Catching up with IFRS 18 Presentation and Disclosure in Financial Statements

In January, we commenced our 2026 IFRS and Corporate Reporting webinar series with ‘IFRS 18 in plain English – What’s changing and why it matters’, the first of an anticipated ten webinars this year on IFRS 18 Presentation and Disclosure in Financial Statements. For those who were unable to attend, a recording of the IFRS 18 in plain English: What’s changing and why it matters webinar is available.

Over the past decade, the International Accounting Standards Board (IASB) has issued a number of IFRS® Accounting Standards that have profoundly changed accounting practices, including IFRS 9 Financial Instruments, IFRS 15 Revenue from Contracts with Customers and IFRS 16 Leases. While IFRS 18 doesn’t have any measurement implications like the aforementioned standards, we expect it will be at least as impactful as these standards, if not more so. Consequently, we’ve decided to dedicate the majority of our client webinars this year to IFRS 18.

What we covered in January’s IFRS and Corporate Reporting webinar

- Current shortcomings in IFRS Accounting Standards that IFRS 18 seeks to address

- The five income and expense categories and why they matter

- How the five income and expense categories link to mandatory subtotals

- Complexities in applying the new classification requirements and related policy options

- Specified main business activities and their impact on the presentation of profit or loss.

Current shortcomings in IFRS Accounting Standards that IFRS 18 seeks to address

IFRS 18 responds to the following three key concerns expressed by stakeholders to the IASB:

|

Statement of profit or loss: Currently vary from entity to entity in structure and content |

In the notes: Performance measures defined by management are useful, but entities often don’t explain how they are calculated and why they are important |

In both the primary financial statements and the notes: Information should be more appropriately and consistently aggregated and disaggregated |

To address these three key concerns, IFRS 18 includes the following three key changes to the current requirements in IAS 1 Presentation of Financial Statements:

|

In the statement of profit or loss: Report two new defined subtotals – operating profit and profit before financing and income taxes Classify income and expenses into one of five specified categories – based on a new set of classification requirements |

In the notes: Disclose information about some management-defined performance measures (MPMs) |

In both the primary financial statements and the notes: Group items applying enhanced requirements for aggregation and disaggregation of information |

In our January 2026 webinar, we focused on the first group of these changes – the two new defined subtotals and the five specified income and expense categories. The following provides a brief summary of the key points covered.

The five income and expense categories and why they matter

To facilitate more consistent presentations of the statement of profit or loss, both across entities and over time, IFRS 18 introduces five categories of income and expense items and requires entities to classify all income and expense items they recognise into one of these categories in accordance with the principles and guidance provided.

| Investing | Financing | Operating | Income taxes | Discontinued operating |

|---|---|---|---|---|

| Income and expenses are classified in the investing category when they relate to certain assets (i.e. specified assets) | Income and expenses are classified in the financing category when they relate to certain liabilities. Classification depends on whether:

|

Income and expenses are classified in the operating category if they don’t belong in any of the other four categories | Income tax expense and income arising from the application of IAS 12 Income Taxes and any related foreign exchange differences are classified in the income tax category | Income and expenses from discontinued operations arising from the application of IFRS 5 Non-current Assets Held for Sale and Discontinued Operations are classified in the discontinued operations category |

It is important to understand that the purpose of classifying all income and expense items into one of these five categories is not necessarily to provide a subtotal for each category. These categories, particularly the investing, financing and operating categories, work in conjunction with the new subtotals prescribed in IFRS 18 to facilitate entities providing more consistent and comparable presentations of their profit or loss statements.

