Automotive update: Impacts of the New Vehicle Emissions Standard on Australian dealerships

Automotive update: Impacts of the New Vehicle Emissions Standard on Australian dealerships

The Australian automotive industry has always drawn a full sail to the winds of change. Between high interest rates, rapid return of supply and soft economic conditions, the Federal Government’s move to introduce the long anticipated New Vehicle Efficiency Standard (NVES) is a substantial shove in the back of an industry long dominated by Internal Combustion Engine (ICE) vehicles, but what does this attempt at a rapid pivot to Battery Electric Vehicles (BEV) mean for Australian dealers?

What is the New Vehicle Emissions Standard?

The New Vehicle Emissions Standard (NVES) is a federal government policy aimed at reducing carbon emissions from new vehicles sold in Australia, primarily by penalising higher carbon dioxide emitting vehicles and encouraging original equipment manufacturers (OEMs) to supply more BEVs.

Although there is a near-uniform agreement that a policy of this nature is required in Australia and overdue, the implementation must be done cumulatively and in a manner in which the industry can adjust without ultimately disadvantaging consumers through either increased prices or a lack of vehicle choice.

The NVES is, according to the federal government, designed to:

- Save money at the petrol pump

- Give consumers more choice about the cars they can buy

- Reduce transport emissions, improving the air that you and your family breathe.

Potential effects of the NVES

Any policy which affects supply, demand, or as in this case, both, will have a direct impact on dealers. We’ve outlined the broad direct and indirect impacts to dealers to provide guidance for our clients on how to respond to the introduction of the NVES.

This guidance surrounds the ideology this policy seeks to implement, principally to shift Australian consumer interest from high carbon emissions vehicles to BEVs, and the lack of comparable BEVs or government incentives to implement this change.

It should be noted that at the time of publishing this article, the Biden administration had announced it was allowing US manufacturers more time and flexibility in meeting vehicle emissions standards, opening a door for the Australian federal government to implement changes of their own.

How would the NVES impact the Australian market?

The Federal Chamber of Automotive Industries (FCAI) reported in their full year 2023 VFACTS data that the most popular vehicle in 2023 was the Ford Ranger. This was closely followed by the Toyota HiLux, with the Isuzu Ute D-Max/MUX variants in third. These Light Commercial Vehicles (LCVs) alone account for over 12 per cent of the total cars sold in Australia last year, painting a clear picture of Australian consumer preferences.

CarSales recently reported that Toyota Australia were bringing forward the hybrid option for the soon to be released all-new Prado model, around the same time Toyota Global CEO Ted Ogawa was reported in Electrek as saying he believes EVs will only make up 30 per cent of the US new-vehicle market in 2030 (half the target sought by the US EPA last year) and that Toyota is better positioned to simply buy credits to close the EPA gap rather than ‘waste money’ on battery electric vehicles. “We are respecting the regulation, but more important is customer demand,” Ogawa says - perhaps the most prescient quote with relevance to our own market.

There is very little pipeline of fit-for-purpose BEVs to replace their higher emitting LCV siblings, the most popular in Australia. Vehicles required to tow or be used as work vehicles do not have near-term BEV replacement alternatives, and risk being removed from the market altogether due to the anticipated cost impact of these vehicles, based on projected consolidated emissions of total OEM sales.

This lack of an immediate and comparable pipeline of BEVs by the most popular car manufacturers represented in Australia means there is almost certainly an immediate cost impact on the vehicles Australians buy, considering:

- Australians, to date, have been relatively slow adopters of electric vehicles, driven mainly by a lack of infrastructure and grid capacity to support large scale rollout of BEVs

- There is no immediate available supply of BEVs to ensure a cost-neutral approach for many of the most popular OEMs

- Australia is a small right-hand drive (RHD) market compared to the demands and more established electric vehicle (EV) policies (and subsidies) of North American and European markets.

How would the NVES impact manufacturers?

The impact on existing OEMs will be variable, depending on how reliant their current sales fleet is on high emission vehicles, and the pipeline of EV products ready to deploy, or at least in advanced development.

Those that stand to benefit the most, financially, are existing fully electric OEMs such as Tesla and BYD, and full-electric OEMs yet to enter the Australian market. Existing players will likely seek to buy credits from pure EV brands given their green status, rather than immediately deploying sufficient BEV variants capable of neutralising the carbon emissions of their entire sales fleet. This can be lucrative for fully-elective manufacturers – Tesla, for example, recorded a total annual revenue from selling carbon credits of USD $1.79 billion in 2023.

The policy also stands to further incentivise the entrance of Chinese BEV manufacturers keen to follow a now well-trodden path by the likes of MG, GWM, BYD and Chery. Currently facing weak local demand, China incentivised supply of its manufacturing sector, which now stands to export substantial volumes of low-cost EVs into foreign markets. In response, the US and many European countries are in the process of introducing tariffs and other measures to balance out price competition with locally produced vehicles, aiming to protect their own markets.

