Simplified accounting for private sector not-for-profit Tier 3 entities

Simplified accounting for private sector not-for-profit Tier 3 entities

Our October 2022 Corporate Reporting Insights article noted that the Australian Accounting Standards Board (AASB) is proposing simplified accounting for a new ‘Tier 3’ category of not-for-profit (NFP) private sector entity, and answers various questions regarding the scope and application of these simplified requirements. Currently these entities must follow all the complex recognition, measurement and disclosure requirements of Australian Accounting Standards that apply to larger Tier 1 and Tier 2 for-profit entities.

Primary financial statements

Firstly, the Discussion Paper proposes that Tier 3 financial statements should consist of:

- A statement of profit or loss and other comprehensive income

- A statement of financial position

- A statement of cash flows, with operating activities presented using the direct method, but preparers will not need to show cash flows from investing activities separately from financing activities.

The AASB has not yet decided whether a statement of changes in equity will be required as part of a complete set of financial statements for Tier 3 NFP private sector entities.

Fair value

Wherever fair value is referred to for Tier 3 simplified accounting, the AASB is also proposing that the principles contained in AASB 13 Fair Value Measurement must be applied. Cost can be used as an approximation of fair value for unlisted share investments when there is insufficient recent information to measure fair value.

Simplified accounting

The ‘big ticket’ areas where the AASB is proposing simplified accounting include:

- Consolidation

- Non-financial assets acquired at significantly less than fair value

- Impairment of non-financial assets

- Leases

- Employee benefits

- Income

- Financial instruments

- Accounting policies, errors and changes in accounting estimates

- Borrowing costs

- Intangible assets.

These are discussed in more detail below.

Consolidation not required

Some NFPs find it difficult to prepare consolidated financial statements because it can be a complex process to identify entities over which it has control (subsidiaries). From a cost-benefit perspective, the AASB is therefore proposing that a parent entity can choose to prepare either:

- Consolidated financial statements, or

- Separate financial statements, with information about the parent entity’s significant relationships.

If preparing separate financial statements, interests in subsidiaries can be measured at either cost, fair value through other comprehensive income, or using the equity method of accounting.

Non-financial assets acquired at significantly less than their fair value

If a NFP is gifted an asset for no consideration, or it acquires a non-financial asset for consideration which is significantly less than fair value, AASB 1058 Income of Not-for-Profit Entities requires them to recognise these assets in accordance with Australian Accounting Standards applicable to those assets, which usually require measurement at fair value. In practice, it may be costly for NFPs to obtain a fair valuation for assets that complies with AASB 13. The proposed approach is:

- Inventory

For donated inventory, the AASB is therefore proposing an accounting policy choice. NFPs will be able to choose to initially measure donated inventory, or inventory acquired at significantly less than fair value, at either cost or current replacement cost.

- Other non-financial assets (excluding peppercorn leases)

For non-financial assets other than inventory, such as motor vehicles, furniture, and property acquired at significantly less than fair value, the AASB is proposing an accounting policy choice of cost or fair value. For example, where the fair value of a gifted second-hand motor vehicle is easy to obtain, the entity may choose to measure it at fair value. However, obtaining valuations for other types of assets may be costly and the entity can choose to recognise those at cost.

Impairment of non-financial assets

Tier 3 entities have to apply the same impairment testing requirements as Tier 1 and Tier 2 entities which are contained in AAS 136 Impairment of Assets. However, the AASB is proposing to simplify the rules about when these entities must conduct an impairment test. An impairment test will only be required for non-financial assets measured at cost or deemed cost:

- If an asset has been physically damaged, or

- When its service potential has been adversely affected.

The Discussion Paper also notes that Tier 3 requirements would include a rebuttable presumption that fair value less costs of disposal is expected to be the most appropriate measure of a non-financial asset’s recoverable amount.

Leases

In another cost-saving measure for NFPs, the AASB is proposing to keep lease accounting off-balance sheet.

Tier 3 entities that enter into leases as lessee will be able to keep the leases off-balance sheet. Instead of capitalising leases in accordance with AASB 16 Leases, NFP lessees will be able to expense lease costs on a straight-line basis unless another systematic basis is appropriate.

A corresponding requirement would apply to lessors.

Right-of-use assets will also not be recognised for concessionary leases. Currently Tier 1 and Tier 2 NFPs recognise a right-of-use asset at its cost or fair value.

