IFRS 18 requires detailed disclosure about management-defined performance measures in the financial statements

In addition to changing the way income and expenses are classified in the statement of profit or loss, IFRS 18 Presentation and Disclosure in Financial Statements, the new financial statements presentation standard that replaces IAS 1 Presentation of Financial Statements, also requires extensive disclosure about management-defined performance measures.

What is a management-defined performance measure (MPM)?

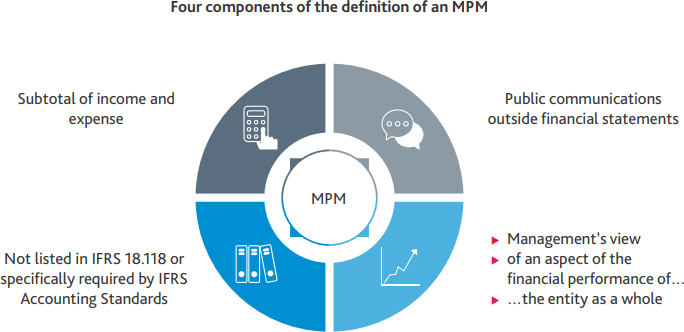

A management-defined performance measure (MPM) is a subtotal of income and expenses that:

- An entity uses in public communications outside financial statements

- An entity uses to communicate to users of financial statements management’s view of an aspect of the financial performance of the entity as a whole, and

- Is not listed in paragraph 118 of IFRS 18 or specifically required to be presented or disclosed by Australian Accounting Standards.

There are four components to an MPM, shown in the diagram below:

Source: BDO IFRS Accounting Standards in Practice IFRS 18 Presentation and Disclosure in Financial Statements 2025/2026, page 109

We discuss each component in more detail below.

Public communications outside the financial statements

To meet the definition of an MPM, a subtotal of income and expenses must be included in public communications outside financial statements. IFRS 18 does not define public communications, but it provides a non-exhaustive list of what public communications would be considered to be included or excluded from this definition. This is shown below.

|

Modes of communication |

|

|

Included in public communications |

Excluded from public communications |

|

Management commentary |

Oral communications |

|

Press releases |

Written transcripts of oral communications |

|

Investor presentations |

Social media posts |

IFRS 18 does not specify whether regulatory filings that are available to the general public are considered public communications. However, in our view, if a particular regulatory filing is available to users without requiring approval from the entity or the regulatory authority, it would be considered to be public communication. We also believe that such filings constitute public communications, even if the user must pay a fee to access them.

Subtotals of income and expenses

To meet the definition of an MPM, the measure must relate to subtotals of income and expenses. Other subtotals that are not simply subtotals of income and expenses are not MPMs. Examples of measures that are not subtotals of income and expenses are ‘adjusted cash flow’ measures, debtor turnover ratios, etc. Accordingly, detailed MPM disclosures are not required for these measures.

Examples of measures that are not MPMs because they are not subtotals of income and expenses

The following are examples of measures that are not MPMs because they are not subtotals of income and expenses:

|

Nature |

Example |

|

Subtotals of only income or only expenses |

|

|

Assets, liabilities, equity or a combination of these elements |

|

|

Financial ratios (note, however, a numerator or denominator of a financial ratio that is a subtotal of income and expenses may be an MPM – see below) |

|

|

Measures of liquidity or cash flows |

|

|

Non-financial performance measures |

|

What if the numerator or denominator in a financial ratio is a subtotal of income and expenses?

While financial ratios themselves are not MPMs because they are not a subtotal of income and expenses, a numerator or denominator in a financial ratio that is a subtotal of income and expenses could be an MPM if all four components are present. An example of this is ‘adjusted operating profit per share’, which is calculated as ‘adjusted operating profit’ divided by the number of shares outstanding.

Adjusted operating profit per share is not an MPM because it is not a subtotal of income and expenses, but ‘adjusted operating profit’ (the numerator) is a subtotal of income and expenses and therefore, the disclosure requirements for MPMs apply to ‘adjusted operating profit’ as the numerator.

