Assessing climate-related risks and opportunities

Assessing climate-related risks and opportunities

Our sustainability webinar series aims to break the complex world of sustainability down into digestible pieces to help you get on top of the fundamentals and start driving change in your organisation. At our July 2024 event, Aletta Boshoff outlined essential steps and resources to guide organisations through the transition from strategic voluntary reporting to mandatory compliance.

Examining your climate-related risks and opportunities

The frequency and severity of extreme weather events, such as bushfires and floods, are on the rise, directly threatening operations and necessitating a proactive approach to risk management. These climatic changes, coupled with shifts in climatic impact drivers like heatwaves, droughts, and floods, become more pronounced with each incremental increase in global temperatures. Businesses that fail to assess and adapt to these risks may face significant operational disruptions and financial losses. Conversely, those who identify and leverage climate-related opportunities can innovate, enter new markets, and establish themselves as leaders in sustainability, securing a competitive advantage in an increasingly eco-conscious global economy.

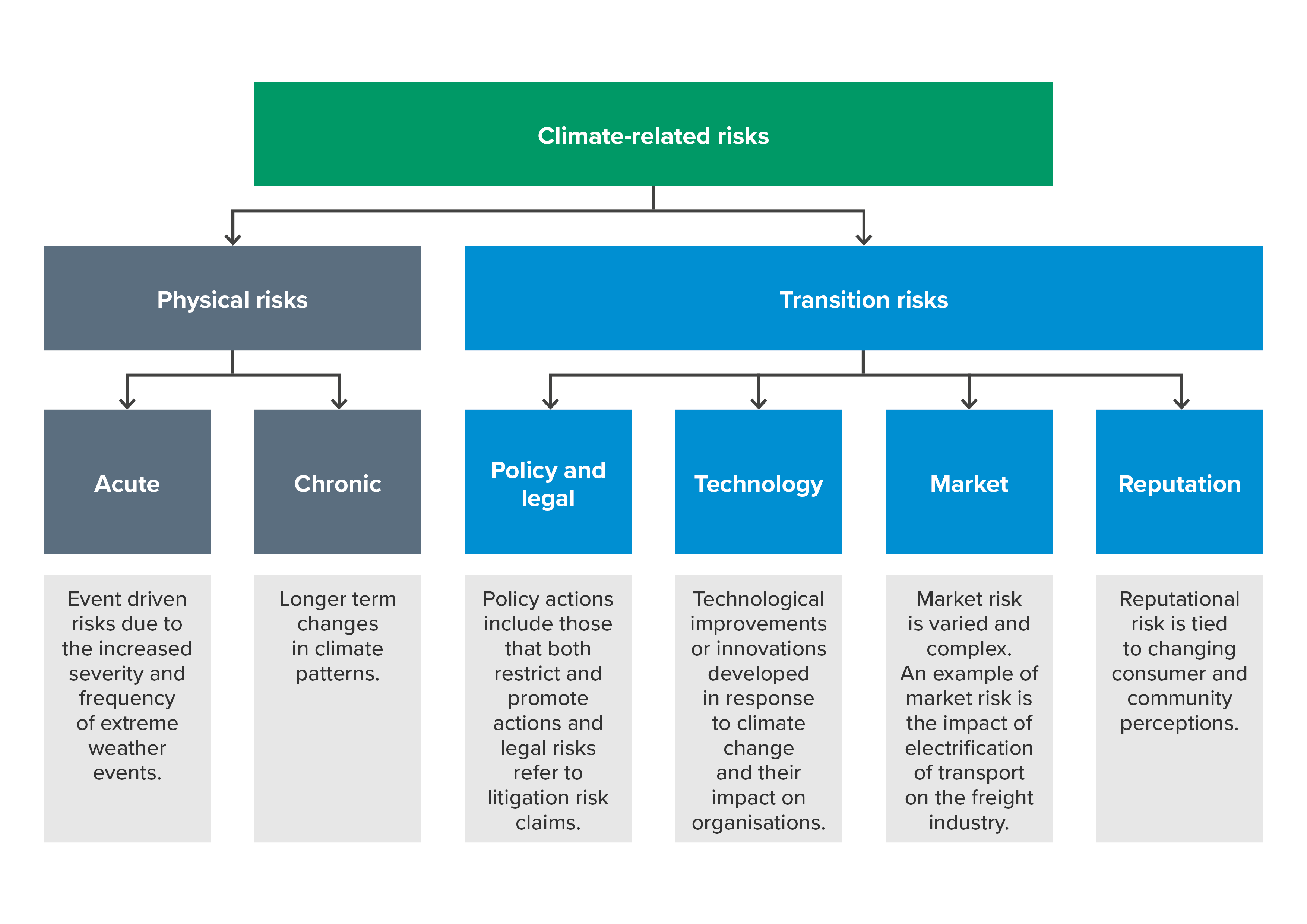

What are climate-related risks?

