Accounting for Australian Carbon Credit Units (ACCUs) and other types of environmental units: Your questions answered

Over the past 12 months we’ve published a number of articles on accounting for Australian Carbon Credit Units (ACCUs). In response to these articles, we’ve received various queries from readers. In October 2025, we published an article addressing some of the more common queries we’ve received around ACCUs. In this article, we address additional questions about ACCUs and other types of environmental credits.

Question 1: If an entity purchases ACCUs from a renewable energy provider, why can’t the purchaser account for the ACCUs under IAS 20 Accounting for Government Grants and Disclosure of Government Assistance?

The scope of IAS 20 is limited to the accounting by private sector for-profit entities for government grants and other forms of government assistance. Accordingly, to account for an acquisition of ACCUs under IAS 20, the entity acquiring the ACCUs must have:

- Acquired the ACCUs from a government, government agency or similar body, whether local, national or international, for ‘below market’ consideration, and

- Received the ACCUs from the government entity in return for past or future compliance with certain conditions relating to the activities of the entity.

Despite the purchaser of the ACCUs having previously agreed with the renewable energy provider to acquire the ACCUs, the Clean Energy Regulator will attribute the ACCUs to the renewable energy provider’s Australian National Registry of Emissions Units (ANREU) account in the first instance. This is normally because the renewable energy provider is the registered owner of the facility to which the ACCUs are attributed.

The purchaser is acquiring the ACCUs from an entity other than a government, typically at or near market price for the ACCUs, and is not required to comply with any past or future requirements specified by the government entity regarding the ACCUs.

Therefore, entities acquiring ACCUs from renewable energy providers don’t typically meet the necessary criteria to account for the ACCUs under IAS 20.

Question 2: IAS 20 Accounting for Government Grants and Disclosure of Government Assistance gives a renewable energy provider a choice of accounting for the ACCUs initially at cost or fair value. Are there any reasons why a provider would prefer applying fair value over cost?

Paragraph 23 of IAS 20 states:

“A government grant may take the form of a transfer of a non-monetary asset, such as land or other resources, for the use of the entity. In these circumstances it is usual to assess the fair value of the non-monetary asset and to account for both grant and asset at that fair value. An alternative course that is sometimes followed is to record both asset and grant at a nominal amount.”

As ACCUs are non-monetary in nature, under IAS 20, entities that generate renewable energy or are otherwise entitled to receive ACCUs from the Australian Government have an accounting policy choice with respect to the initial measurement of ACCUs.

As discussed previously, entities that have facilities subject to the Safeguard Mechanism would be expected to initially account for ACCUs they have generated themselves from other parts of their business at fair value, principally to demonstrate to users of their financial statements that they have resources available to meet any obligation arising from their Safeguard Mechanism obligations.

For those entities that generate ACCUs but don’t have any potential Safeguard Mechanism obligations, they may also be inclined to initially account for any ACCUs received at fair value, principally to convey to users the value of the resources available to them.

Question 3: Our previous article noted that renewable energy project developers could sell the resulting ACCUs into the Commonwealth government’s reverse auction process or to other entities. Is this arrangement still available to renewable energy project developers?

Since we prepared that article, a number of changes have been enacted around the Australian Government purchasing ACCUs. In July 2022, the Australian Government appointed an independent panel led by Professor Ian Chubb to review the integrity of ACCUs under the ACCU Scheme. The Final Report of the Independent Review of Australian Carbon Credits was published in December 2022 and comprises 16 recommendations. The Australian Government accepted in principle all 16 recommendations from the review.

Recommendation 3.3 of the Final Report proposed that responsibility for the Australian Government’s purchasing of ACCUs should be moved out of the Clean Energy Regulator and into another Australian Government body to avoid actual or perceived conflicts of interest. Consequently, the Clean Energy Regulator no longer holds ACCU Scheme auctions on behalf of the Commonwealth, and participants can no longer enter into new carbon abatement contracts with the Regulator. The Department of Climate Change, Energy, the Environment and Water is currently implementing the findings of the Independent Review. As part of this process, the Department is considering how ACCU Scheme purchasing processes will be conducted in the future.

While new carbon abatement contracts are not currently available, entities that have active carbon abatement contracts with the Commonwealth Government are able to sell ACCUs to the Government, subject to the terms of their contract. ACCUs can also be sold on the secondary market or to private buyers.

Question 4: What is the difference between an ACCU and a Safeguard Mechanism Credit Unit? Is the accounting for a Safeguard Mechanism Credit Unit different from the accounting for an ACCU?

