Financial assets under IFRS 9 – The basis for classification has changed

One of the key differences introduced by IFRS 9 Financial Instruments (IFRS 9) relates to the manner in which financial assets are classified. The difference relates not just to the measurement options available, but also to the process that is followed when determining the measurement basis that will apply.

Under IAS 39, financial asset classification, and consequently measurement, is based on the financial asset’s characteristics and management’s intention in relation to the asset. For example:

| An investment in: | Will be classified as: | And carried at: | If management intends to: |

| Ordinary shares of another entity | A financial asset at fair value through profit or loss | Fair value, with value changes recognised in profit or loss | Hold the financial asset for trading (short term profit taking) |

| Available for sale | Fair value, with value changes recognised in other comprehensive income | Hold the financial asset for the longer term | |

| Debt instruments (such as bonds) of another entity | A financial asset at fair value through profit or loss | Fair value, with fair value changes recognised in profit or loss | Hold the financial asset for trading (short term profit taking) |

| Held to maturity | Amortised cost (which results in value changes being recognised in profit or loss) | Hold the financial asset to maturity and the entity has the ability to do so | |

| Available for sale | Fair value, with value changes recognised in other comprehensive income | Hold the financial asset for the longer term, but not until maturity |

When IFRS 9 is adopted, classification of financial assets will be based on the characteristics of the financial asset and the business model under which the financial asset is held.

The business model under which a financial asset is held is determined on the basis of how an entity typically manages such assets – it is a matter of fact rather than on intention. This means that the classification of financial assets under IFRS 9 is based on facts rather than management intention (as is the case under IAS 39).

The other key difference between IFRS 9 and IAS 39 in the classification of financial assets is the default measurement category. Under IFRS 9, the default financial asset measurement category is fair value through profit or loss (FVTPL), while under IAS 39 it is available for sale (which also requires measurement at fair value, but results in less volatility in profit or loss because fair value changes are recognised in other comprehensive income).

Initial measurement of financial assets under IFRS 9

Under IFRS 9, a financial asset is initially measured at fair value plus transaction costs, unless it is carried at fair value through profit or loss, in which case transaction costs are immediately expensed. There is an exemption to this requirement – trade receivables without a significant financing component are initially recognised at the transaction price.

Under IFRS 9, when determining how a financial asset should be measured after initial recognition, the first step is to determine whether the financial asset is an equity instrument, or a non-equity instrument.

Subsequent measurement where the financial asset is a non-equity instrument

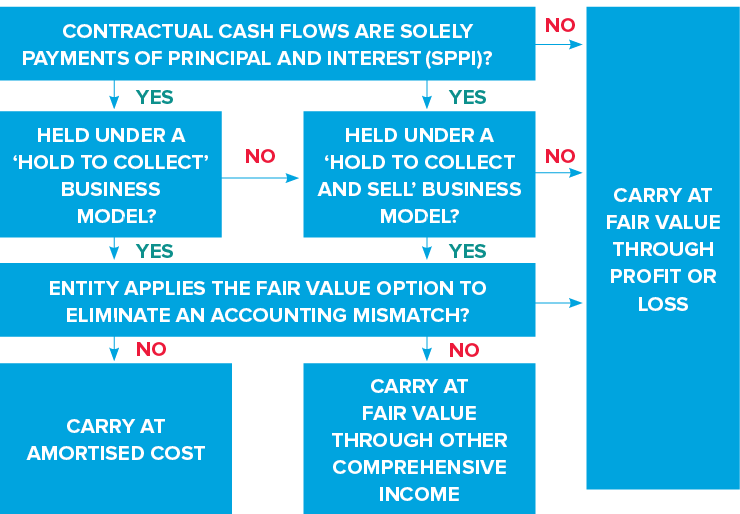

Where a financial asset is a non-equity instrument (e.g. debt instrument), measurement at amortised cost or at fair value through other comprehensive income only occurs if specified criteria are met (otherwise it is carried at FVTPL):

| If the instrument is: | It may be measured at: | If: |

| A non-equity instrument e.g. debt instrument | Amortised cost | It meets both:

|

| Fair value through other comprehensive income | It meets both:

|

A financial asset will pass the:

- ‘Contractual cash flow characteristics’ test if the financial asset gives rise on specified dates to cash flows that are solely payments of principal and interest on the principal amount outstanding, with the key components of interest being the time value of money and credit risk

- ‘Hold to collect’ business model test if it is held within a business model whose objective is to hold financial assets in order to collect contractual cash flows

- ‘Hold to collect and sell’ business model test if it is held within a business model whose objective is to both collect contractual cash flows and sell the financial asset.

Even if a non-equity financial asset meets the criteria for measurement at amortised cost or at fair value through other comprehensive income, the entity can elect to carry it at fair value through profit or loss to eliminate an accounting mismatch.

The following flow chart shows how non-equity financial assets are classified under IFRS 9:

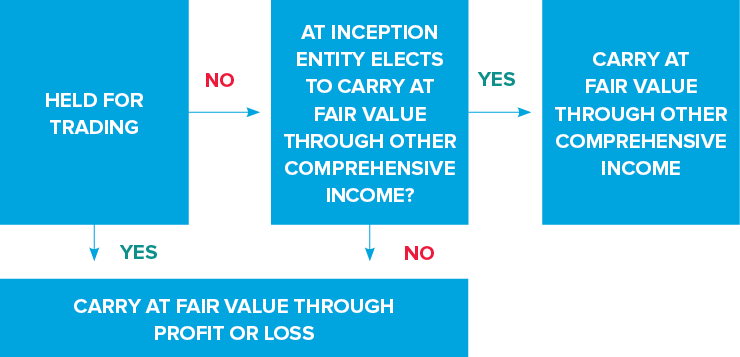

Subsequent measurement where the financial asset is an equity instrument

Where a financial asset is an equity instrument, the default measurement category is fair value through profit or loss; measurement at fair value through other comprehensive income only occurs if specified criteria are met:

| If the instrument is: | It may be measured at: | If: |

| An equity instrument | Fair value through other comprehensive income |

|

When an equity instrument is classified at fair value through other comprehensive income under IFRS 9, all the fair value changes are recognised in OCI (other than dividend income which is recognised in profit or loss). Upon sale of the equity instrument, the cumulative changes in OCI will never be recognised in profit or loss (i.e. there is no recycling of gains or losses). This is a significant difference to the available for sale category under IAS 39.

IFRS 9 has also tightened the requirements in relation to measuring unlisted equity investments at cost. This is only permitted in certain limited rare circumstances and will result in more financial assets being carried at fair value.

The following flow chart shows how financial assets that are equity instruments are classified under IFRS 9:

Concluding thoughts

Under both IFRS 9 and IAS 39, the characteristics of a financial asset are central to the manner in which it will be measured subsequent to initial recognition. Under IAS 39, management’s intentions in relation to a financial asset are also considered when determining the basis of measurement. However, under IFRS 9 management intention is irrelevant to measurement, and it is instead the entity’s business model in relation to financial assets that must be considered when determining measurement.

Determining the business model under which financial assets are held will require examination of past business practice. For those companies that are audited, it is likely that your auditor will require more evidence to support your financial asset classification decisions than has been required in the past.