Must the subtotal of income and expenses always be presented in the statement of profit or loss?

While an MPM must be a subtotal of income and expenses, it may not always be presented in the statement of profit or loss because various adjustments may be made to existing subtotals. For example, entities may communicate subtotals such as ‘adjusted profit’ or operating profit excluding recurring items, etc. outside the financial statements.

So, while an MPM must be a subtotal of income and expenses, it does not have to appear as a subtotal in the statement of profit or loss.

Not listed in paragraph 118 nor specifically required by an IFRS® Accounting Standard

Some subtotals are not defined by IFRS Accounting Standards, but are commonly used in financial statements and are well understood by users. IFRS 18 therefore excludes these from the scope of the detailed MPM disclosures:

- Gross profit or loss (revenue minus cost of sales) and similar subtotals

- Operating profit or loss before depreciation, amortisation and impairments within the scope of IAS 36 Impairment of Assets

- Operating profit or loss and income and expenses from all investments accounted for using the equity method

- For an entity that provides financing to customers and applies the accounting policy choice of classifying income and expenses from liabilities that do not relate to the provision of financing to customers in the operating category, a subtotal comprising operating profit or loss and all income and expenses classified in the investing category

- Profit or loss before income taxes

- Profit or loss from continuing operations.

Additional subtotals in the statement of profit or loss that are not required by IFRS Accounting Standards are likely to be MPMs.

In some cases, a subtotal of earnings before interest, taxation, depreciation, and amortisation (EBITDA) may be considered an MPM, and in others, it may not. EBITDA is usually determined as net income before taxation, with interest, depreciation and amortisation added back.

Under paragraph 118(b), a subtotal for ‘operating profit or loss before depreciation, amortisation and impairments within the scope of IAS 36’ is not an MPM. To meet this exclusion, an entity would essentially need to have no income and expenses classified in the investing or financing categories, and no other adjustments to EBITDA for the EBITDA measure to equate to ‘operating profit or loss before depreciation, amortisation and impairments within the scope of IAS 36’.

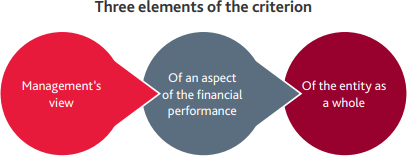

Management’s view of an aspect of the financial performance of the entity as a whole

The fourth component of the MPM requirements is whether entity uses the subtotal of income and expenses to communicate to users of the financial statements management’s view of an aspect of the financial performance of the entity as a whole. There are three elements to this:

Source: BDO IFRS Accounting Standards in Practice IFRS 18 Presentation and Disclosure in Financial Statements 2025/2026, page 113

Management’s view

The purpose of the MPM disclosures is to provide users with information to understand management’s view of the entity’s financial performance.

Rebuttable presumption

IFRS 18 contains a rebuttable presumption that a subtotal of income and expenses used in public communications outside financial statements communicates to users of financial statements management’s view of an aspect of the financial performance. However, the rebuttable presumption is not intended to bring in a large number of subtotals as MPMs. Instead, it provides an objective way for an entity to determine which measures it communicates publicly should be disclosed as MPMs in the financial statements.

An entity can rebut the presumption if it has reasonable and supportable information demonstrating that both of the following criteria are met.

| Criteria |

Examples to demonstrate instances where each criterion could be met |

|

The subtotal does not communicate to users of financial statements management’s view of an aspect of the financial performance of the entity as a whole. |

|

|

The entity has a reason for using the subtotal in its public communications other than to communicate management’s view of an aspect of the financial performance of the entity as a whole. |

|

There is no need to disclose the fact that the presumption has been rebutted.

Subtotals communicated without prominence

It is a matter of judgement whether a subtotal is communicated without prominence. Examples of factors to consider when exercising this judgement are shown below.

|

Example of factors to consider |

Demonstrates prominence |

Demonstrates lack of prominence |

|

The extent of references to the subtotal |

Numerous references |

Few references |

|

The content of commentary or analysis about or relying on the subtotal |

|

A description of the subtotal as information that does not communicate management’s view, and the subtotal is provided only in response to frequent requests from some users. |

Subtotals not used internally

Sometimes, an entity might adjust the subtotal communicated in public communications for use internally by management. The entity must apply judgement to assess whether the subtotal it uses internally is sufficiently similar to the subtotal used in its public communications. The more similar the subtotals are, the more likely it is that the subtotal used in the entity’s public communications conveys to users of financial statements management’s view of an aspect of the financial performance of the entity as a whole.

