Time running out to ‘declutter’ your financial statements - 31 December 2016 financial statements must be ‘decluttered’

As part of the International Accounting Standards Board’s initiative to improve disclosures in financial statements (Disclosure Initiative), amendments have been made to AASB 101 Presentation of Financial Statements to facilitate ‘decluttering’ of financial statements by allowing preparers to apply judgement when deciding which mandatory disclosures are relevant to users, and which are not.

| The ‘decluttering’ requirements apply to your 31 December 2016 financial statements. |

While ‘decluttering’ is not normally associated with half-year financial statements prepared under AASB 134 Interim Financial Reporting, if you are preparing annual financial statements at 31 December 2016, we recommend that you commence this process now.

What do we mean by ‘decluttering’?

The changes to AASB 101 clarify that:

- Notes to the financial statements only need to be included if they are material (even if they form part of a list of black-letter, mandatory disclosures)

- Notes can now be in any order and need not follow the order of the four primary financial statements. For example, notes can now be grouped by operating activities, or by how items are measured (e.g. all items at fair value)

- Balance sheet categories can be further disaggregated if this is relevant to a user’s understanding of the entity’s financial position (e.g. an entity with significant balances of goodwill and brand names can present each of these separately in the balance sheet to meet the requirement to disclose intangibles)

- Only significant accounting policies need to be disclosed (a laundry list (summary) is no longer required).

Are our financial statements ‘overweight’?

If your financial statements include any of the following features, it is likely that your financial statements are ‘overweight’, and therefore in need of ‘decluttering:

|

Too much useless information about immaterial items that are not relevant to users (e.g. small profit or loss item disclosures, detailed reconciliations of PPE where movements are minimal during the period) |

|

Accounting policies describing transactions and events that do not occur in the entity (e.g. hedging, certain types of financial instruments, consolidations, equity accounting, joint arrangements, revaluing assets, etc.) |

|

Accounting policies that are so boilerplate that users are unable to really understand how transactions are recognised and measured (e.g. revenue recognition) |

|

Information about sources of estimation uncertainty that is so boilerplate it tells the user nothing about the specific assumptions made in the estimate that could impact the estimation of the carrying amount of assets and liabilities in the next financial year |

|

Providing information about estimates that are not significant to the financial statements (e.g. employee leave provisions), or will not result in a material adjustment to assets and liabilities in the next financial year (e.g. share-based payment estimations) |

|

Boilerplate information about judgements made that do not explain, in plain English, what the judgement was (e.g. choice of accounting policy A instead of accounting policy B because …) |

|

Laundry lists of detailed information about standards that are only effective in future years which are unlikely to have a material impact on the entity, or indeed could never vaguely apply to the entity because they do not operate in a particular industry, or engage in the relevant types of transactions |

|

Comparative information carried forward which has no relevance to the current period financial statements (e.g. including detailed disclosures for a business combination that occurred two years ago, or a share-based payment that was granted three years ago) |

|

Too much narrative when a tabular format of disclosure would enable the user to better understand disclosures |

|

Technical accounting or other jargon which is not explained, rather than using plain English wherever possible |

|

Notes about the most important transactions and events buried in the financial statements, making them hard to find. |