Employee benefits

Many NFPs have volunteers, and therefore no employee benefit expense or liability for leave benefits. However, some have paid employees who may work for the organisation for many years, and therefore accrue liabilities for annual and long service leave benefits. AASB 119 Employee Benefits contains a complicated projected unit credit method calculation to discount future expected long service leave payments, which is costly for NFPs to implement. The AASB is therefore proposing a simplified Tier 3 method for accounting for employee benefit obligations as noted below.

Annual leave liability

This will be calculated based on the undiscounted amount expected to be paid to settle the employee’s annual leave entitlement, i.e. amount of salary when the employee is expected to take their leave. Annual leave entitlements will always be classified as a current liability because the entitlement has vested.

Long service leave liability

This will be also calculated based on the undiscounted amount expected to be paid to settle the employee’s long service leave entitlement, assuming a probability that the employee will meet the long service leave vesting conditions.

Long service leave entitlements will be classified as a current liability if the entitlement has vested, or non-current liability if they have not vested.

Income

One of the difficulties commonly experienced by Tier 1 and Tier 2 NFPs is trying to determine whether inflows are recognised:

- Under AASB 15 Revenue from Contracts with Customers, and potentially deferred and recognised as revenue as and when the entity satisfies sufficiently specific performance obligations, or

- Immediately as income under AASB 1058.

