Have you accounted for all your ‘make good’ and restoration provisions?

Have you accounted for all your ‘make good’ and restoration provisions?

The implementation of IFRS 16 Leases in 2019/2020, as well as increasing shareholder interest about Environmental, Social and Governance (ESG) matters, has highlighted that ‘make good’ and restoration provisions recognised in the balance sheets of lessees, oil and gas producers and other mining operators may often be incomplete or insufficient.

What is the difference between ‘make good’ and restoration provisions?

‘Make good’ and restoration provisions are essentially the same thing but ‘make good’ provisions usually refer to the obligation of a tenant (lessee) to return their rental premises to the landlord in a similar condition to when they moved in, whereas the term ‘restoration provision’ covers similar ‘make good’ obligations, but is usually used for oil and gas and certain mining entities.

‘Make good’ provisions

Examples of ‘make good’ provisions include:

- If a tenant rents the premises as a shell, their ‘make good’ obligation could involve stripping all fixtures and fittings, removing staircases, and returning the premises to the landlord as a shell (sometimes also referred to as decommissioning obligations)

- If the tenant rents empty space that is carpeted and newly painted, their ‘make good’ obligation may require returning the premises with new carpet and a fresh coat of paint.

The introduction of IFRS 16 means ASIC now has greater visibility of the leasing activities of groups with a significant retail footprint, so it is in a better position to assess the adequacy of ‘make good’ provisions that must typically be settled in some form at the end of a lease. Such entities need to consider their ‘make good’ obligations in every single lease and provide for all obligations meeting the recognition and measurement criteria in IAS 37 Provisions, Contingent Liabilities and Contingent Assets.

Restoration provisions

Examples of restoration provisions include:

- Manufacturers required to cleanup environmental damage

- Exploration entities required to rectify land damage caused by drilling

- Oil and gas entities required to decommission and remove pipelines and infrastructure including any offshore and certain subsea infrastructure

- Mining entities required to decommission and rehabilitate a mine site at the end of the life of the mine.

In light of ASIC’s recent media releases, oil and gas and mining entities need to reassess whether they have adequately provided for all restoration obligations under IAS 37 because these are likely to be material.

When to recognise ‘make good’ and restoration provisions?

‘Make good’ and restoration provisions are recognised in accordance with IAS 37, paragraph 14, as follows:

- an entity has a present obligation (legal or constructive) as a result of a past event

- it is probable that an outflow of resources embodying economic benefits will be required to settle the obligation; and

- a reliable estimate can be made of the amount of the obligation. If these conditions are not met, no provision shall be recognised.

IAS 37, paragraph 14.

It is therefore important to correctly identify the past event (obligating event) because this is what determines when the provision is recognised. An obligating event is one where the entity has no realistic alternative but to settle the obligation created by the past event, which can only occur if either:

- Settlement of the obligation can be enforced by law

- For constructive obligations, the event creates a valid expectation by other parties that the entity will discharge the obligation.

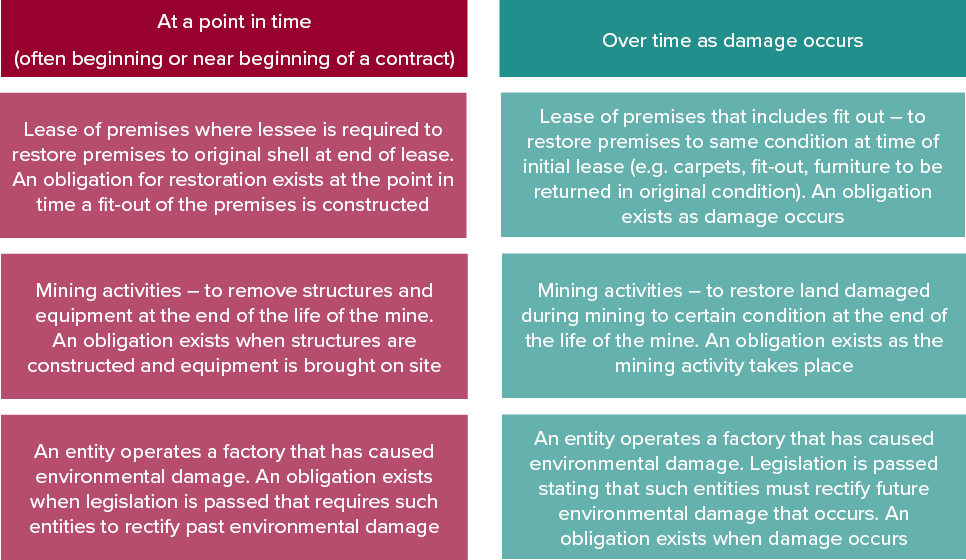

So, essentially, ‘make good’ and restoration provisions are recognised when the obligating event to rehabilitate property occurs, which is usually as and when the entity’s actions have damaged property. This is illustrated in the diagram below.

Recognising ‘make good’ and restoration provisions too early or too late can have a material impact on the financial statements. For example:

- If a mine fails to recognise its full decommissioning obligation as soon as the mine structure and equipment is constructed and installed on the property, provisions will likely be significantly understated.

- If a mine recognises upfront as a provision the full expected cost of rectifying environmental damage expected to occur to property over the life of the mine, provisions will likely be significantly overstated.

ESG commitments do not necessarily result in restoration provisions

Some ESG commitments result in a restoration provision being recognised in the balance sheet and others not.

Investor pressure to improve an entity’s ESG commitments in the future would not result in restoration provisions being recognised in the balance sheet. This is because there is no past (obligating) event. While an entity’s commitment to the public (e.g. net zero by 20XX) is a ‘constructive obligation’, it does not arise as a result of a past event that gives rise to a provision.

Contrast this with an entity that is not legally required to rehabilitate contaminated land, but publicly promises to voluntarily do so. Contaminating the land is the past event, and the promise to rehabilitate is the constructive obligation that creates an obligating event to be recognised as a provision under IAS 37.

Need assistance?

Determining whether a ‘make good’ or restoration provision meets the recognition requirements in IAS 37 is not always easy. Judgement is often required to assess whether there is a present obligation as a result of a past event, i.e. identifying if there is an obligating event. Please contact BDO’s IFRS & Corporate Reporting team if you require assistance.