IASB provides accounting relief for lessees who receive rent concessions

On Friday 15 May 2020 at a supplementary IASB meeting, the IASB decided to provide lessees with a practical expedient in accounting for particular COVID-19-related rent concessions. The practical expedient does not address lessor accounting. The IASB expects to issue the amendment to IFRS 16 on or around 28 May 2020. A lessee shall apply the amendment for annual reporting periods beginning on or after 1 June 2020. Earlier application is permitted, including in annual and interim financial statements not yet authorised for issue at the date the amendment is issued.

Why did the IASB decide to amend IFRS 16?

Many lessors have provided, or are expected to provide, rent concessions to lessees as a result of the COVID-19 pandemic. This is particularly prevalent in the retail industry and, in some cases, is encouraged or required by government. Rent concessions provided include rent holidays or rent reductions for a period of time, possibly followed by increased rent payments in future periods.

Lessees may have difficulty:

- Assessing whether a potentially large volume of COVID-19-related rent concessions are lease modifications; and

- Applying the required accounting in IFRS 16 to those that are lease modifications.

What is the amendment to IFRS 16?

The IASB has decided to amend IFRS 16 to permit lessees, as a practical expedient, not to assess whether particular COVID-19-related rent concessions are lease modifications. Instead, lessees that apply the practical expedient would account for those rent concessions as if they were not lease modifications.

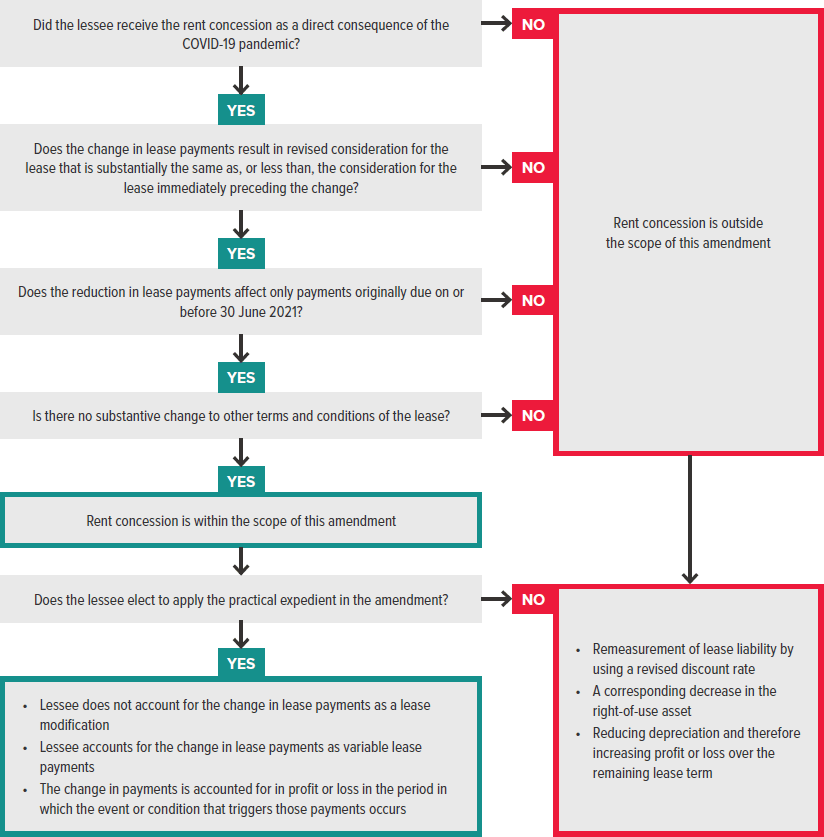

Starting point - Assess whether a rent concession is within the scope of this amendment

The practical expedient applies to rent concessions only if all of the following conditions are met:

- The rent concession occurs as a direct consequence of the COVID-19 pandemic;

- The change in lease payments results in revised consideration for the lease that is substantially the same as, or less than, the consideration for the lease immediately preceding the change;

- Any reduction in lease payments affects only payments originally due on or before 30 June 2021 (for example, a rent concession would meet this condition if it results in reduced lease payments before 30 June 2021 and increased lease payments that extend beyond 30 June 2021); and

- There is no substantive change to other terms and conditions of the lease.

What are the accounting consequences if the rent concession is outside the scope of this amendment?

The lessee will need to assess whether the rent concession meets the definition of a lease modification or not. IFRS 16 defines a lease modification as “A change in the scope of a lease, or the consideration for a lease, that was not part of the original terms and conditions of the lease (for example, adding or terminating the right to use one or more underlying assets, or extending or shortening the contractual lease term)”. This assessment might be difficult. For example, a lease contract or applicable law or regulation may contain clauses, such as force majeure, which were developed without contemplating the COVID-19 pandemic. It may be difficult to determine whether rent concessions offered—or mandated by government—are captured by the operation of such clauses.

Revised lease payments as a result of a rent holiday or 6-month reduction in lease payments will often meet the definition of a lease modification and therefore result in the following accounting treatment under IFRS 16:

- Remeasurement of the lease liability by discounting the revised (e.g. reduced) lease payments using a revised discount rate;

- A corresponding decrease in the carrying amount of the related right-of-use asset; and

- Reducing depreciation over the remainder of the lease term.

What are the accounting consequences if the rent concession is within the scope of this amendment?

As a practical expedient, a lessee may elect not to assess whether a COVID-19-related rent concession is a lease modification. A lessee that makes this election shall account for any change in lease payments resulting from the COVID-19-related rent concession the same way it would account for a change applying IFRS 16 if the change were not a lease modification.

IFRS 16 states that if a change in lease payments does not result from a lease modification, the change in lease payments would generally be accounted for as a variable lease payment. The lessee is required to apply paragraph 38 of IFRS 16 and generally recognises the change in payments in profit or loss in the period in which the event or condition that triggers those payments occurs. It could be argued that the event or condition that triggers the negative variable payments (i.e. rent concessions) is the granting of the rent concessions to the lessee by the lessor or government. The granting of a rent concession will therefore lead to a profit or loss impact at the time when the rent concession is granted. For example, if a lessor provides rent relief to a lessee before 30 June 2020 and it meets all the criteria as required by the amendment to IFRS 16 (e.g. relates to lease payments originally due before 30 June 2021), then the profit or loss impact of the variable lease payments will be recognised in the 30 June 2020 financial statements.

A lessee that chooses to apply the practical expedient applies it consistently to all lease contracts with similar characteristics and in similar circumstances, as already specified by paragraph 2 of IFRS 16.

Overview of the Amendments to IFRS 16