Large wholly-owned subsidiaries lose lodgement relief if parent entity fails to lodge group financial statements on time

Large proprietary companies must generally lodge audited financial statements with the Australian Securities and Investments Commission (ASIC) within four months of the end of the reporting period.

Exceptions

If a wholly-owned subsidiary is party to a deed of cross guarantee with its parent entity, it may be relieved from its lodgement obligations if it meets all the conditions in ASIC Corporations (Wholly-owned Companies) Instrument 2016/785 (LI 2016/785). Please refer to Part 2, section 6 of (LI 2016/785) for full details of these conditions.

Parent entity must lodge consolidated financial statements

For wholly-owned subsidiaries to obtain financial reporting relief, one of the conditions is that the parent entity must lodge consolidated financial statements with ASIC within the following timeframes:

- Three months (if the parent entity is a disclosing entity)

- Four months (if the parent entity is an unlisted public company or a large proprietary company).

What happens if the parent entity lodges late or fails to lodge?

If the parent entity does not lodge consolidated financial statements within the timeframes set out above, all LI 2016/785 conditions for relief have not been met, and the relief provided in section 5 of LI 2016/785 never applies for that financial year. For each wholly-owned subsidiary, this means:

- It must prepare a financial report and a directors’ report for the financial year

- The financial report must be audited, and

- The financial report must be sent to members

- The financial report must be tabled at the AGM (if the entity is required to hold an AGM, such as an unlisted public company).

Is there a grace period for subsidiaries to lodge their financial statements late?

There is no grace period to provide extra time for wholly-owned subsidiaries to prepare and lodge their audited financial statements with ASIC, as LI 2016/785 provides no cure or extension in these circumstances. In other words, LI 2016/785 does not deem the subsidiary to be complying simply because the parent eventually lodges late.

What does this mean in practice?

If the parent entity fails to lodge its consolidated financial statements on time, for wholly-owned subsidiaries relying on the relief in LI 2016/785, this typically means:

- They will have to prepare and lodge their own audited financial statements as soon as the failure is identified

- They will be subject to late lodgement fees and potential ASIC compliance action.

Example

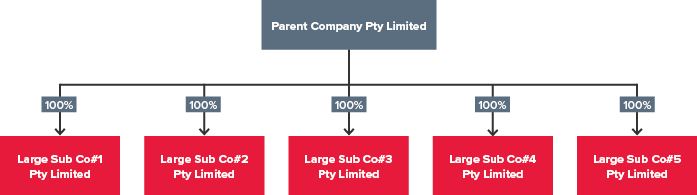

Assume the following group structure. All entities are incorporated in Australia.

Parent Company Pty Limited has five Australian wholly-owned subsidiaries (all large proprietary companies). All six group entities have entered into a deed of cross-guarantee.

Parent Company Pty Limited wishes to apply the relief in LI 2016/785 so that its five large wholly-owned subsidiaries do not have to prepare and lodge separate financial reports.

The year-end of all six entities is 31 December 2025.

To obtain financial reporting relief for the five wholly-owned subsidiaries, Parent Entity Pty Limited must lodge audited consolidated financial statements with ASIC no later than 30 April 2026.

If Parent Entity Pty Limited fails to lodge these on time by 30 April 2026, all five wholly-owned subsidiaries must lodge individual audited financial statements. Large SubCo#1 Pty Limited, Large SubCo#2 Pty Limited, Large SubCo#3 Pty Limited, Large SubCo#4 Pty Limited and Large SubCo#5 Pty Limited must, therefore, prepare and lodge audited financial statements with ASIC as soon as possible in order to minimise penalties for late lodgement.

If Parent Entity Pty Limited anticipates that it is likely to miss the 30 April 2026 deadline, the five wholly-owned subsidiaries must prepare and lodge individual audited financial statements by 30 April 2026.

Can Parent Company Limited apply financial reporting relief for subsidiaries in future years?

Yes, but it may have to effectively ‘start again’, ensuring that all conditions in section 6 of LI 2016/785 are met. For example, as Parent Company Pty Limited would not have relied on the relief during the prior year, it must lodge an ‘opt-in notice’ with ASIC again. The opt-in notice must:

- Be signed by a director or secretary

- Be lodged with ASIC using Form 389 Opt-in/change of holding entity notice by wholly-owned company relieved from financial reporting obligations

- Contain a statement that the company has taken advantage of the relief under LI 2016/785

- Identify the holding company

- Be lodged before the lodgement deadline (i.e. for the year ended 31 December 2026, this will be 30 April 2027).

Don’t forget disclosure in the consolidated financial report when the wholly-owned subsidiary reporting relief applies

In addition to preparing consolidated financial statements for the group, the parent entity must include the following disclosures in the notes to the financial statements (refer to Part 2, section 6(v) of LI 2016/785 for more details):

- A brief explanation of what the deed of cross guarantee is and what it does

- A list of all entities that were parties to the deed at the end of the financial year, clearly showing which entities are part of the closed group, and which are part of the extended closed group

- Details (with dates) of any changes to the deed during or since the financial year, including entities added, removed, and entities sold or disposed of

- Details (with dates and reasons) of any entities that qualified for relief under LI 2016/785 last year but do not qualify in the current year

- If the consolidated financial statements include entities that are not in the closed group - additional consolidation information showing only the closed group entities (after eliminating all transactions between members of the closed group)

- If the consolidated financial statements include entities that are not parties to the deed of cross guarantee, additional consolidation information showing only the parent entity and the controlled entities that are parties to the deed (after eliminating all transactions between parties to the deed of cross guarantee)

- If any entities that are parties to the deed are not controlled by the parent entity (excluding trustees that are not group entities), additional consolidation information for those entities, either individually or combined.

Also, the directors’ declaration of the parent entity must state whether, at the date of the document, there are reasonable grounds to believe that the members of the extended closed group will be able to meet any liabilities to which they are, or may become, subject because of the deed of cross guarantee.

Need assistance?

Please contact our IFRS & Corporate Reporting team if you would like further information, or if you require assistance with any financial reporting matters.