How to recognise income when NFPs receive a grant to acquire or construct a non-financial asset?

Preparers of financial statements for not-for-profit entities (NFPs) should, by now, be aware of the new income recognition requirements of AASB 1058 Income of Not-for-Profit Entities. Except for its deferral in limited circumstances for research grants until 30 June 2020 (see December 2019 article), AASB 1058 applies to all NFPs for annual periods beginning on or after 1 January 2019.

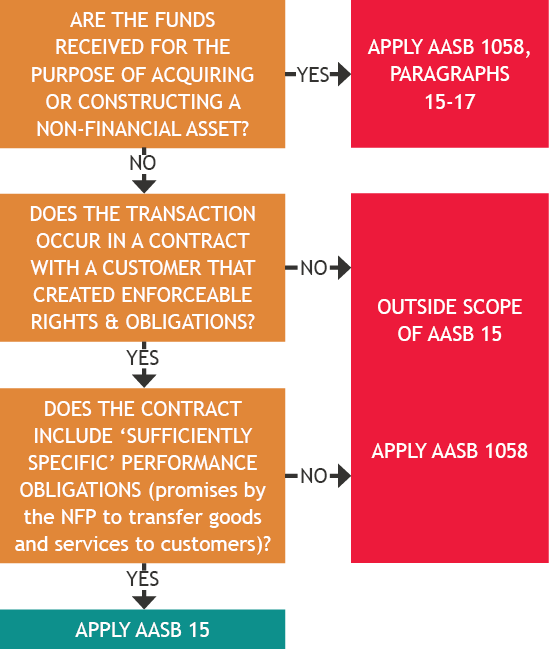

During 2019, our Accounting News articles focused on the second and third steps shown in the diagram below, which require analysis of the terms of grant contracts to assess whether income is recognised under AASB 15 Revenue from Contracts with Customers, or AASB 1058.

This month we focus on the very first step in the diagram, i.e. how to account for a grant received to acquire or construct a non-financial asset.

Many NFPs may previously have automatically deferred capital grants and recognised income only in periods during which the related depreciation is recognised (i.e. matched income and expenses).

It is important to note that while paragraphs 15-17 enable NFPs to defer the initial receipt of capital grants in certain circumstances, these provisions do not permit ‘matching’ of income with related expenses, and this could have a significant impact on profit or loss in future.

We strongly recommend that management assess all capital grant contracts as a matter of urgency in order to determine whether transition adjustments will be required on first time adoption of AASB 1058.

When answering the question in the first step above, we refer to paragraphs 15 to 17 of AASB 1058.

AASB 1058, paragraph 15 requires the following:

A transfer of a financial asset to enable an entity to acquire or construct a recognisable non-financial asset that is to be controlled by the entity is one that:

- Requires the entity to use that financial asset to acquire or construct a recognisable non-financial asset to identified specifications;

- Does not require the entity to transfer the non-financial asset to the transferor or other parties; and

- Occurs under an enforceable agreement.

Where these criteria are met, the NFP recognises the receipt (cash) initially as a liability, which is transferred to income when (or as) the NFP satisfies its obligation to build the non-financial asset (refer paragraph 16 below).

An entity shall recognise a liability for the excess of the initial carrying amount of a financial asset received in a transfer to enable the entity to acquire or construct a recognisable non-financial asset that is to be controlled by the entity over any related amounts recognised in accordance with paragraph 9. The entity shall recognise income in profit or loss when (or as) the entity satisfies its obligations under the transfer.

AASB 1058, paragraph 16It is a real ‘privilege’ to be able to apply paragraphs 15-17 because grants for this purpose will automatically be ‘deferred’. It is therefore important to ensure that all criteria in paragraph 15 have been met, including that:

- The funds received are for the acquisition or construction of a recognisable non-financial asset

- The asset will be controlled by the entity once acquired or construction is complete, and the NFP is not required to transfer the asset to anyone else

- There are agreed specifications for the non-financial asset, and

- The grant agreement is enforceable.

Example 1 – Recognisable non-financial asset

Charity J received a $1,000,000 grant on 1 December 2019 to develop a new website. The grant was from an unrelated donor.

Charity J will commence development of the website on 1 February 2020, and it is expected to be completed and ready to ‘go live’ on 31 December 2020.

Charity J has hired a team of software engineers (with significant experience in website development) to develop the website. Development costs are expected to be $1,200,000.

The website will provide information to existing donors on all projects being run by Charity J.

The terms of the agreement state:

- Charity J must use the funds to develop a new website

- Charity J will control the website after development

- Any grant monies that are not spent on website development are required to be refunded the donor at the conclusion of the development phase.

Charity J has a 31 December year-end.

Analysis

Charity J accounts for the $1,000,000 cash received as a financial asset on 1 December 2019 in accordance with AASB 9 Financial Instruments.