A subtotal used only internally by management does not meet the definition of an MPM as it is not used in public communications.

Change in an entity’s use of a subtotal

An entity might change its use of a subtotal to communicate to users of its financial statements management’s view of an aspect of the financial performance of the entity as a whole, thereby making a subtotal an MPM or ceasing to be one. For example, Entity A began using a subtotal in its public communications in response to frequent requests from some users. At that time, the subtotal did not reflect management’s view of an aspect of the entity’s financial performance and the presumption about communicating management’s view was rebutted. After a period of time, management started using the measure to internally assess and monitor the entity’s financial performance. As a result, the externally published measure meets the definition of an MPM.

An aspect of the financial performance of the entity

Judgement may be needed to determine whether a measure communicates management’s view of an aspect of the entity’s financial performance.

Financial performance of the entity, not management’s performance

The focus of MPM’s is on communicating management’s view of an aspect of the entity's performance, not management’s performance. Subtotals used only to assess management’s performance, for example, a measure used internally to determine management remuneration, would not meet the definition of MPMs. However, where these measures are also communicated externally to communicate management’s view of an aspect of the entity’s performance, they would be considered MPMs.

Entity as a whole

The definition of an MPM requires the measure to communicate management’s view of an aspect of the financial performance of the entity as a whole. Some measures do not relate to the entity’s overall financial performance, but rather to an element of it. These measures are not MPMs because an MPM must relate to an aspect of the financial performance of the entity as a whole. The following provides contrasting examples:

- XYZ Group, using a performance measure of ‘profit or loss before non-recurring expenses and non-recurring income’ in its public communications, communicates management’s view of an aspect of the financial performance of XYZ Group as a whole, since it excludes non-recurring income and expenses from profit or loss for the entire group. This would meet the definition of an MPM

- XYZ Group presenting a measure of ‘profit or loss before non-recurring expenses’ of Subsidiary S does not relate to an aspect of the financial performance of XYZ Group as a whole, and would therefore not be expected to meet the definition of an MPM, although this requires the exercising of judgement.

Judgement may be required to assess whether the measure provides information about an aspect of the entity’s financial performance as a whole.

Are the subtotals of income and expenses for reportable segments related to the reportable segments?

Usually, subtotals for an individual segment’s income and expenses do not provide information about an aspect of the financial performance of the entity as a whole and would therefore not be MPMs. However, if a subtotal relates to a segment that contains only one main business activity and is presented separately in the statement of profit or loss, the subtotal would meet the definition of an MPM, provided the other criteria are met (IFRS 18.B115).

Can the entity provide ‘voluntary MPM disclosures’?

An entity is not prevented from including the MPM disclosures for measures that are not subtotals of income and expenses, provided they are:

- Are labelled in a way that clearly distinguishes the ‘voluntary’ disclosures from the mandatory ones, i.e. they should be labelled as not being MPMs

- Complete and do not present the voluntary measures in a selective or biased manner.

Do private entities also have to provide MPM disclosures?

The intention of the MPM disclosures is to provide transparency and discipline over performance measures communicated to users outside financial statements. This applies regardless of whether the entity is private or public.

Therefore, there is no exemption for private entities from providing MPM disclosures. However, many private entities do not make public communications outside of financial statements and so won’t be impacted by these new disclosures.

More information

You can find more articles about IFRS 18 challenges on our IFRS 18 topic page. Additionally, our publication and webinars will help you on your IFRS 18 implementation journey.

Need help

Our recent articles on IFRS 18 demonstrate the complexity of applying IFRS 18 in practice. Reach out to our team of experts for assistance with understanding the latest requirements in IFRS 18.