When is the acquisition of a business accounted for as a business combination?

Preparing general purpose financial statements (GPFS) means that entities must comply with the recognition and measurement requirements of all Australian Accounting Standards, including when accounting for business combinations.

Which Accounting Standard applies?

IFRS 3 Business Combinations is the Accounting Standard that describes the appropriate accounting treatment for ‘business combinations’. However, IFRS 3 does not apply in the following instances:

- The formation of a joint arrangement (in the financial statements of the joint arrangement itself)

- The acquisition of an asset or group of assets that does not constitute a business (asset acquisition)

- A combination of entities or businesses under common control, and

- Where a parent entity reorganises its group by establishing a new parent entity on top of an existing company or group of companies (frequently referred to a 'top hatting').

Asset acquisitions

The purchase of a group of assets, or a group of assets and liabilities, does not automatically meet the definition of a ‘business’. If not a business, the acquisition is accounted for as an ‘asset acquisition’. The distinction is important because there are significant differences in the accounting for asset acquisitions vs business combinations, which could have a material impact on post combination profit or loss, as well as on the statement of financial position of the acquirer group.

For an asset acquisition, we therefore do not see goodwill or deferred tax recognised as part of the acquisition entries. Transaction costs are capitalised into the carrying value of individual assets, rather than being expensed as is the case for business combinations.

Common control transactions

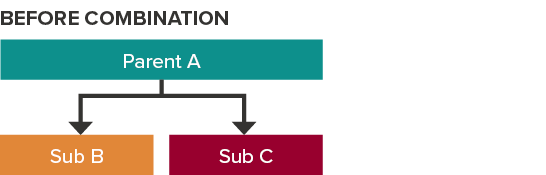

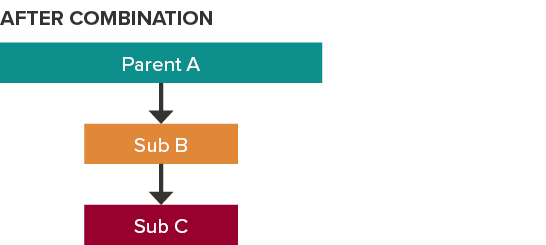

Business combinations under common control are also not accounted for under IFRS 3. A key feature of these transactions is that both before and after the transaction, all of the combining entities or businesses are controlled by the same party or parties, and the control is not transitory (i.e. a restructure has not taken place to utilise a particular accounting treatment prior to another transaction). These reorganisations are generally performed to either streamline the group's operations, for tax reasons or for other reasons. The diagram below illustrates a very simple example where the structure of Parent A group is reorganised so that Sub C is owned directly by Sub B rather than Parent A.

|  |

| Example of business combination under common control | |

‘Book value accounting’ is the most commonly used method to account for business combinations under common control. Under this method, no changes are made to the carrying values recognised for assets and liabilities. This is because the acquired business has simply moved from one part of a group under common control to another. Only in rare cases where the common control transaction has substance can it be accounted for under IFRS 3.

