ASIC focus areas for 31 December 2022 financial reports

ASIC focus areas for 31 December 2022 financial reports

The Australian Securities and Investments Commission (ASIC) conducts surveillance on the financial reports of Australian entities (mainly listed entities) as part of its financial reporting surveillance program. As a result of these risk-based reviews, ASIC conducts inquiries on matters of concern, and depending on the outcome, entities may be ‘named and shamed’ in media releases if they restate financial reports as a result.

In two recent Media Releases, ASIC outlined its focus areas for its surveillance of 31 December 2022 financial reports, and called for greater focus on material business risk disclosure in annual reports. Directors, preparers, and auditors should take note of these to ensure financial reports provide useful and meaningful information for investors and other users. Focus areas of other regulators are consistent with ASIC.

Five focus areas

ASIC’s focus areas Media Release highlights five areas that it will focus on when it conducts these reviews:

- Uncertainties and risks

- Asset values

- Provisions

- Subsequent events

- Disclosures in the financial report and the Operating and Financial Review (OFR).

These are discussed further below. In addition, ASIC highlights that:

- Insurers must continue to disclose the impact of the new insurance accounting standard, IFRS 17 Insurance Contracts in the notes to the 31 December 2022 financial report. Given the new standard applies for periods beginning on or after 1 January 2023, it is reasonable to expect insurers to be able to quantify the impact of the new standard in their 31 December 2022 financial reports. Non-insurers affected by IFRS 17 for certain transactions should include similar note disclosures

- Entities need to consider whether off-balance sheet exposures should be recognised on-balance sheet (for example, interests in non-consolidated entities)

- Aged care providers need to assess their accounting treatment for bed licences given they are to be discontinued on 1 July 2024

- Private health insurers should consider the impacts on the deferred claims liability for changes in the backlog of deferred procedures. A liability may be required for a commitment to return premiums to existing policyholders for savings during the pandemic

- Entities must disclose material penalties for non-compliance with sanctions imposed in Australia or elsewhere in relation to Russia.

