset.

A performance obligation may be satisfied:

- At a point in time, or

- Over time.

Over time

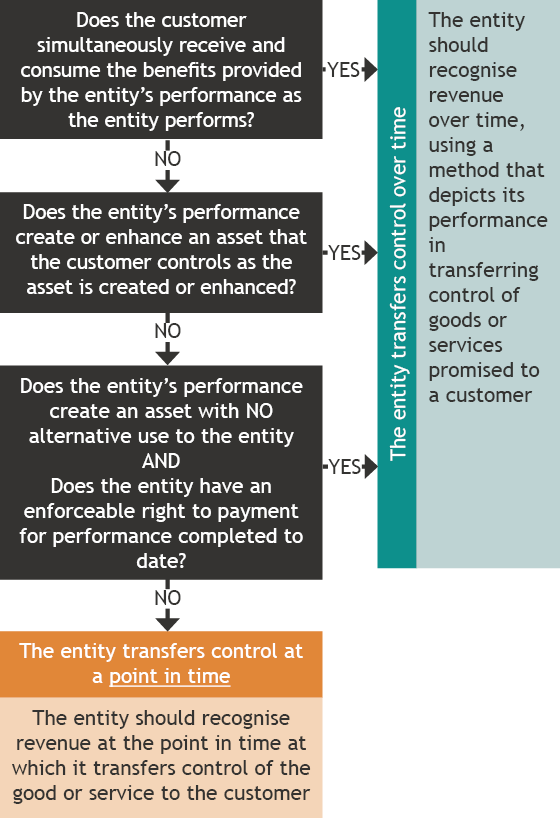

IFRS 15, paragraph 35 contains the requirements for recognising revenue over time. An entity transfers control of a good or service over time and, therefore, satisfies a performance obligation and recognises revenue over time, only if at least one of the following criteria is met:

- The customer simultaneously receives and consumes the benefits provided by the entity’s performance as the entity performs (this would occur, for example, in relation to the provision of nightly office cleaning services)

- The entity’s performance creates or enhances an asset (for example, work-in-progress) that the customer controls as the asset is created or enhanced, or

- The entity’s performance does not create an asset with an alternative use to the entity and the entity has an enforceable right to payment for performance completed to date.

| Customer simultaneously receives and consumes benefits | OR | Customer controls asset as it is created or enhanced | OR | Asset created has no ‘alternate use’ to entity AND entity has enforceable right to payment |

With respect to the third criterion above, an asset created does not have an alternative use to an entity if the entity is:

- Contractually restricted from directing the asset for another use during its creation or enhancement, or

- Practically limited from readily directing the completed asset for another use.

An ‘enforceable right to payment for performance completed to date’ requires the entity to be entitled to an amount that at least compensates the entity for performance completed to date if the contract is terminated by the customer or another party for reasons other than the entity’s failure to perform as promised. Such amount would approximate the selling price of the goods or services transferred to date (for example, recovery of the costs incurred by an entity in satisfying the performance obligation plus a reasonable profit margin), rather than compensation for only the entity’s potential loss of profit if the contract were to be terminated.

In Australia, what constitutes an ‘enforceable right to payment for performance completed to date’ is not an easy question to answer. Each contract must be considered on its merits having regard to both the terms and conditions of the contract and any relevant statute and the common law.

For the purpose of paragraph 35(c), the contract must contain a formula for providing compensation for performance completed to date and provide for the recovery of a reasonable proportion of the entity’s expected profit margin or a reasonable return on the entity’s cost of capital. If the contract excludes the right to recover a proportion of the lost profit or return on capital (which the contract might do if it contains a clause excluding ‘consequential loss’), is silent on those matters or there is no written contract, then the principal remedy for any loss suffered as a result of an early termination is damages (the amount of which may also be adjusted to take account of any loss mitigation steps that need to be taken), which in most instances will not constitute an ‘enforceable right to payment for performance completed to date’.

In short, if your contracts do not specify that compensation is required for performance completed to date where there is an early termination, it is unlikely they would meet the ‘over time’ revenue recognition criteria in paragraph 35.

Point in time

If a performance obligation is not satisfied over time, an entity satisfies the performance obligation at a point in time.

To determine the point in time at which a customer obtains control of a promised asset and the entity satisfies a performance obligation, the entity must consider the indicators of the transfer of control, which include, but are not limited to:

- The entity has a present right to payment for the asset

- The customer has legal title to the asset

- The entity has transferred physical possession of the asset to the customer

- The customer has the significant risks and rewards of ownership of the asset

- The customer has accepted the asset.

The requirements for the recognition of revenue are best illustrated in the decision tree below:

Methods for recognising revenue over time

Where a performance obligation is satisfied over time, a method for measuring progress towards satisfaction of the performance obligation must be used. Appropriate methods of measuring progress include:

- Output methods – these recognise revenue on the basis of direct measurements of the value to the customer of the goods or services transferred to date relative to the remaining goods or services promised under the contract

- Input methods – these recognise revenue on the basis of the entity’s efforts or inputs to the satisfaction of a performance obligation (for example, resources consumed, labour hours expended, costs incurred, time elapsed or machine hours used) relative to the total expected inputs to the satisfaction of that performance obligation.

Example of output methods include surveys or appraisals of results achieved, milestones reached, time elapsed and units produced/delivered. The output method selected should faithfully depict the entity’s performance towards complete satisfaction of the performance condition.

In future editions of Accounting News we will look at some examples of the timing of revenue recognition.

Concluding thoughts

Under IAS 18 Revenue, revenue recognition was comparatively straightforward. When goods were being sold, revenue was recognised when the risks and rewards of those goods passed to the purchaser (which was frequently when legal tile passed) and when services were being sold, revenue was recognised on a percentage of completion basis.

Under IFRS 15, revenue can only be recognised over time if the strict criteria are met. A determination of whether those criteria have been met will often involve an in-depth examination of the terms of contracts that have been entered into with customers. As we have seen with all of the five steps in the IFRS 15 revenue recognition model, this will require finance teams to work with sales (and in some instances legal) teams to ensure that they have a sufficiently in-depth understanding of contractual terms to correctly identify when revenue should be recognised.