Expect to see a reduction in the amount of accounting policy disclosures

For annual reporting periods beginning on or after 1 January 2023, we expect to see a significant reduction in the amount of accounting policy disclosures in financial statements.

What’s changed?

In future, only ‘material accounting policy information’ must be disclosed. Currently IAS 1 requires disclosure of ‘significant’ accounting policies, but the term ‘significant’ is not defined in IFRS and the IASB decided that it was easier to use the term ‘material’ because it is already defined in IFRS and IFRS Practice Statement 2 provides guidance on assessing materiality.

What is ‘material accounting policy information’?

Accounting policy information is only material if, when considered together with other information included in an entity’s financial statements, it can reasonably be expected to influence decisions that the primary users of general purpose financial statements make on the basis of those financial statements.

Immaterial accounting policy information need not be disclosed

The amendments to IAS 1 clarify that:

- Accounting policy information relating to immaterial transactions, other events or conditions need not be disclosed because it is ‘immaterial’.

- Accounting policy information relating to material transactions, other events or conditions may not always be material.

However, accounting policy information may be material even if it relates to transactions, other events or conditions that are quantitatively immaterial (i.e. small in dollar terms).

When is accounting policy information expected to be material?

As noted above, if an entity has material transactions, it does not necessarily follow that an accounting policy should be disclosed.

Accounting policy information is expected to be material if users of an entity’s financial statements would need it to understand other material information in the financial statements.

Extract of IAS 1, paragraph 117B

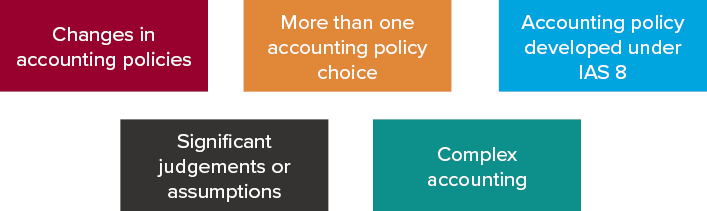

For example, accounting policy information is likely to be material if the information relates to material transactions, other events or conditions, and:

- The entity changed its accounting policy during the period, resulting in a material change to information reported in the financial statements

- The entity chose the accounting policy from one or more options permitted under IFRS (e.g. measuring investment property at historical cost or fair value)

- The accounting policy was developed applying the hierarchy in IAS 8 Accounting Policies, Changes in Accounting Estimates and Errors because there is no specific IFRS dealing with the transaction

- The entity was required to make significant judgements or assumptions in applying the accounting policy, and these judgements or assumptions have been disclosed as required by IAS 1, paragraphs 122 or 125, or

- The accounting is complex and users would otherwise not understand the material transaction (for example, if more than one IFRS standard applies to the transaction).

Figure 1: factors to consider when assessing whether accounting policy information is material.

No more ‘boilerplate’ accounting policies – Entity-specific information to be disclosed

The amendments specifically note that accounting policy information which focusses on how an entity has applied IFRS to its own circumstances provides entity-specific information that is more useful to users than standardised (boilerplate) information that merely duplicates or summarises what has already been said in IFRS.

If an accounting policy is immaterial, does that mean other IFRS disclosures for the transaction are also immaterial?

No. While a transaction or balance may be quantitatively material, the related accounting policy information may be considered immaterial because none of the factors in Figure 1 above were present. However, other related IFRS disclosures are still required.

Example

All entities account for income taxes in the same way under IAS 12 Income Taxes because IAS 12 contains no accounting policy choices. The accounting policy information may therefore be considered immaterial. However, if income tax expense, and deferred tax assets and deferred tax liabilities are quantitatively material, IAS 12 disclosures must be provided.

Examples on how to apply the factors to consider in Figure 1

Two examples have been added to IFRS Practice Statement 2 to demonstrate how to assess whether accounting policy information is material or immaterial. These relate to the disclosure of accounting policies for:

- Revenue from contracts with customers with more than one performance obligation – Example S, and

- Impairment of property, plant and equipment (Example T).

More information

For more information, please read our International Financial Reporting Bulletin IFRB 2021 07 IASB issues amendments to IAS 1, IAS 8 and IFRS Practice Statement 2 – Disclosure of Accounting Policies and Definition of Accounting Estimates.

Early adoption

These amendments are only effective for periods beginning on or after 1 January 2023 but we encourage entities to adopt these changes sooner rather than later. While many entities may have streamlined and tailored accounting policies during the ‘Disclosure Initiative’ a few years ago, there are still many that have a long way to go.

Need help?

BDO’s IFRS Advisory Team is here to if you require assistance streamlining your accounting policies, converting them to Plain English, and making them entity-specific. Please contact us if you require assistance.