Establishing a new parent entity on top of an existing company or group

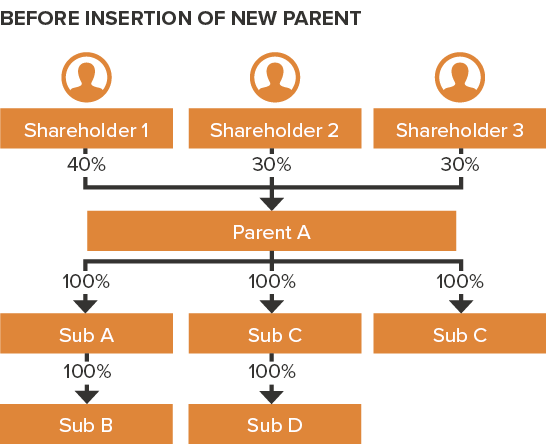

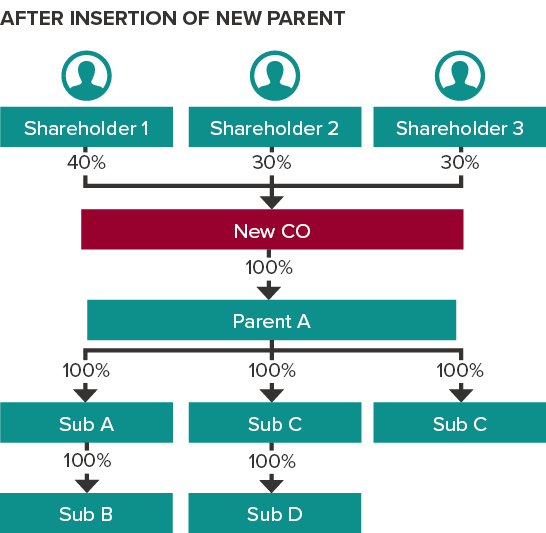

‘Top hatting’ transactions, often performed for tax reasons or prior to an IPO, occur where a parent entity establishes a new parent entity on top of an existing company or group of companies. An example of this type of transaction is shown below, where NewCo (a shell company with its only asset being 100 shares in Parent A) is established above Parent A (a holding company for trading subsidiaries):

|  |

These transactions are usually accounted for using a ‘pooling of interests’ method which combines the assets, liabilities and reserves of Parent A and Subs A to E, and records them at historical values.

What is a ‘business combination’?

A ‘business combination’ is a transaction where an acquirer obtains control of one or more ‘businesses’.

What is a ‘business’?

A ‘business’ is defined in IFRS 3 as an integrated set of activities and assets that is capable of being conducted and managed for the purpose of:

- Providing goods or services to customers

- Generating investment income (such as dividends or interest), or

- Generating other income from ordinary activities.

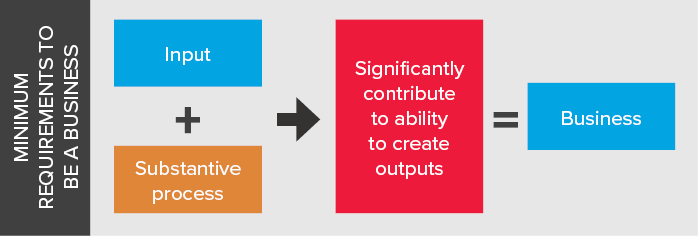

IFRS 3, paragraphs B7-B12D provide extensive guidance on the definition of a ‘business’. A ‘business’ consists of inputs and substantive processes applied to those inputs that have the ability to contribute to the creation of outputs.

Inputs

An input is an economic resource that create outputs, or has the ability to contribute to the creation of outputs, when one or more processes are applied to it. Examples include:

- Non-current assets such as plant and equipment, intangible assets and rights-to-use non-current assets

- Intellectual property, and

- The ability to obtain access to necessary materials or rights and employees.

Processes

A process is any system, standard, protocol, convention or rule that, when applied to an input or inputs, creates outputs, or has the ability to contribute to the creation of outputs. Examples include:

- Strategic management processes

- Operational processes, and

- Resource management processes.

Accounting, billing, payroll and other administrative systems are not processes used to create outputs.

Outputs

Outputs are the result of inputs and processes applied to inputs that:

- Provide goods or services to customers

- Generate investment income (such as dividends or interest), or

- Generate other income from ordinary activities.

As is evident from the above diagram, outputs are not required for there to be an integrated set of activities and assets (i.e. a business). The two essential elements for a business are merely inputs, and a substantive process, which together significantly contribute to the ability to create outputs. While businesses usually have liabilities, it should be noted that a business does not always have liabilities.

