Diving deeper into IFRS 18: Implementation without a specified main business activity

Diving deeper into IFRS 18: Implementation without a specified main business activity

In March, our 2026 IFRS and Corporate Reporting webinar explored the practical challenges entities will face when implementing IFRS 18 Presentation and Disclosure in Financial Statements, with a specific focus on the investing, financing and operating categories.

This article builds on that discussion and looks more closely at how these categories operate for entities without a specified main business activity. It highlights some of the key distinctions between the five profit or loss categories that will be particularly relevant as entities begin applying IFRS 18 in practice.

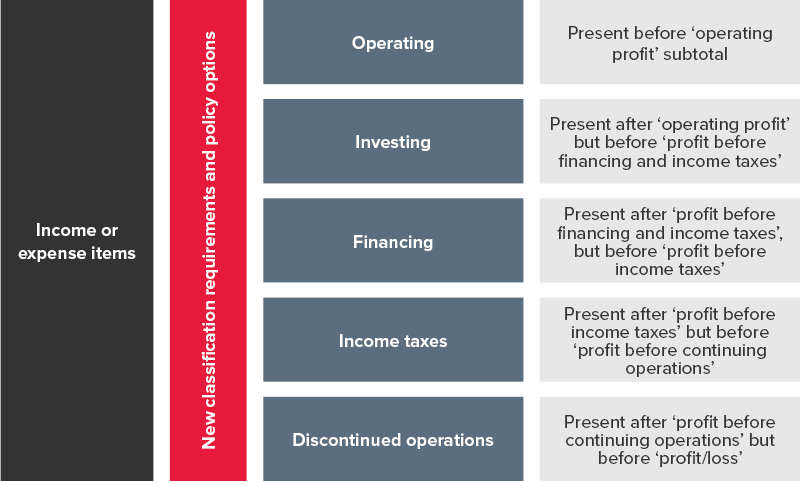

Relationship between the five categories and the presentation of the profit or loss statement

IFRS 18 requires entities to classify all income and expense items into one of five categories identified in the diagram below. Where an entity does not have one or both of the specified main business activities, the general classification requirements apply without modification. In those circumstances, income and expenses are classified based on the descriptions and key features of the categories, and the nature of the relevant income or expense item.

| Investing | Financing | Operating | Income taxes | Discontinued operations |

|---|---|---|---|---|

| Income and expenses are classified in the investing category when they relate to certain assets (i.e. specified assets) | Income and expenses are classified in the financing category when they relate to certain liabilities. Classification depends on whether:

|

Income and expenses are classified in the operating category if they don’t belong in any of the other four categories | Income tax expense and income arising from the application of IAS 12 Income Taxes and any related foreign exchange differences are classified in the income tax category | Income and expenses from discontinued operations arising from the application of IFRS 5 Non-current Assets Held for Sale and Discontinued Operations are classified in the discontinued operations category |

To facilitate consistent classification of income and expense items over time and across entities, IFRS 18:

- Identifies some specific items of income and expense that are required to be classified into each of the five categories (‘specified income and expenses’), and

- Provides application guidance to assist with the classification of the remaining ‘non-specified income and expenses’.

These classification rules, principles and guidance are represented by the red vertical box in the following diagram.

Accordingly, where an entity determines that it doesn’t have either or both of the specified main business activities, it classifies each income and expense item subject to:

- The descriptions and key features of the five income and expense categories, and

- If the income or expense item is ‘specified’ by IFRS 18, the specific requirements that apply to that specified income or expense item, or

- The relevant application guidance applicable to the (non-specified) income or expense item.

The following discussion uses the investment category to demonstrate and explain this classification process more clearly.

Categorising items in the investing category

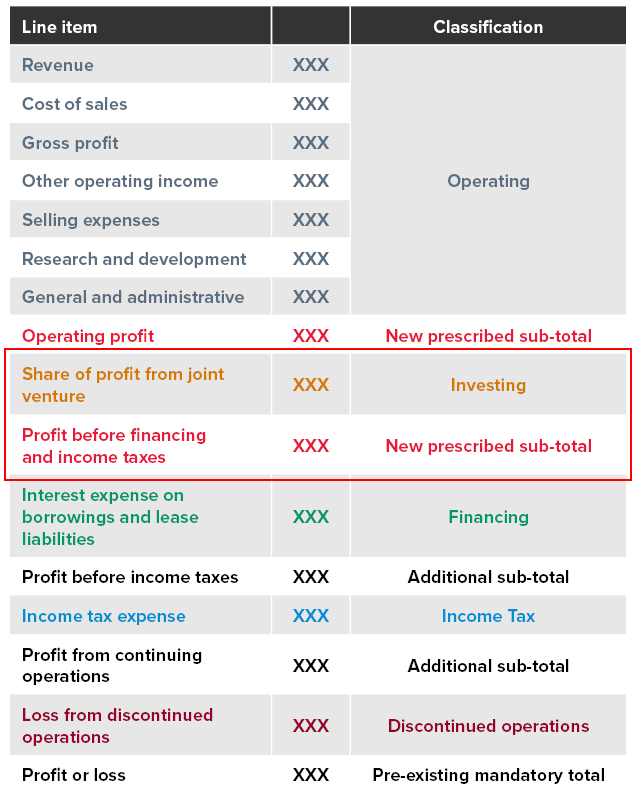

Position of the investing category in the statement of profit or loss

The following diagram shows where all income and expense items categorised in the investing category will be recognised relative to other income and expense items under IFRS 18.