In determining whether the ‘credit side’ of the entry can be deferred and recognised under AASB 1058, paragraphs 15-17, we firstly need to be satisfied that all criteria in paragraph 15 have been met:

Paragraph 15 requirement | Condition met |

The funds received are for the acquisition or construction of a recognisable non-financial asset. | No. While the donor agreement requires a new website to be developed, these development costs cannot be capitalised in accordance with AASB 138 Intangible Assets because the website development costs do not meet the criteria in AASB 138, paragraph 57(d) to be capitalised as an intangible asset. Charity J is unable to demonstrate how the website will be capable of generating future economic benefits (i.e. revenue). Therefore the criteria in AASB 138.57(d) cannot be met. Also refer to AASB Interpretation 132 Intangible Assets – Web Site Costs |

The asset will be controlled by the entity once acquired or construction is complete, and the NFP is not required to transfer the asset to anyone else. | Yes. Charity J will control the website after development. |

There are agreed specifications for the non-financial asset. | Yes. The website will provide information to existing donors on all projects being run by Charity J. |

The grant agreement is enforceable. | Yes. Any grant monies that are not spent on website development are required to be refunded the donor at the conclusion of the development phase. |

As not all criteria in paragraph 15 have been met, Charity J recognises the $1 million donation on 1 December 2019 as income in accordance with paragraph 10 of AASB 1058 as follows:

| Dr ($) | Cr ($) | |

| Cash | 1,000,000 | |

| Income | 1,000,000 |

Website development costs would then be expensed during the development period from 1 February 2020 to 31 December 2020 as follows:

| Dr ($) | Cr ($) | |

Website development costs (P/L expense) | 1,200,000 | |

Cash | 1,200,000 |

Example 2 - Recognisable non-financial asset

Same facts as Example 1 above, except that the website will also include functionality for new and existing donors to donate money to both new and existing projects.

Analysis

Charity J accounts for the $1,000,000 cash received as a financial asset on 1 December 2019 in accordance with AASB 9.

In Example 1, we concluded that:

- Charity J will control the website after development

- There are agreed specifications for the website, and

- The grant agreement is enforceable.

As these facts have not changed, we simply need to reassess whether the funds received for the website development will result in a non-financial asset being recognised on Charity J’s balance sheet.

Paragraph 15 requirement | Condition met |

The funds received are for the acquisition or construction of a recognisable non-financial asset. | Yes. The donor agreement requires that the cash transferred to Charity J must be used to develop a new website. In this fact pattern, the development costs are capitalised because they meet the criteria in paragraph 57 of AASB 138 to be capitalised as an intangible asset. That is, Charity J can demonstrate the following:

|

As all criteria in paragraph 15 have been met, Charity J recognises the $1 million donation on 1 December 2019 as a liability as follows:

| Dr ($) | Cr ($) | |

| Cash | 1,000,000 | |

| Liability | 1,000,000 |

Website development costs will then be capitalised during the development period from 1 February 2020 to 31 December 2020 as follows:

| Dr ($) | Cr ($) | |

| Website development costs (intangible asset) | 1,200,000 | |

| Cash | 1,200,000 |

Charity J then recognises the liability as income as the website development takes place (during financial year ended 31 December 2020):

| Dr ($) | Cr ($) | |

| Liability | 1,000,000 | |

| Income | 1,000,000 |

Example 3 – Asset to be controlled by the entity

Kids Club, a private NFP company that is limited by guarantee, runs out of school hours’ programs and activities.

On 1 July 2019, Kids Club received a $20,000,000 cash grant from the Government to construct a state of the art building so Kids Club can run art classes, woodworking classes, music lessons and drama classes.

Question:

Assume that the grant agreement is enforceable, that the building is a recognisable non-financial asset under AASB 116 Property, Plant and Equipment, and that the building will be built to detailed, agreed specifications.

Does Kids Club control the building once development is complete if the building is constructed on:

Land…. | Control? |

Owned by Kids Club | Yes. Kids Club will control the building once completed because it owns the land upon which the building is constructed. |

Leased by Kids Club from the Local Council under a 50-year peppercorn lease (Assume useful life of building is 40 years) | Yes. Kids Club will control the building once completed because the building is constructed on land leased for 50 years by Kids Club. The building will be recognised as a leasehold improvement under AASB 116. |

Leased by Kids Club from the Local Council under a 20-year peppercorn lease (Assume useful life of building is 40 years) | Yes. Even though Kids Club does not have a lease over the land upon which the building is constructed for the full 40 year useful life of the building, Kids Club will nevertheless control the land for a period of 20 years through its right-of-use asset (land). If there are no options to extend the lease beyond 20 years, the building will be amortised over a period of 20 years rather than 40 years. |

Leased by Kids Club from the Local Council under a rolling 3-month peppercorn lease (Assume useful life of building is 40 years) | Yes. Considering the recent IFRIC agenda decision regarding lease term for cancellable leases (where there is no initial term), Kids Club would incur a significant penalty if it decided to terminate the lease after 3 months. Given the useful life of the building for 40 years, and a $20 million carrying value of leasehold improvements, AASB 16, paragraph B34 would point to an enforceable agreement and a lease term that is likely to be close to 40 years. |