Australia’s tax reform no. 1 Bill: What the capital gains tax (CGT), negative gearing and ‘tax-time’ changes mean in practice

The first of the Budget bills has hit, the tax reform no.1 Bill sets out a package of proposed changes that would re-shape three areas many taxpayers have long treated as ‘known knowns’, such as how capital gains are taxed, when rental losses can be used, and how individuals claim everyday work-related deductions.

What has changed

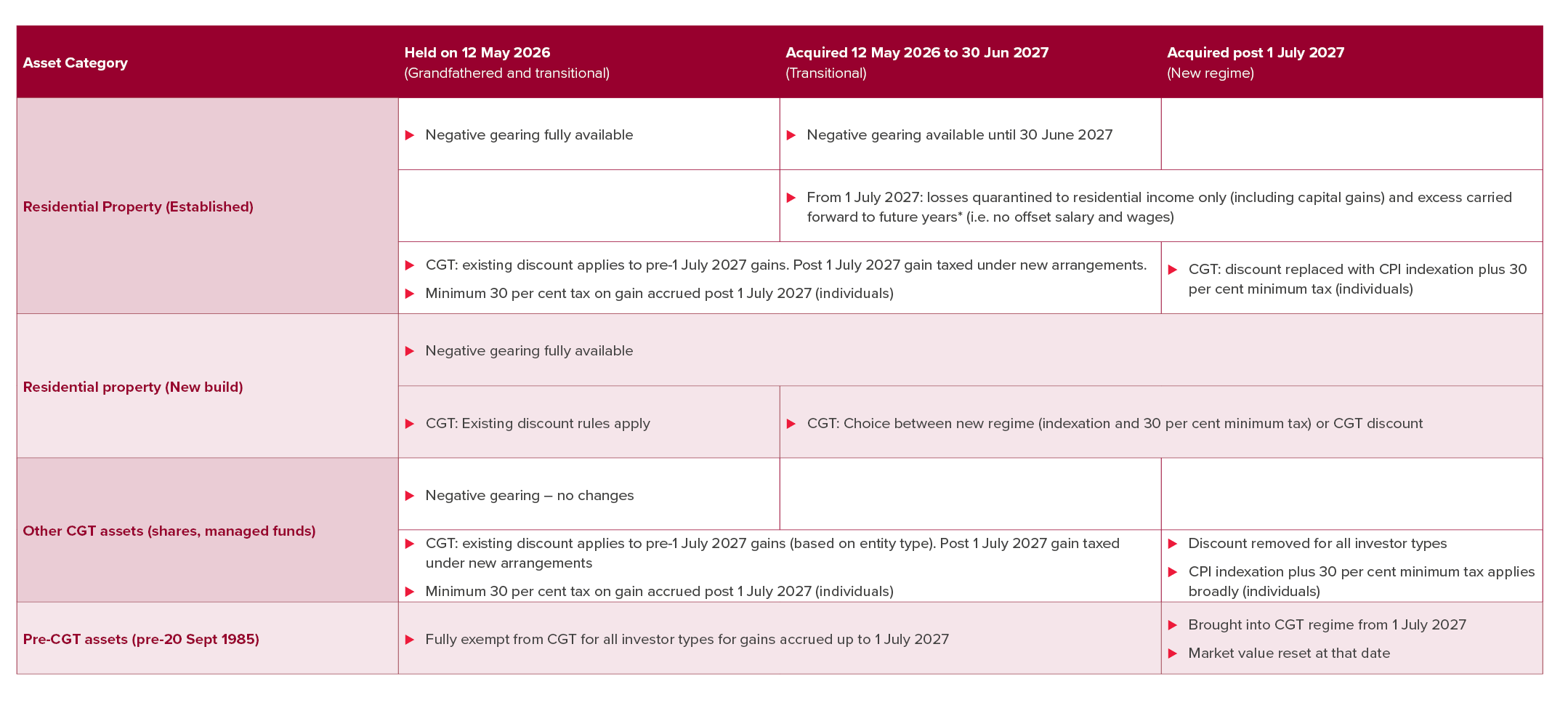

CGT: Discount out, indexation in for individuals and trusts, plus a minimum tax for some individuals

From 1 July 2027, the proposal would replace the 50 per cent CGT discount for individuals and trusts with cost base indexation, so only inflation-adjusted gains are taxed. The new regime applies to capital gains made directly or indirectly by Australian resident individuals and trusts, but not by foreign residents, temporary residents, companies or superannuation funds.