The Safeguard Mechanism is contained in the National Greenhouse and Energy Reporting Act (2007) and is designed to facilitate Australia’s largest industrial facilities in reducing their greenhouse gas emissions in line with the Australian Government’s target of net zero by 2050. The Safeguard Mechanism currently applies to approximately 215 Australian industrial facilities that emit more than 100 ktCO2-e per annum and requires them to reduce their emissions in line with their individual target baseline emissions. Baselines decline annually by approximately 5%.

Owners of facilities that are subject to the Safeguard Mechanism that exceed their baseline can manage excess emissions in a number of ways, including:

- Acquiring and surrendering ACCUs

- Borrowing emissions from their baseline in the following year, and/or

- Acquiring and surrendering Safeguard Mechanism Credits (SMCs).

Entities subject to the Safeguard Mechanism can generate an SMC by reducing CO2-e emissions to 1 tonne or more below a facility's baseline. Entities can bank SMCs for future compliance needs or sell to other entities under the Safeguard Mechanism. SMCs are held, managed and traded through the Australian National Registry of Emissions Units (ANREU) accounts.

The accounting applied to SMCs should be the same as the accounting applied to ACCUs. Private sector entities awarded SMCs would account for them under IAS 20 Accounting for Government Grants and Disclosure of Government Assistance, which provides an accounting policy choice with respect to the initial measurement of government grants in the form of non-monetary assets at fair value or at a nominal amount. In contrast, an entity that acquires an SMC from another entity subject to the Safeguard Mechanism would initially account for the SMC at cost. Following initial recognition, private sector entities would account for acquired SMCs as inventory under IAS 2 Inventories, or as intangible assets under IAS 38 Intangible Assets, depending on their intended use.

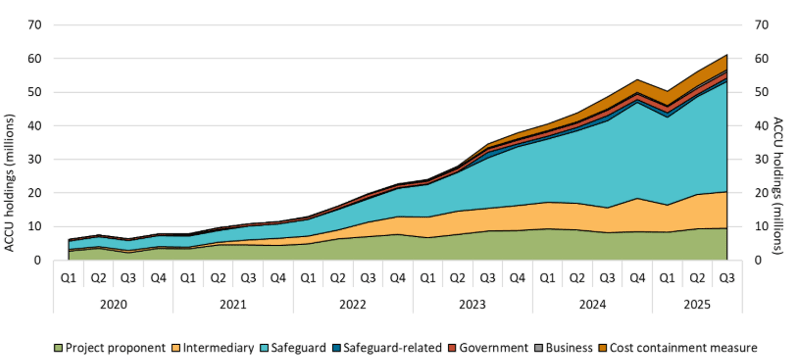

Question 5: Is there any published data on which entities hold ACCUs and for what reason(s)?

The Clean Energy Regulator produces Quarterly Carbon Market Reports, available from its website. Below is an extract from its September 2025 report that provides a summary of the ACCU holdings in the ANREU accounts.

About Figure 1.3

This figure shows ACCU holdings in Australian National Registry of Emissions Units (ANREU) accounts by market participation and the cost containment measure over time.

As is evident from the graph above, over time, the main holders of ACCUs have become entities with Safeguard Mechanism obligations. Next largest holders are intermediaries and entities conducting eligible emission reduction and carbon storage activities (‘project proponents’).

Question 6: What are the differences between Small-scale Technology Certificates and Large-scale Generation Certificates? Do the accounting for Small-scale Technology Certificates and Large-scale Generation Certificates differ?

Small-scale Technology Certificates (STCs) are available to home and business owners to encourage installation of eligible renewable energy systems, including:

- Solar PV

- Solar batteries and water heaters, and

- Air source heat pumps.

One STC is equivalent to 1 megawatt-hour (MWh) of renewable energy production. STCs are saleable on the Australian Energy Exchange (AEX) and the Renewable Energy Certificate Registry (RECR) system to other entities, including those with obligations under the Renewable Energy Target (RET) Scheme obligations.

In contrast, Large-scale Technology Certificates (LGCs) are available to operators of large-scale renewable energy power stations (greater than 100 kW). One LGC is equivalent to 1 megawatt-hour (MWh) of renewable energy production. 1MWh could power anywhere between 250 and 1,000 average Australian homes for an hour, subject to peak energy usage. Typically, LGCs are purchased by electricity and gas retailers, large energy users and other entities that have obligations under the RET Scheme.

Entities with RET Scheme obligations are required to procure and surrender an allocated volume of STCs and/or LGCs to the Commonwealth Government each quarter.

In principle, the accounting for STCs and LGCs doesn’t differ from each other. However, some entities that acquire STCs directly from the Australian Government do not have financial reporting obligations, so may not prepare financial statements in accordance with IFRS® Accounting Standards or Australian Accounting Standards.

Need assistance?

You can find more information about accounting for ACCUs in our webinar. If you need assistance accounting for ACCUs, reach out to our IFRS & Corporate Reporting team for help.