Need only disclose material accounting policy information for Simplified Disclosures

Need only disclose material accounting policy information for Simplified Disclosures

In March 2021 Accounting News we noted that users of financial statements should expect to see a reduction in the amount of accounting policy disclosures as a result of amendments to IAS 1 Presentation of Financial Statements and IFRS Practice Statement 2 Making Materiality Judgements.

What does this mean for entities preparing general purpose financial statements using Simplified Disclosures?

AASB 1060 General Purpose Financial Statements – Simplified Disclosures for For-Profit and Not-for-Profit Tier 2 Entities, as initially drafted, required disclosure of all significant accounting policies, but recent amendments align accounting policy disclosures with the changes to IAS 1 discussed above (refer to AASB 2021-6 Amendments to Australian Accounting Standards - Disclosure of Accounting Policies: Tier 2 and Other Australian Accounting Standards for more information).

What accounting policy information is expected to be material?

If an entity has a material transaction, it does not automatically follow that an accounting policy should be disclosed.

Accounting policy information is expected to be material if users of an entity’s financial statements would need it to understand other material information in the financial statements.

Extract of IAS 1, paragraph 117B

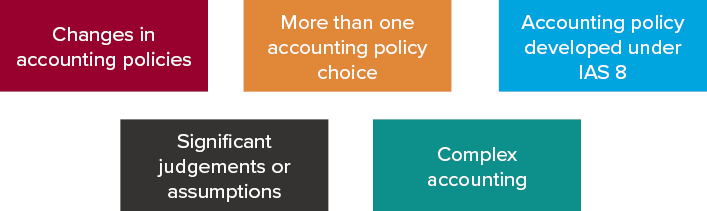

For example, accounting policy information is likely to be material if the information relates to material transactions, other events or conditions, and:

- The entity changed its accounting policy during the period, resulting in a material change to information reported in the financial statements

- The entity chose the accounting policy from one or more options permitted under IFRS (e.g. measuring investment property at historical cost or fair value)

- The accounting policy was developed applying the hierarchy in IAS 8 Accounting Policies, Changes in Accounting Estimates and Errors because there is no specific IFRS dealing with the transaction

- The entity was required to make significant judgements or assumptions in applying the accounting policy, and these judgements or assumptions have been disclosed as required by IAS 1, paragraphs 122 or 125, or

- The accounting is complex and users would otherwise not understand the material transaction (for example, if more than one IFRS standard applies to the transaction).

More information

For more information to assist with deciding whether accounting policy information is material, please refer to the following resources:

- Accounting News article ‘Expect to see a reduction in the amount of accounting policy disclosures’ (March 2021)

- International Financial Reporting Bulletin IFRB 2021 07 IASB issues amendments to IAS 1, IAS 8 and IFRS Practice Statement 2 – Disclosure of Accounting Policies and Definition of Accounting Estimates.

Need help?

BDO’s IFRS & Corporate Reporting team is here to help if you require assistance streamlining your accounting policies, converting them to plain English, and making them entity-specific. Please contact us if you require assistance.