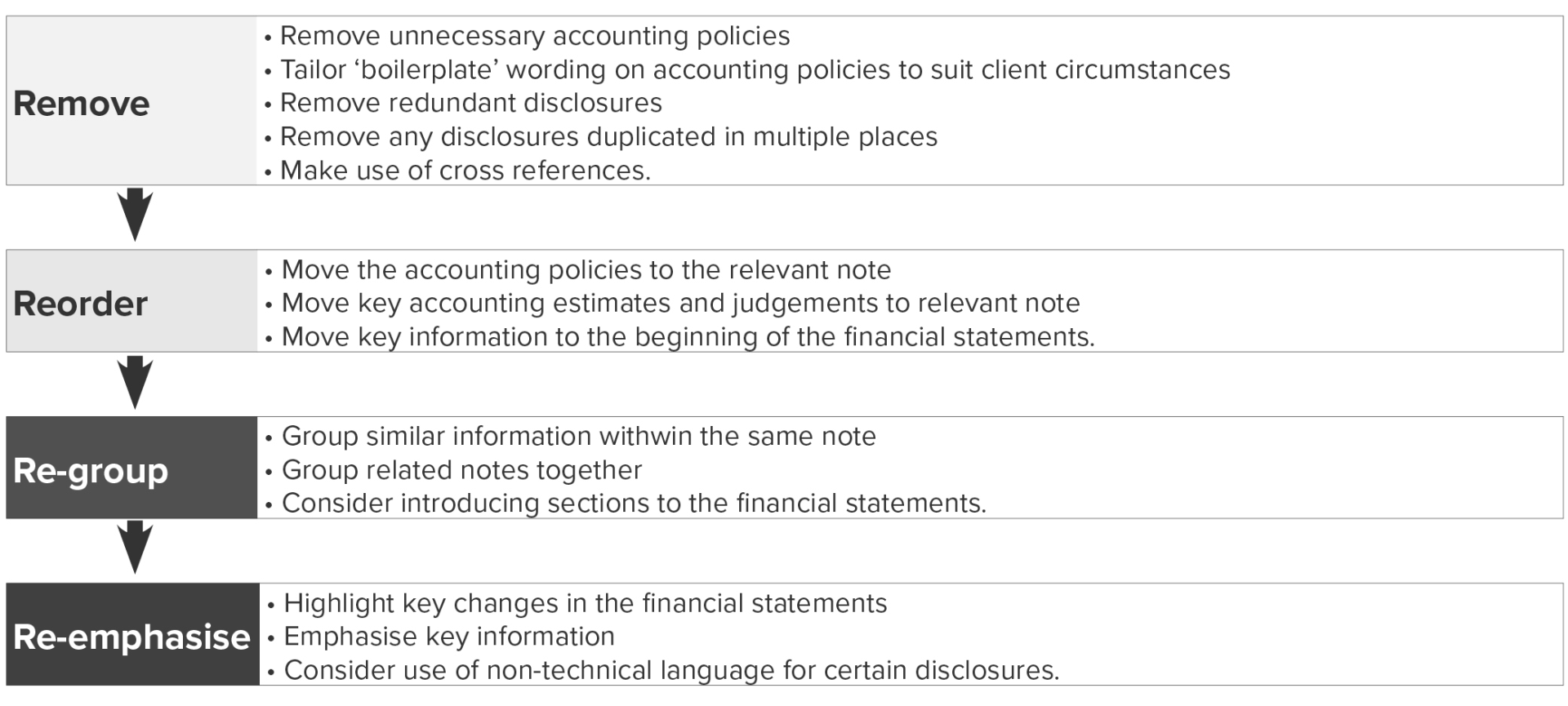

The ‘Four Rs’ - How do we start the ‘decluttering’ process?

Our November 2015 Accounting News provides a detailed step by step approach, which we call ‘the Four Rs’, which will help you to start your ‘decluttering’ process.

To summarise, you should:

- Firstly, REMOVE any unnecessary information in the financial statements, including redundant accounting policies, and properly tailor information, particularly for accounting policies and estimates and judgements.

- Secondly, REORDER information in the financial statements. Of companies that adopted these changes early, and ‘decluttered’ their 2015 financial statements, we found that the most useable financial statements moved their accounting policies, and critical accounting estimates and judgements, into the relevant notes.

- Thirdly, RE-GROUP similar information into the same note, and then grouped related notes together – for instance, include impairment information with the intangible assets that have been impaired during the period.

- Finally, RE-EMPHASISE information by using boxes, colours and other items to highlight key changes in the financial statements that users should be aware of. Companies that have done this already have also tended to use plain English to describe transactions – whether this be for the entire note, or a simple overview at the beginning of a section.

Is ‘decluttering’ also required for special purpose financial statements and general purpose financial statements applying the reduced disclosure requirements?

While the number of disclosures required in special purpose financial statements, and general purpose financial statements applying reduced disclosures is obviously significantly less than for full general purpose financial statements, our experience shows that most entities have some work to do, including:

- Removing redundant accounting policies and tailoring them in plain English

- Moving accounting policies to the relevant transaction/balance note, which often indicates that many accounting policies have ‘nowhere to go’ and should be deleted

- Tailoring material estimate notes to the relevant transaction/balance, and ensuring that assumptions are properly described and if necessary, quantified

- Tailoring material judgement notes

- Considering note ordering.

More cash flow statement disclosures to come

For periods beginning on or after 1 January 2017, changes have been made to AASB 107 Statement of Cash Flows to require that you disclose additional information to provide users with information to evaluate changes in liabilities arising from financing activities, including changes arising from cash flows and non-cash flows.

An example of what these disclosures might look like is shown below:

|

|

Non-cash changes | |||||

|

|

2016 | Cash flows | Acquisition | Foreign exchange movement | Fair value changes | 2017 |

|

|

$ | $ | $ | $ | $ | $ |

| Long-term borrowings | 22,000 | (1,000) | - | - | - | 21,000 |

| Short-term borrowings | 10,000 | (500) | - | 200 | - | 9,700 |

| Lease liabilities | 4,000 | (800) | 300 | - | - | 3,500 |

| Assets held to hedge long-term borrowings | (675) | 150 | - | - | (25) | (550) |

| Total liabilities from financing liabilities | 35,325 | (2,150) | 300 | 200 | (25) | 33,650 |

More information

For more information on the Disclosure Initiative, please refer to the IASB Disclosure Initiative section of our Issues and Trends page on our web site.