Disclosing related party transactions - Who is a related party?

Disclosing related party transactions - Who is a related party?

During the past year, we have been tackling one accounting topic at a time in Corporate Reporting Insights to assist entities with preparing their first general purpose financial statements (GPFS).

Which standard applies?

IAS 24 Related Party Disclosures is the Accounting Standard that identifies related party relationships, and requires various disclosures about related party relationships and related party transactions and balances.

Why is disclosure of related party information important?

Related party relationships can affect the profit or loss and the financial position of an entity because related parties may enter into transactions that unrelated parties would not. For example, related parties may sell goods to one another or provide services that are not on ‘arm’s length’ or normal commercial terms. Profit or loss may be affected even if transactions do not occur. For example, a parent entity may instruct its subsidiary not to deal with a trading partner if it acquires a business that is in direct competition with the former trading partner.

Who is a related party?

A related party is a person or entity that is related to the entity preparing the financial statements (i.e. the reporting entity).

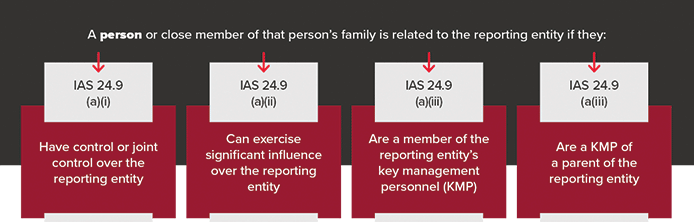

Persons

A person is related to a reporting entity if any of the following apply.

Key management personnel are those persons having authority and responsibility for planning, directing and controlling the activities of the entity, directly or indirectly, including any director (whether executive or otherwise) of that entity.

Source: Definition of ‘key management personnel’ in IAS 24.

A close member of the person’s family is also related to the reporting entity if they have one of the relationships mentioned above. Close members of the person’s family include, but are not limited to:

- The person’s children

- The person’s spouse or domestic partner

- Children of the person’s spouse or domestic partner (i.e. stepchildren)

- Dependants of the person (for example, dependant parents)

- Dependants of the person’s spouse or domestic partner (for example, in-laws).

Sometimes judgement may be required to assess whether a person is a dependant.

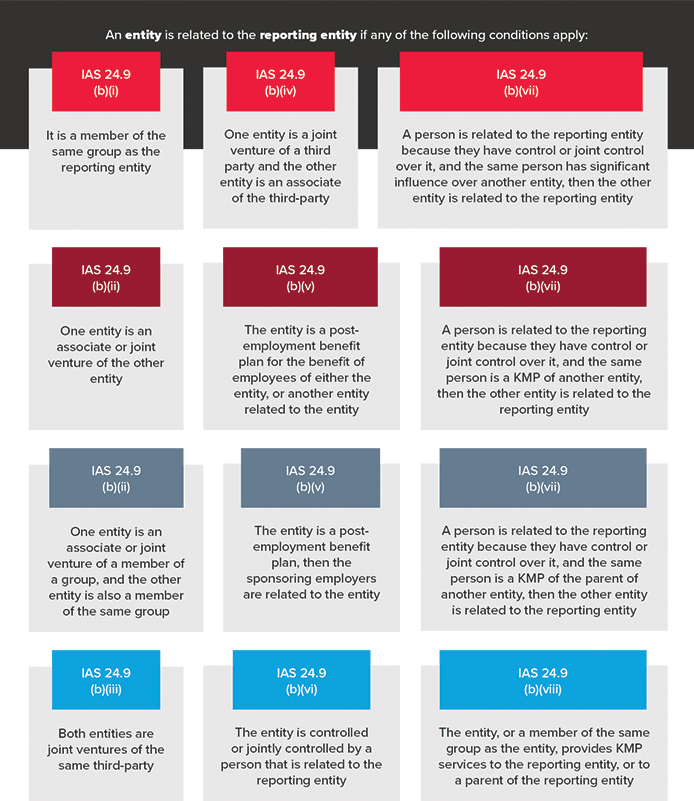

Related entities

It is more complicated to identify related entities under IAS 24 than related persons. An entity is related to another entity if any of the following apply.

Disclosures

The required disclosures for related party relationships and related party transactions are outlined in IAS 24 (full general purpose financial statements) or AASB 1060, paragraphs 189-203 (Simplified Disclosures). Please refer to the standards for specific requirements.

Not-for-profit entities

Not-for-profit entities are required to disclose related party transactions from 2023. They may experience difficulty in applying these definitions to their governance structures and relationships. Please refer to our article, ACNC guidance - Who is a related party?, for more information.

Need assistance?

The above diagram shows that many persons or entities could be related to your reporting entity, and identifying related parties can therefore be a complex process.

BDO’s latest eLearning course provides a step-by-step analysis and examples for each aspect of the related party definition.

If you require assistance with identifying your related party relationships, or preparing your first time related party disclosures, you can contact BDO’s IFRS & Corporate Reporting team.