NFPs: Find your appropriate financial reporting framework

NFPs: Find your appropriate financial reporting framework

On 21 April 2026, the Australian Accounting Standards Board approved its ‘Tier 3’ standard, AASB 1061 General Purpose Financial Statements – Not-for-Profit Private Sector Tier 3 Entities. AASB 1061 requires smaller not-for-profit (NFP) private sector entities to prepare general purpose financial statements (GPFS) applying simpler recognition, measurement and disclosures. The application date is for periods beginning on or after 1 July 2029, with early application permitted.

The new ‘Tier 3’ standard does not mandate which smaller NFPs can apply it as a basis for preparing GPFS. Instead, it relies on legislators such as the Australian Charities and Not-for-profits Commission (ACNC) and the Treasury to amend the Australian Charities and Not-for-profits Commission Act 2012 and the Corporations Act 2001, respectively.

Despite the early adoption option, at the time of writing, AASB 1061 is yet to be published on the AASB website. Even if it is published prior to NFPs finalising their 30 June 2026 financial statements, we don’t recommend applying this until legislators clarify which entities can use it. This article, therefore, summarises the current state (status quo) and requirements for NFPs reporting under current legislation for 30 June 2026.

With limited exceptions, most for-profit private sector entities required to prepare financial statements in accordance with Australian Accounting Standards must prepare GPFS. However, NFPs can still prepare special purpose financial statements (SPFS) in some circumstances, but the rules are confusing.

This article will help you assess which reporting framework is appropriate for you, depending on whether your NFP is:

- Registered with the ACNC

- Not registered with the ACNC but is a company limited by guarantee required to prepare financial statements in accordance with Part 2M.3 of the Corporations Act 2001

- Is not registered with the ACNC and is not a CLBG, but is required by other legislation, a contract or an agreement to prepare financial statements

- Has no mandatory reporting requirements (unless specifically requested by a member).

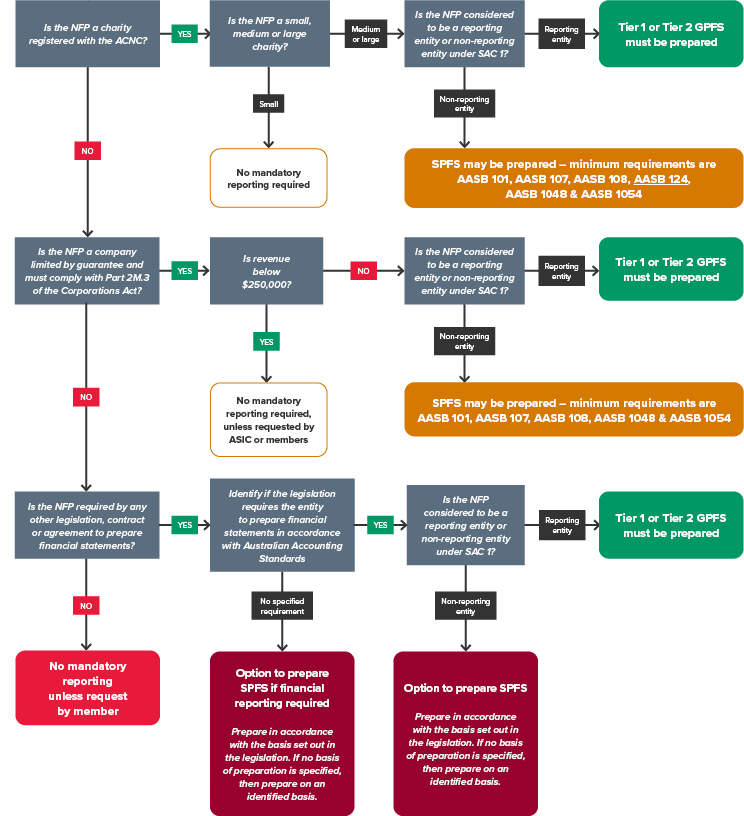

These four scenarios are shown in the decision tree below.