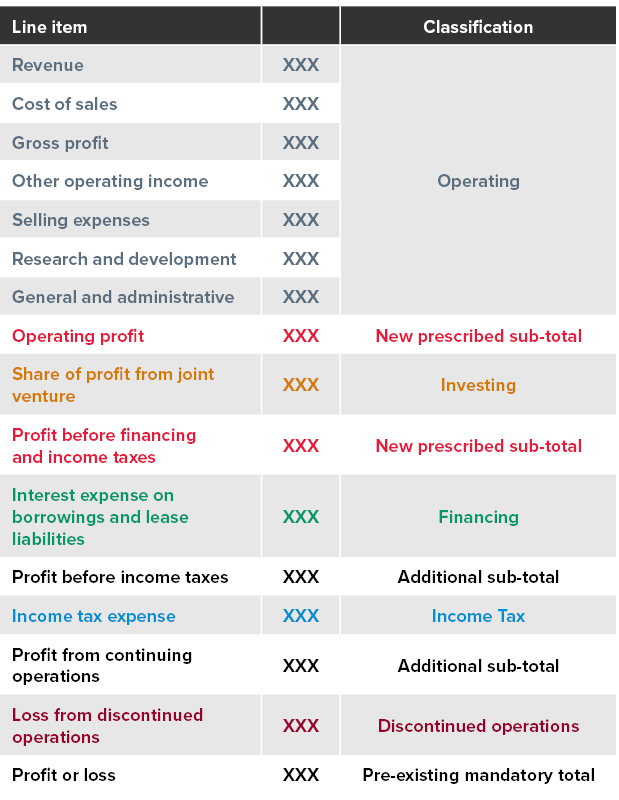

How the five income and expense categories link to mandatory subtotals

IFRS 18 retains three of the prescribed subtotals from IAS 1 - profit before income taxes, profit from continuing operations, and profit or loss - and adds two new ones: operating profit and profit before financing and income taxes. These new subtotals create a more consistent and comparable structure for presenting income and expenses aligned to an entity’s business activities. The diagram below shows how the five categories link to the five defined subtotals.

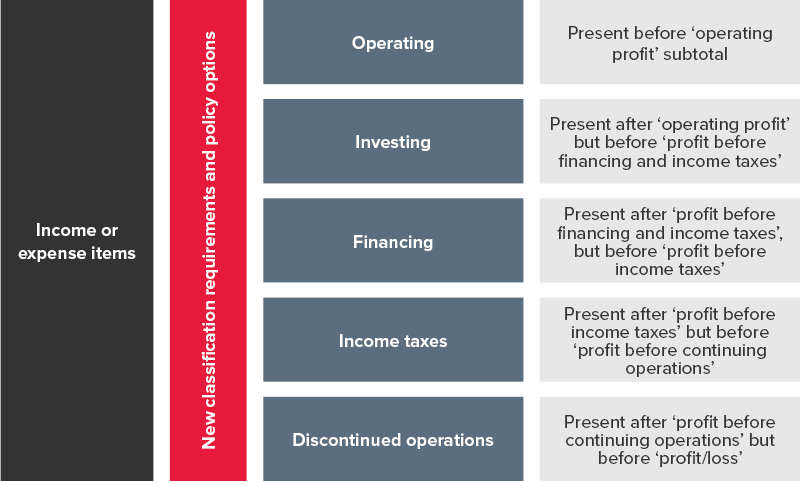

To facilitate consistent, comparable and (most importantly) meaningful presentation of income and expense items, IFRS 18 includes a number of classification requirements and policy options to assist entities in identifying the most appropriate classification for each income and expense item. The following diagram provides a visual representation of the interaction between these new classification requirements and policy options, the five categories and the mandatory sub-totals under IFRS 18.

By applying the new classification requirements and policy options to each income and expense item, an entity can identify the most appropriate classification, which in turn determines where the entity presents the item in its profit and loss statement relative to each of the five mandatory subtotals.

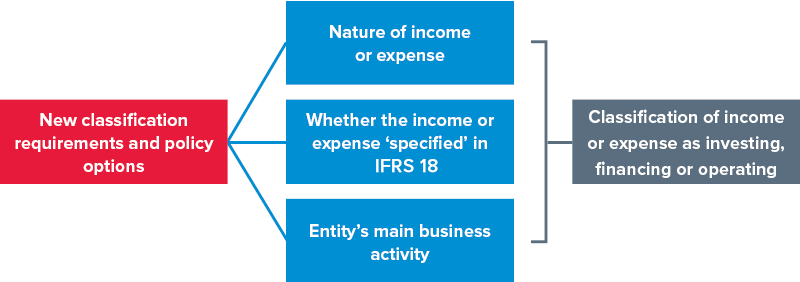

Complexities in applying the new classification requirements and related policy options

As demonstrated in the diagram below, classification of income and expense items between investing, financing or operating categories is based on the following criteria:

- The nature of the income or expense item

- Whether the item is ‘specified’ in IFRS 18, and

- Whether the entity has a specified main business activity, and if so, whether the entity’s specified main business activity is investing in assets, providing finance to customers, or both.

While IFRS 18 is relatively clear on what income or expense is specified for the purpose of classification, for many entities, some judgement may be necessary to determine:

- The nature of some income and expense items, and

- Whether the entity has one, or both, of the specified main business activities.