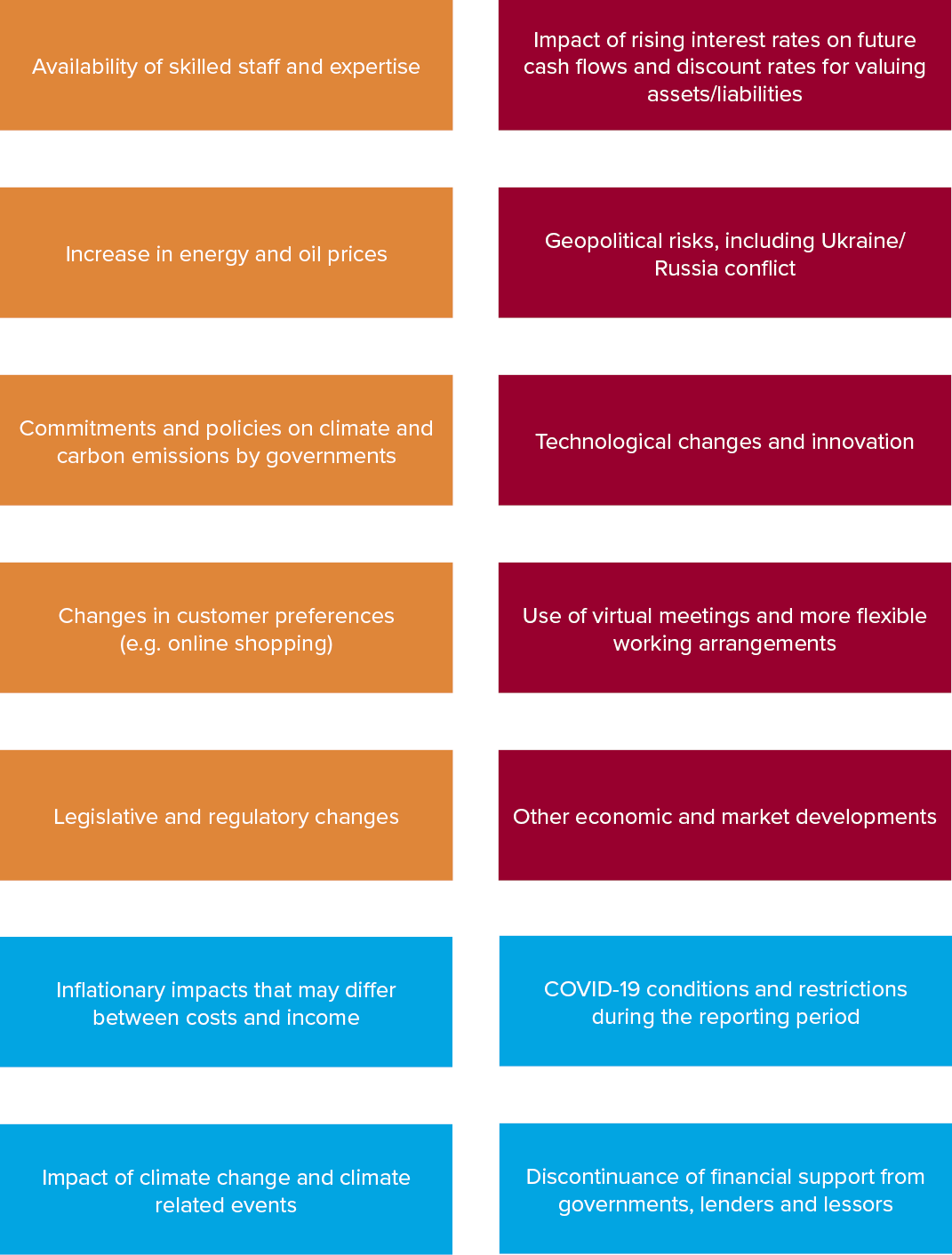

Uncertainties and risks

Entities continue to face changes in circumstances and uncertainties about future economic and market conditions that may impact their business strategies and future financial performance. These uncertainties should be factored into the assumptions used for financial reporting purposes and should be reasonable and supportable. Examples of changes in circumstances, uncertainties, and risks to be considered when preparing 31 December 2022 financial reports include those listed in the diagram below. This list is not exhaustive.

Asset values

ASIC’s focus on asset values relates to the following areas:

|

Financial statement area |

Focus areas |

|

Impairment of non-financial assets |

|

|

Values of property assets |

Note: Refer to our Lease Accounting webpage for more information about the complexities of lease accounting, including software solutions, training materials, and publications. |

|

Expected credit losses (ECL) on loans and receivables |

|

|

Value of other assets |

|

Provisions

Entities should consider the need for, and adequacy of, provisions for onerous contracts, leased property make good, mine site restoration, financial guarantees given, and restructuring.

Subsequent events

Entities should review events occurring after the end of the reporting period, in order to determine whether these are ‘adjusting’ or ‘non-adjusting’ post-balance date events.

Disclosures in the financial report and OFR

Lastly, entities should focus on ensuring adequate disclosures as outlined in the table below.

|

Consider |

Focus areas |

|

General considerations |

|

|

Disclosures in financial report |

|

|

Disclosures in OFR |

Note: The Media Release notes that the OFR should include a discussion on environmental, social and governance (ESG) risks. Disclosing an exhaustive list of generic risks that might potentially affect a large number of entities is not helpful, and these risks should be described in context. For example, it could include discussion about:

Also refer to ASIC’s separate Media Release MR 22-332 that calls for greater focus on material business risk disclosure in annual reports, as well as BDO’s recent article on this subject. |

|

Assistance and support from others |

|

|

Non-IFRS financial information |

|

|

Disclosure in half-year financial reports |

|

Need assistance?

Please contact our IFRS Advisory team if you need support with any financial reporting matters for your 31 December 2022 financial reports.