Charities registered with the ACNC

The reporting requirements for a charity registered with the ACNC depend on whether it is small, medium or large, as defined in section 205-25 of the Australian Charities and Not-for-profits Commission Act 2012. The size test depends on the charity’s revenue from its ordinary activities. The ACNC provides guidance on determining revenue.

|

Size of charity |

Required to prepare a financial report? |

Revenue threshold |

Audit/review requirement |

|

Small |

No. Optional to prepare and submit a financial report to the ACNC (Cash or accrual basis of accounting permitted) |

Less than $500,000 |

None |

|

Medium |

Yes. Must prepare and submit a financial report to the ACNC (Accrual basis of accounting) |

$500,000 to $3 million |

Review or optional audit |

|

Large |

Yes. Must prepare and submit a financial report to the ACNC (Accrual basis of accounting) |

Greater than $3 million |

Audit |

Medium and large charities – SPFS or GPFS?

As noted in the table above, medium and large charities must prepare financial statements for the ACNC applying an accrual basis of accounting. However, the question remains:

Must they prepare GPFS (and if so, Tier 1 or Tier 2), or will SPFS suffice?

The decision tree above notes that medium and large charities must determine whether they are a reporting entity or a non-reporting entity under SAC 1 Definition of the Reporting Entity:

- Reporting entities: Must prepare GPFS, and as charities are seldom publicly accountable, they can prepare financial statements applying the Simplified Disclosures (Tier 2)

- Non-reporting entities: Can prepare SPFS, applying as a minimum AASB 101 Presentation of Financial Statements, AASB 107 Statement of Cash Flows, AASB 108 Accounting Policies, Changes in Accounting Estimates and Errors and AASB 1054 Australian Additional Disclosures. Related party disclosures are also required, as are key management personnel (KMP) compensation disclosures for large charities with more than one KMP.

Companies limited by guarantee (CLBG) that are not registered with the ACNC

Small CLBGs with revenue of $250,000 or less have no financial reporting obligations. However, medium and large CLBGs (i.e. those with revenue greater than $250,000 or those that are not deductible gift recipients) must prepare financial statements in accordance with Australian Accounting Standards and lodge them with the Australian Securities and Investments Commission (ASIC). The audit or review requirements depend on whether the CLBG is:

- Large (revenue exceeds $1 million): An audit

- Medium (revenue is less than $1 million and the CLCG is not small): A review.

Medium and large CLBG – SPFS or GPFS?

Similar to the rules for charities registered with the ACNC, and noted in the above decision tree, medium and large CLBGs must determine whether they are a reporting entity or a non-reporting entity under SAC 1 Definition of the Reporting Entity:

- Reporting entities: Must prepare GPFS; usually, these would be Tier 2 (Simplified Disclosures)

- Non-reporting entities: Can prepare SPFS, applying as a minimum AASB 101, AASB 107, AASB 108 and AASB 1054 (noting that related party disclosures are not required).

Required by other legislation, a contract or an agreement to prepare financial statements

The requirement for incorporated associations, co-operatives and other types of NFP structures to prepare financial statements is usually driven by state-based legislation, which can differ significantly from one state to another. These types of NFPs must determine if Australian Accounting Standards are required, and if so, whether the entity is a reporting entity or a non-reporting entity under SAC 1 Definition of the Reporting Entity:

- Reporting entities: Must prepare GPFS; usually, these would be Tier 2 (Simplified Disclosures)

- Non-reporting entities: Can prepare SPFS, applying the basis set out in the legislation, or if no basis is specified, as per the accounting policies in Note XX.

If no basis is identified, there is no requirement to apply as a minimum AASB 101, 107, 108 and 1054.

In some cases, a contract or an agreement (e.g. a banking agreement) may specify the type of financial statements. If Australian Accounting Standards are required, the same reporting entity vs non-reporting entity assessment described here is applied.

No mandatory reporting requirements (unless specifically requested by a member)

If the NFP is not a charity registered with the ACNC or a CLBG and it does not have financial reporting obligations specified in other legislation, a contract or an agreement, then no financial statements are required unless requested by members. In such cases, the NFP must refer to the member’s request to determine the appropriate financial reporting framework.

Need assistance?

Please contact our IFRS & Corporate Reporting team if you require assistance with deciphering your financial reporting requirements for your NFP.