Substantive processes

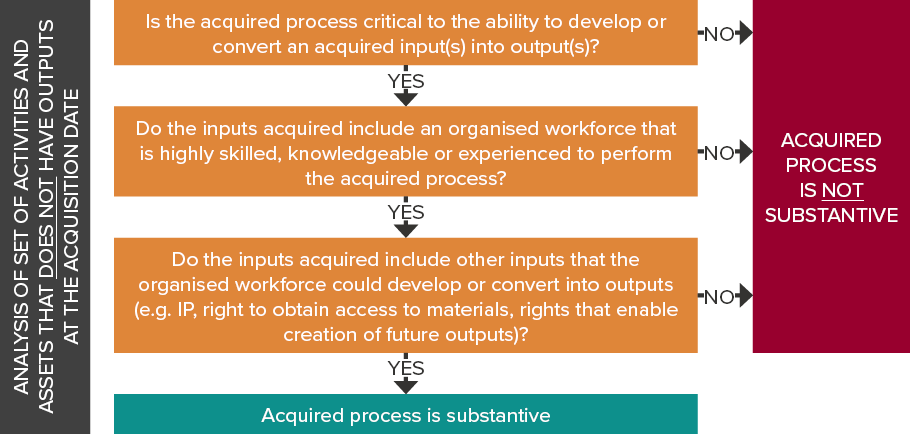

As noted above, a ‘business’ must, as a minimum, contain an input and a substantive process. IFRS 3 contains a complex set of requirements and examples to determine whether an acquired process is substantive, with different rules, depending on whether the acquired set of activities and assets:

- Has outputs, or

- Does not have outputs (e.g. an early stage company that has not started generating revenue).

The diagram below shows the criteria for determining whether a set of activities and assets that does not have outputs at the acquisition date is a substantive process.

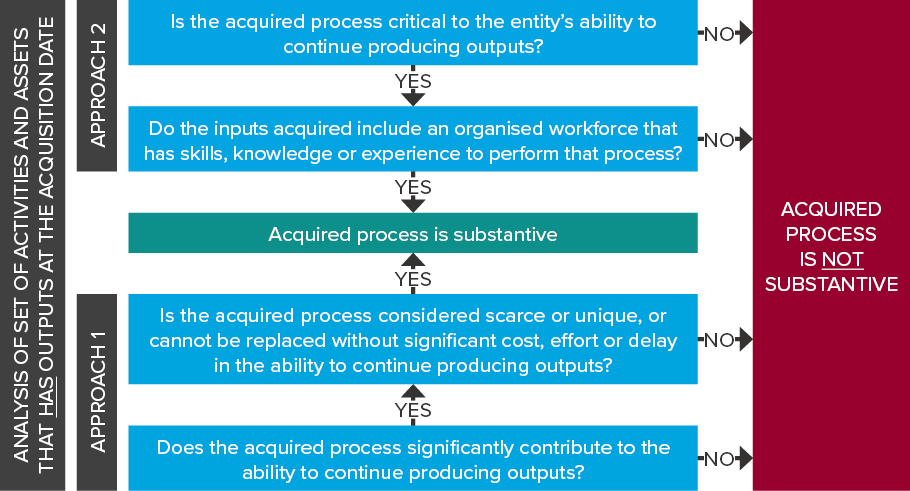

Where a set of activities and assets has outputs at the acquisition date, there are two approaches for determining whether an acquired process is substantive. If the test in either approach is met, the acquired process is substantive, otherwise it is not substantive.

If the transaction includes a minimum of an input and a substantive process, or an input, a substantive process and an output, it would meet the definition of a business combination and be accounted for under IFRS 3.

Optional concentration test

IFRS 3 also includes a ‘short cut’ method (optional concentration test) whereby an acquirer can conclude that an integrated set of activities and assets is not a ‘business’. This optional concentration test can be applied on a transaction by transaction basis.

The concentration test is met if substantially all of the fair value of the gross assets acquired is concentrated in a single identifiable asset or group of similar identifiable assets.

IFRS 3.B7B

IFRS 3.B7B includes detailed criteria that must all be met before concluding that the acquired set of activities and assets is not a business (refer to September 2020 Accounting News for more information).

If all of the paragraph B7B criteria:

- Are met – the transaction is accounted for as an asset acquisition

- Are not met - the detailed assessment described above of inputs, processes and outputs must be performed to determine if a business has been acquired.

Need assistance?

In practice, assessing whether a transaction is a business combination can be extremely complex and judgemental, and determining the appropriate accounting where a transaction falls outside the scope of IFRS 3 is also not always straightforward. Please contact BDO’s IFRS & Corporate Reporting team if you require assistance with this process.

More information

Additional resources are available on this topic, including:

- You can purchase our e-learning materials on IFRS 3 - Business combinations on our website

- IFRS in Practice, Distinguishing between a business combination and an asset purchase in the extractives industry.