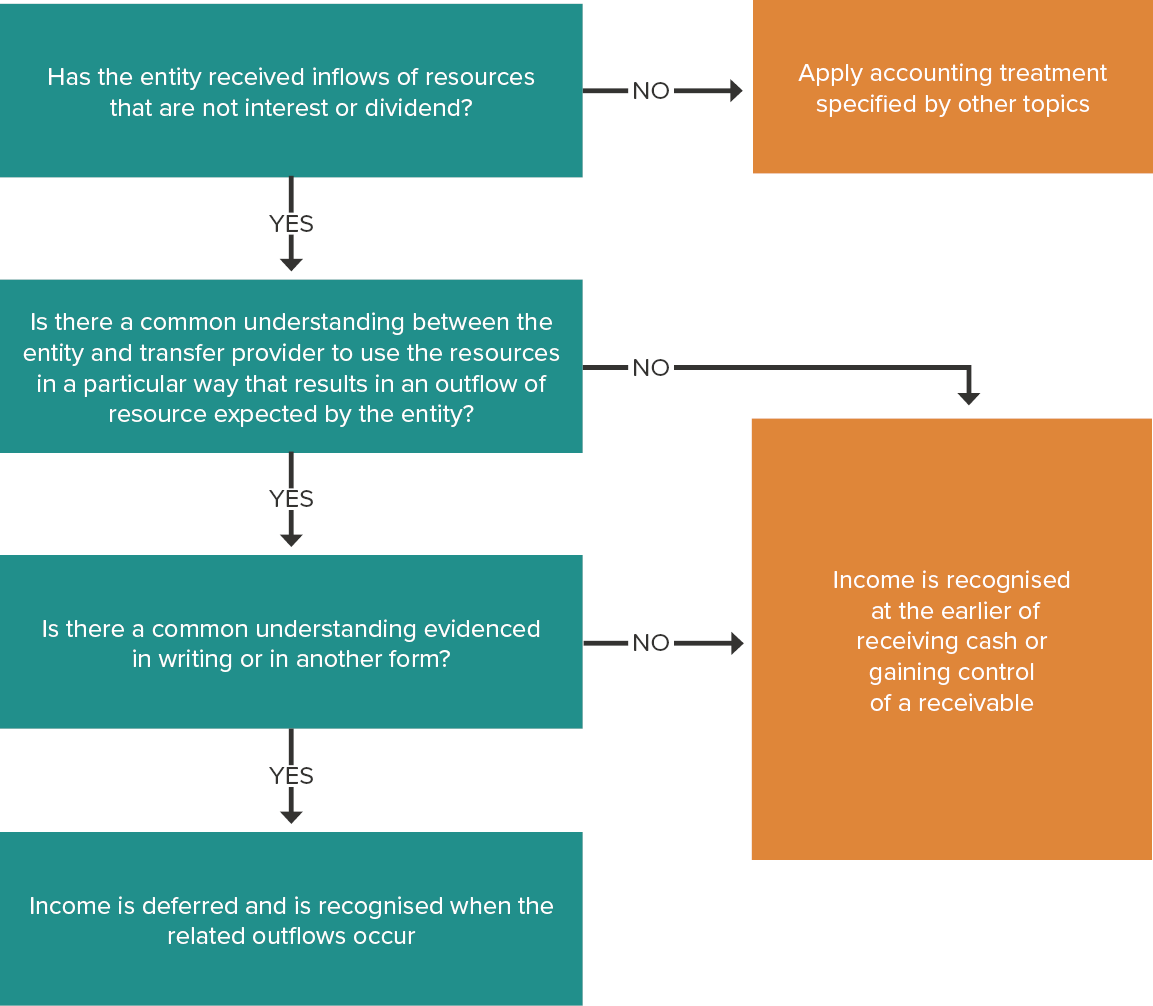

The AASB is proposing to eliminate the need for Tier 3 NFPs to consider both these standards. Instead, they can apply a simpler approach to determine if revenue/income is recognised immediately upon receipt or deferred. The following diagram summarises this new approach, and has been extracted from section 5.181 (Figure 5.3) of the Discussion Paper:

Many grant agreements previously did not contain sufficiently specific performance obligations under AASB 15. This resulted in income recognition when funds were received, and a ‘mismatch’ between the timing of funds received and fund spent.

Applying the above proposals, provided there is evidence of a common understanding between the grant provider and the NFP as to how the funds should be spent, income will be deferred and recognised when the related outflows occur.

For example, if a NFP receives $100,000 to employ two psychologists in the next reporting period, it can defer income until salaries of the psychologists have been incurred.

Similarly, if a NFP receives $50,000 on 30 June 2025 to spend generally in running its operations during the financial year ending 30 June 2026, provided this common understanding of what the funds are to be used for is evidenced, the NFP will defer recognising the $50,000 grant income until it incurs related outflows. Under AASB 15, the requirement to spend money over a time period would not meet the requirements to be a sufficiently specific performance obligation.

However, where a NFP raises funds by running raffles or having collectors standing outside shopping centres, there is unlikely to be a common understanding of what the money is to be used for, and these receipts will be recognised as income immediately.

Financial instruments

Most NFPs only have basic forms of financial instruments such as cash, receivables, security bonds, term deposits and government bonds, investments in shares and managed funds, trade payables and loans. The AASB is proposing to simplify the recognition and measurement requirements contained in AASB 9 Financial Instruments for these basic financial instruments.

The table below, extracted from the AASB’s Snapshot overview, summarises the Tier 3 measurement proposals for these basic financial instruments:

Type of financial instrument |

Proposed measurement requirements |

|

All financial instruments – initial recognition |

At fair value with immediate expensing of transaction costs |

|

Financial assets – subsequent measurement |

|

|

Financial liabilities – subsequent measurement |

At cost |

|

Interest income/expenses |

Calculate by reference to the instrument’s contractual interest rate, with any initial premium or discount amortised on a straight-line basis over the expected life of the instrument |

|

Impairment |

Consider when probable that the carrying amount will not be collectible |

|

Financial assets – derecognition |

Derecognise when either:

|

|

Financial liabilities – derecognition |

|

|

Other simplifications |

|

For more complex financial instruments, NFPs would need to consider AASB 9 for guidance.

Changes in accounting policies, errors and changes in accounting estimates

To simplify retrospective accounting where the NFP has a voluntary change in accounting policy, or needs to correct an error, the AASB is proposing that Tier 3 entities do not ‘reopen’ comparatives. This means that comparatives would not need to be restated. The cumulative effect of correcting the error, or changing an accounting policy, is made by adjusting opening balances of retained earnings and other items in the current period’s statement of financial position.

Changes in estimates will continue to be accounted for prospectively.

The AASB plans to deliberate what the accounting treatment should be for mandatory changes in accounting policies and transitional provisions, such as where there is a change to the Tier 3 measurement requirements.

Borrowing costs

Currently, Tier 1 and Tier 2 private sector NPFS must capitalise borrowing costs if they are directly attributable to the acquisition, construction, or production of a qualifying asset. The AASB’s Tier 3 proposals require that all borrowing costs be expensed as incurred.

Intangible assets

The AASB has not yet formed a preliminary view on the accounting for intangible assets by NFPs. It will determine the accounting after considering stakeholder feedback on the extent and use of intangible assets relevant to smaller NFPs.

Comments due

The AASB is seeking comment on these proposals by 31 March 2023.