Climate-related risks are potential adverse outcomes that arise from the multifaceted impacts of climate change. These risks are broadly categorised into two main types: Physical risks and Transition risks. Physical risks include acute events like severe weather incidents—storms, floods, and heatwaves—that can cause immediate and significant damage to infrastructure, ecosystems, and human health. They also encompass chronic changes such as rising sea levels and long-term shifts in precipitation patterns, which can gradually undermine agricultural productivity, water supply, and the habitability of specific regions.

Transition risks are associated with the global shift towards a low-carbon economy and include policy and legal actions that may impose new regulations or liabilities on businesses. Transition risks also include technological advancements that could render existing products or services obsolete, market shifts where consumer preferences evolve towards greener options and reputational impacts where stakeholders’ perception of an organisation’s environmental responsibility can affect its brand value and customer loyalty. These risks can lead to stranded assets, increased operational costs, and changes in market demand that can significantly impact a company’s financial performance.

What are climate-related opportunities?

Climate-related opportunities offer businesses the chance to innovate and lead in the transition to a sustainable future. Resource efficiency is a prime area for exploration, where companies can reduce operating costs by adopting more efficient modes of transport, production, and distribution. Embracing a circular economy and optimising building and water use can significantly save costs.

Another opportunity is the development of low-emission products and services. As consumer preferences evolve, businesses that invest in research and development can diversify their offerings and tap into new markets, leveraging public sector incentives and adapting to changing insurance landscapes. By proactively considering your climate-related opportunities, you can potentially enhance your company’s reputation and market position.

Impacts on strategic planning, risk management and finances

What should entities do once they have identified climate-related risks and opportunities? This information must feed into the entity’s strategic planning, risk management and budgeting processes. Ultimately, the financial implications of these risks and opportunities can be considerable. By measuring the potential impact on the balance sheet revenue streams and expenditures, businesses can make informed decisions that contribute to environmental responsibility and drive economic growth. By doing so, companies can protect themselves from the adverse effects of climate change and position themselves to benefit from the growing demand for sustainable practices and products. Tables A1.1 and A1.2 in the Task Force on Climate-related Financial Disclosures (TCFD) include several examples of climate-related risks and opportunities and their potential financial impacts, and Table A1.3 shows examples of potential climate-related impacts by financial categories.

Climate-risk assessment with an industry focus

The TCFD also provides guidelines highlighting the importance of industry-specific assessments. For instance, in the energy sector, companies involved in fossil fuels and electric energy must navigate the risks and opportunities presented by the global shift towards renewable energy sources. Similarly, the transportation industry faces challenges and opportunities in adapting to low-emission technologies. The materials and buildings sectors must consider the implications of new construction standards. At the same time, the agriculture, food, and forest products groups must assess the impact of climate change on resource availability and consumer preferences. Each industry’s unique position underscores the need for tailored risk assessments to identify strategic opportunities in the context of climate change.

Climate-risk assessment methodology

BDO’s recommended approach for creating a climate-risk assessment involves a five-step methodology that comprehensively evaluates an organisation’s climate-related risks.

This is a summary of our high-level approach:

|

Step 1 |

Identify climate risks and opportunities |

Information gathering, review of information and research to identify climate risks and opportunities; transition and physical. Including review of existing enterprise risk management framework. |

|

Step 2 |

Workshop with leadership team |

Discussion particularly of identified risks and opportunities, with the leadership team and other internal subject matter experts. Reports of risks and opportunities, including the inherent risk assessment, is delivered, following the workshop. |

|

Step 3 |

Prepare draft risk register |

Incorporate insights from workshop and other feedback, into draft report and draft climate risk register, which is delivered for final review and residual risk assessment. |

|

Step 4 |

Assess control environment and residual risk |

Collaborate with management to undertake assessment of internal controls and residual risk. Draft climate risk register is updated based on findings. |

|

Step 5 |

Consider impact on risk register |

Consider how these climate risks can be embedded in the existing risk management framework. Delivery of recommended mapping of climate risks to risk register delivered. |

The outcome ensures that identified climate risks are incorporated into the company’s risk register and that climate-related risks are continuously managed alongside other business risks, facilitating a proactive and integrated approach to risk management.

How BDO can help

BDO's expertise in assessing climate-related risks and opportunities, provides businesses with the insights and tools they need to manage a changing environment. From risk assessments to strategy development, we can support you in your journey towards sustainability and resilience.

Are you ready?

To assist finance teams in preparing for mandatory climate-related financial disclosures in Australia, we’ve produced a practical roadmap aimed at helping you get ready for reporting. You can find these resources on the Chartered Accountants website or the BDO website.

Subscribe to receive our insights

SUBSCRIBE