A 30 per cent minimum tax on capital gains for Australian resident individuals from 1 July 2027, aimed at limiting the benefit of timing disposals into low-rate years, such as retirement. It would operate through new Division 119 and an ‘extra income tax’ mechanism that tops up tax so relevant gains are taxed at a minimum 30 per cent rate before offsets.

The proposal also includes transitional rules. For assets held across the start date, gains are split into pre- and post-1 July 2027 components. Pre-CGT assets (acquired before 1985) would enter the CGT regime only for gains accruing after that date, while earlier gains remain disregarded.

The Bill also preserves incentives through carve-outs for new residential dwellings and affordable housing. For those assets, taxpayers may be able to choose between the existing CGT discount settings and the new regime of indexation plus the minimum tax, depending on the asset class and the choice made.

Negative gearing: Quarantining rental losses for many residential dwellings acquired from Budget night

From 1 July 2027, the Bill would treat a person’s net rental losses on a residential dwelling used or held as residential accommodation as a quarantined amount, if the relevant interest was acquired on or after 7.30pm (AEST) on 12 May 2026 (Budget night), unless an exception applies. Quarantined amounts are not lost. They can only be used to offset:

- Net assessable income from residential dwellings used or held as residential accommodation (including certain non-quarantined dwellings), and/or

- Revenue or capital gains from a residential dwelling, applied through the CGT method statement.

The Bill introduces a tailored definition of residential dwelling which specifically excludes caravans and mobile homes, hotels, motels, hostels and boarding houses, student accommodation linked to educational institutions, boats and marine vessels, and classes set by ministerial instrument.

A key feature is that the regime targets established residential dwellings, while new residential dwellings are carved out. The concept of a new residential dwelling will be set by legislative instrument and may require the dwelling to genuinely add to housing supply, such as where one demolished home is replaced by two separately titled duplexes.

Proposed Budget changes for individuals and trusts

Capital gains tax and negative gearing

Click image to open in new tab.

Why this matters in practice

The CGT reset changes long-held assumptions for individuals, trusts and family groups

For taxpayers who have historically modelled outcomes assuming a flat 50 per cent discount after 12 months, moving to indexation is a fundamental change in how gains are calculated and how holding periods are evaluated. More granular categorisation of gains (including ‘residential’ and ‘non-residential’ capital gains and ‘deferred’ categories) to support the interaction with quarantined rental losses will need to be considered.

Practically, that means taxpayers will need to think about record availability and data quality for assets held across the start date, especially where assets transition from being fully outside CGT (pre‑1985 assets) to being partly within CGT based on post‑1 July 2027 accrual. It also means trust reporting and beneficiary data flows become more important, especially for new trustee reporting requirements and penalties.

Property investors face a two-part change: Loss quarantining plus CGT mechanics

The negative gearing measure is designed so rental losses become a quarantined pool that can be applied against certain residential income streams and, crucially, against residential capital gains through the CGT method statement. This creates a different set of modelling questions for property investors and family groups, including:

- How quarantined losses are tracked and carried forward, and when they can be used against gains

- Whether an interest is caught based on acquisition timing, including some specific rules around changes to joint tenancy interests; and

- Whether a dwelling qualifies as ‘new’ under a ministerial instrument, which may require evidence that the dwelling genuinely adds to housing supply.

For those with mixed portfolios, such as older residential holdings, newer purchases, developments, and non-residential assets, the character of income and losses becomes more relevant because the Explanatory Memorandum makes it clear that quarantining is targeted to residential dwellings and does not apply to other investments like shares or commercial property.

How BDO can help

BDO can help clients pressure-test how these proposed changes apply to their fact pattern, including scenario modelling for post-2027 disposals, portfolio reviews for residential property acquisition timing and quarantined loss impacts, and guidance on record keeping requirements. Contact our corporate and international tax team for support.