IFRS 18 recognises that entities will need to exercise judgement in several other areas. For example:

- Foreign exchange differences should be presented in the same profit or loss category as the related income and expenses, unless this would involve undue cost or effort, and

- When services are purchased in a foreign currency on extended credit terms, entities must use their judgement to determine whether the resulting foreign exchange differences relate to the service purchase (operating category) or to the financing element (financing category).

As a result, many entities may require time and analysis to determine the appropriate classifications.

Specified main business activities and their impact on the presentation of profit or loss

IFRS 18 distinguishes between entities with specified main business activities and those without, enabling entities in the former group to present profit or loss in a way that better reflects the nature of their core operations than if they were to apply the general requirements in IFRS 18. The Standard identifies two types of such entities:

- Those that invest in specific types of assets, and

- Those that provide financing to customers.

Entities assessed as having either or both of the specified main business activities may access accounting policy options not available to other entities. For example, entities that borrow funds to provide customer financing must classify the related interest expense as an operating expense. If they also borrow for other purposes, and certain other criteria are met, they may elect to classify the interest expense on those non‑customer borrowings in either the operating or financing category.

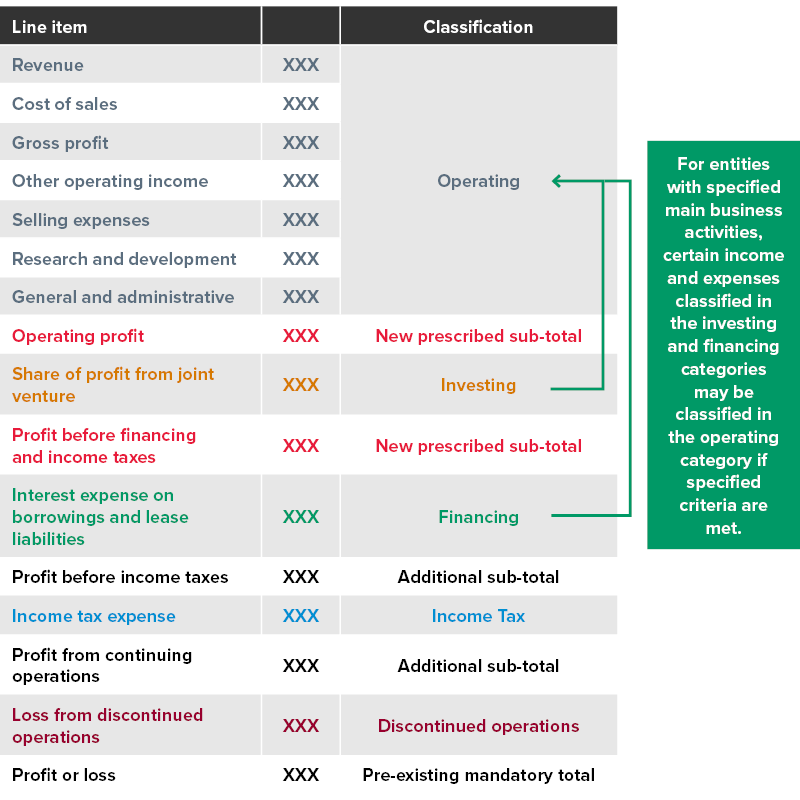

The following diagram demonstrates how having a main business activity can affect the classification of income and expense items across the operating, investing and financing categories.

As noted above, some accounting policy choices under IFRS 18 are not entirely free, as they depend on other requirements or policy decisions within the Standard. These interdependencies between classification rules and policy options further complicate the interpretation and application of IFRS 18.

Looking ahead

Our 2026 IFRS and Corporate Reporting Webinar Series continues with a strong focus on IFRS 18, including upcoming sessions exploring how specified main business activities underpin the new presentation and disclosure requirements.

We will also be announcing a series of IFRS 18 virtual masterclasses, designed to support entities as they transition to the new requirements:

- Transitioning your profit or loss to IFRS 18

- Transitioning your balance sheet and cash flow statement to IFRS 18

- Transitioning your management-defined performance measures.

Each IFRS 18 virtual masterclass will work through practical examples to help clarify the key considerations for implementing IFRS 18. Stay tuned for more details.

Need help?

BDO provides specialist support to entities preparing for audits or developing accounting position papers. Contact BDO’s IFRS & Corporate Reporting team to discuss how we can assist with your IFRS 18 implementations.