It stands to be seen what impact this will have on the Australian new vehicle market, now that the NVES policy provides an incentive to send vehicles here. BYD’s Australian growth may be an example of what is possible for other Chinese fully electric OEMs exploring the Australian market as a viable component of global expansion.

What is certain, as has been playing out over recent years, is that exposure to Chinese franchises is becoming an important factor for Australian dealers to diversify and, in turn, de-risk their business models.

How would the NVES impact Australian consumers?

The direct impact on Australians majorly surrounds affordability and infrastructure. Whilst BEVs provide demonstrated city-based fuel efficiency cost benefits, the price differential and limited availability of suitable options, along with unpredictability in resale values, at present largely offsets this.

Other than effectively seeking to make the alternatives more expensive, the policy in its current format does not provide a structure of incentives for consumers to purchase BEVs. Dealers will witness an inverse opportunity curve where those reliant on vehicles most favoured by Australians will be disadvantaged, as popular models such as the Ford Ranger, Toyota Hilux and Isuzu Utes will be directly targeted by the NVES policy.

Additionally, Australia is still waiting to see meaningful investment - private and public - in large scale EV infrastructure. Until Australians have more readily available access to renewable energy, saving money at the petrol pump will come at the increasing expense of time and convenience. Mainstream media is awash with frustrated EV owners reporting long wait times at available charging infrastructure and outages due to faulty infrastructure or overdue maintenance.

Unfortunately, current infrastructure issues have minimised the environmental potential of EVs. Victoria is reliant on approximately 60 per cent of its electricity supply from coal fired power stations, and in some recent examples of rural charging infrastructure quality, videos are emerging of (hopefully) short-term solutions involving chargers powered by diesel generators.

The required investment in infrastructure begs the following questions:

- Will dealers be prepared to invest capital for necessary facilities in a challenging economic climate where cash-flow preservation is paramount?

- Should new vehicle sales stay consistent (at 1.1 million to 1.2 million annual vehicle sales), how will this influence the adaptation of the extensive infrastructure already built by the 50+ OEMs currently operating in the Australian market?

Impacts for Australian dealers: an analysis on the policy’s short-term outcomes

Our analysis centres on agitation to supply and demand, compared with current market conditions. In short, the direct impact of the NVES is an increase to the price of many high emitting new vehicles, with a flow-on effect of reduced new vehicle margin (all other conditions being unchanged).

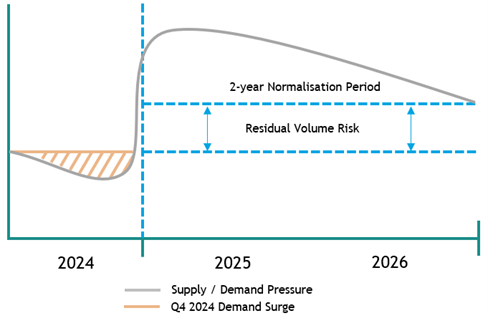

Modelling suggests the most obvious impact of the NVES policy is through calendar 2025 and 2026. As illustrated below, during this time the market is force-reconciled by consumers adapting to the positions adopted by each individual OEM, most of whom have indicated a high likelihood of passing any cost or penalties of this policy onto the dealer network and, ultimately, consumers.

Image 1: NVES impact model

Despite the possibility of penalties increasing under the NVES after the initial phase (only 10% of vehicles sold in 2023 would pass the 2029 emission thresholds, as is currently drafted), the medium-term outcomes may take two possible paths in our modelled ‘normalisation period’. Firstly, OEMs might supply more BEVs, especially comparable options for the most popular Australian vehicles, thus lowering their overall emissions. Alternatively, consumers may adjust by accepting higher prices for vehicles with higher emissions if they're still being sold.

During the fourth quarter (Q4) of the 2024 calendar year, it is anticipated that, as would ordinarily occur near 30 June, a demand surge will occur for consumers and fleets to acquire vehicles before revised pricing comes into effect on orders after 1 January. This will represent a significant opportunity for dealers in December where activity is generally quiet, relative to annual holidays. It will also stand to benefit average inventory balances which are so far expected to remain high well into the end of 2024.

It will come as no surprise that OEMs with minimal near-term BEV pipeline and heavy reliance on high carbon-emitting vehicles and/or LCVs stand to be more heavily impacted by the implementation of the NVES.

Factors to consider when calculating a dealership’s exposure include current dealer performance levels, the typical price elasticity for most popular models, pipeline of BEVs, balance of overall sales fleet emissions, and threat to core sales models.

Financial impact will mainly arise from decreased profit margins on new vehicles, which is already an issue in the industry. This serves as a warning that there will be even more pressure on profit margins for new vehicles – as such, current market conditions are an early indicator of how susceptible your dealership is to the proposed NVES policy. Sales turnover and its flow-on effect to pool of gross will also be a factor, where there is a reduction in new vehicle sales this poses a risk to used vehicles, finance, and aftermarket in the near-term, and risks a reduction in strength of back-end service and parts in the medium to long term.