Assets that give rise to income and expenses classified in the investing category

With regards to the investing category, IFRS 18 requires specified income and expense items arising from the following assets (i.e., specified assets) to be categorised in the investing category:

- Investments in associates, joint ventures and unconsolidated subsidiaries

- Cash and cash equivalents, and

- Other assets if they generate a return individually and largely independently of the entity’s other resources.

Assuming an entity has appropriately applied the requirements in the IFRS® Accounting Standards applicable to the items in the first two categories above (i.e., IAS 28 Investments in Associates and Joint Ventures, IFRS 11 Joint Arrangements, IFRS 10 Consolidated Financial Statements and IAS 7 Statement of Cash Flows), it could rely on the classification of those assets in its statement of financial position to identify the related specified income and expense items classifiable in the investing category.

Assets that generate returns independently of other resources

With regards to other assets (i.e., assets that fall within the third category above), entities may need to evaluate their non-specified classes of assets to determine whether they generate a return individually and largely independently of the entity’s other resources.

In some cases, the classification of an asset in the statement of financial position will affect how associated income and expense items are classified under IFRS 18. For instance, buildings classified as either inventory under IAS 2 Inventories or as property, plant and equipment under IAS 16 Property, Plant and Equipment would not typically generate returns individually and largely independently of other resources, as they normally need to be used in conjunction with other assets and activities to generate returns.

In contrast, property classified as investment property under IAS 40 Investment Property can generate returns individually and largely independently of the entity’s other resources through capital appreciation, regardless of whether the property is rented out.

Where accounting policy choices are available for an asset, those choices are not relevant in assessing whether the asset is capable of generating returns individually and largely independently of other resources. However, they do determine the nature of the income and expenses arising from the asset, and therefore the types of income and expense items recognised in the investing category.

For example, investment property accounted for under the cost model in IAS 40 will give rise to recognised capital gains and losses only on disposal (and potentially impairment losses when they arise), whereas investment property accounted for under the fair value model will give rise to fair value gains and losses recognised over the holding period.

To facilitate consistent classification, paragraph B46 of IFRS 18 identifies the following assets as capable of generating returns individually and largely independently of the entity’s other resources:

- Debt or equity instruments, and

- Investment properties and receivables for rent generated by those properties.

Paragraph B48 of IFRS 18 provides further guidance by clarifying that the following assets do not typically generate returns individually and largely independently of other resources:

- Property, plant and equipment, and

- Assets that arise from the production or supply of goods and services for which the related income and expenses are classified in the operating category (for example, trade receivables).

Specified income and expense items classified in the investing category

As noted above, not all income and expenses that relate to specified assets may be classified in the investing category. Paragraphs 54 and B47 of IFRS 18 clarify that the following specified income and expense items arising from the assets identified above are classifiable in the investing category.

|

Income and expense item |

Common examples |

|

Income generated by the asset |

Interest income, dividend income and rental income (as applicable) |

|

Income and expenses that arise from the initial and subsequent measurement of the assets, including on derecognition of the asset |

Depreciation, impairment losses, reversal of impairment losses and fair value gains and losses (subject to the accounting policies applied to the asset under the applicable IFRS Accounting Standard) |

|

The incremental expenses directly attributable to the acquisition and disposal of the asset |

Transaction costs on financial assets classified as fair value through profit or loss and costs to sell assets, such as broker commissions on financial instruments |

Source: BDO IFRS Accounting Standards in Practice – IFRS 18 Presentation and Disclosure in Financial Statements 2025/26 (page 14)

A pictorial explanation of the relationship between specified assets, specified income and expense items and their classification in the investing category is provided in the following diagram.

Illustrative example — equity accounted investments

The application of the above requirements can be demonstrated more clearly using the following practical example.

On 1 January 2028, Entity A acquired 25% of the outstanding shares in (and significant influence over) Entity B. For the annual reporting period ending 31 December 2028, Entity A accounted for its investment in Entity B using the equity method under IAS 28.

During the 2028 annual reporting period:

- Entity B reported an operating profit after tax of $250,000

- Entity B revalued its property, plant and equipment by $40,000 and recognised a corresponding increase in its asset revaluation reserve

- Entity A loaned $100,000 to Entity B. As at the end of the reporting period, Entity B had failed to make all required repayments, resulting in Entity A recognising expected credit losses of $5,000

- Separately, as a consequence of legal proceedings commencing against Entity B, Entity A recognised an impairment loss of $20,000 in respect to its investment.

Applying the relevant requirements in IFRS 18, Entity A concludes that the following income and expense items arising from the equity accounted investment in Entity B are classified in the investing category:

- Share of profit or loss of associates accounted for using the equity method

- Impairment loss of $20,000 in respect to the investment in Entity B, and

- Expected credit loss of $5,000 in respect to the intercompany loan (having determined, in accordance with paragraph B46(a) of IFRS 18, that the loan is capable of generating returns individually and largely independently of other resources).

By contrast, the following items would be classified outside the investing category:

- Interest expense on loans used to finance the acquisition of the investment in Entity B (most likely classified in the financing category), and

- Employee costs incurred in managing the investment (classified in the operating category).

The $40,000 revaluation increment recognised by Entity B is not classified within any profit or loss category under IFRS 18, as it is recognised in other comprehensive income.

Need help?

Preparing for IFRS 18 requires careful judgement, particularly when assessing income and expense items classifiable in the investing category.

We provide specialist support to entities preparing for audits or developing accounting position papers. Contact BDO’s IFRS & Corporate Reporting team to discuss how we can assist with assessing business activities, developing accounting policies and implementing IFRS 18 requirements.

We are also conducting a series of IFRS 18 virtual masterclasses to support entities with key aspects of transition during 2026. These sessions focus on practical implementation considerations and worked examples.