There are, of course, OEMs who stand to be closer to cost neutral. For example, Hyundai, Volkswagen and MG, who have indicated their support and shown a greater balance of lower-emission vehicles and a strong pipeline of BEVs. Manufacturers that will be less effected, or who may stand to gain, include:

- Those already well advanced in EV offerings. Although not yet at parity with their non-electric offerings, the NVES will make non-electric competitor vehicles more expensive.

- Those with greater scale. A greater local and global scale will absorb at least some of the financial impact levied under the NVES (either directly or via increased dealer incentive structures), reducing the impact to consumers.

- Those with existing Australian brand power. In this case, customers will be likely to absorb most pricing increases. Whilst some OEMs may stand out here, it will largely be a level playing field. For example, Mercedes Benz, BMW and Audi generally have comparable models and variants, and whilst at different stages of BEV rollout, are already fighting for market share driven at least partially by pricing.

- Those with a mature and profitable dealer network. Starting from a position of strength will be an important advantage compared to networks lacking a mature service car-parc or above average level of dealer profitability.

BDO Automotive recommendation: What can dealers do to prepare?

In times of change, dealers are best to focus on what they can control. We have outlined some initial areas that we suggest for our clients to understand the impact on their business, as well as where to focus to ensure they are ready for any reduction in income during the normalisation period.

- Estimate the impact of NVES on your primary market area (PMA), as every region will be impacted differently. Factors such as cost of living pressures, average vehicle age, and demographic characteristics (e.g., families or retirees) can vary and influence the impact of the NVES regulations.

- Used cars are always the differentiator for those that thrive when challenging conditions prevail. Increased pricing on new vehicles will almost certainly drive increases to used vehicle prices, similar to the volatility seen during the Global Financial Crisis (GFC) and Covid-19 pandemic. This will be even more critical for dealers currently with below-average used vehicle departments, as they stand to face steep losses when the market moves quickly, most likely from mid-2024, as the implementation of the NVES approaches.

- Review return on inventory investment. Are you volume- or margin-oriented? How is this affecting the decisions your management team are, or are not making? These questions will provide important insight to your operations in times of uncertainty.

- Revisit your ‘pool of gross’. It is critical to understand your reliance on income from new vehicles in comparison to that from used, aftermarket, finance, service, and parts. If your dealership is still heavily reliant on front-end new vehicle gross (as rose prevalently through the Covid-19 pandemic) the chances are your profitability has already been heavily impacted by the return of new vehicle supply, deterioration of new-vehicle gross and substantially increased floorplan costs.

- Focus on the basics. Large dealer groups are refocusing on fundamentals in their sales operations, such as inventory management, customer experience, maintaining balanced profit margins, and leveraging economies of scale. If a dealer hasn't previously prioritised excellent customer experience, they'll likely find themselves in a situation where they're competing solely on price, which is not a sustainable strategy in the long term.

- Revisit the addition of lower footprint franchises to your existing. This should form a key pillar of a dealers buy or sell strategy. With some franchises facing increased competition and lower market share, it will benefit you to explore your own PMA and how this strategy can strengthen your business. Opportunities likely exist to look after existing service car parcs that are underrepresented and travelling outside of your PMA.

- Assess the strength of your finance business. For used cars, stocking the right (financeable) vehicles is essential. Now that consumer rates have increased, reviewing your net amount financed (NAF) is critical to ensuring you maximise incentives available under current plans. Alongside this, it is important to identify opportunities to renegotiate with white label and second tier providers should their incentive structures not generate required returns.

- Review performance of your aftermarket business. A clear gap between benchmark dealerships and average dealerships has emerged over the last 24 months. A benchmark dealer is now over $1,000 per new vehicle retailed, with an average dealer at $300-$450 per vehicle. For a dealer selling 1,000 new vehicles per annum, that is a gap of over $500,000 in gross margin.

- Support the growth and development of your talent. Remember that most salespeople employed within the past three years (without prior sales experience) have likely not learned the art of the sale. Back-to-basics sales training and promoting an environment of generating and converting leads is critical at a grass roots level.

- Carefully consider future capital investment in your dealership sites. Perhaps the most critical of factors, dealers must consider that for every $150,000 increase in rent expense, an average dealer would need to generate an additional $1,250,000 in gross profit in order to retain the level of the expense compared to gross margin. This will be particularly relevant for upgrading BEV dealership infrastructure and the OEM corporate identity (CI) updates that will accompany this transition.

Should you wish to discuss the impacts of the NVES in greater detail, including what it would mean for your own dealer group, reach out to our automotive experts today.

Sign up for BDO's annual Federal Budget analysis

Want to know more about other government initiatives in the pipeline that may affect your industry? Sign up now to be the first to receive our expert commentary on this year’s Federal Budget Release in May.