When is a lease not a lease – Does the lessee have the right to direct the use of the asset?

For years ending 31 December 2019, IFRS 16 Leases requires all leases, except for some short-term and low value leases, to be capitalised on the balance sheet of lessees as a right-of-use asset and a lease liability.

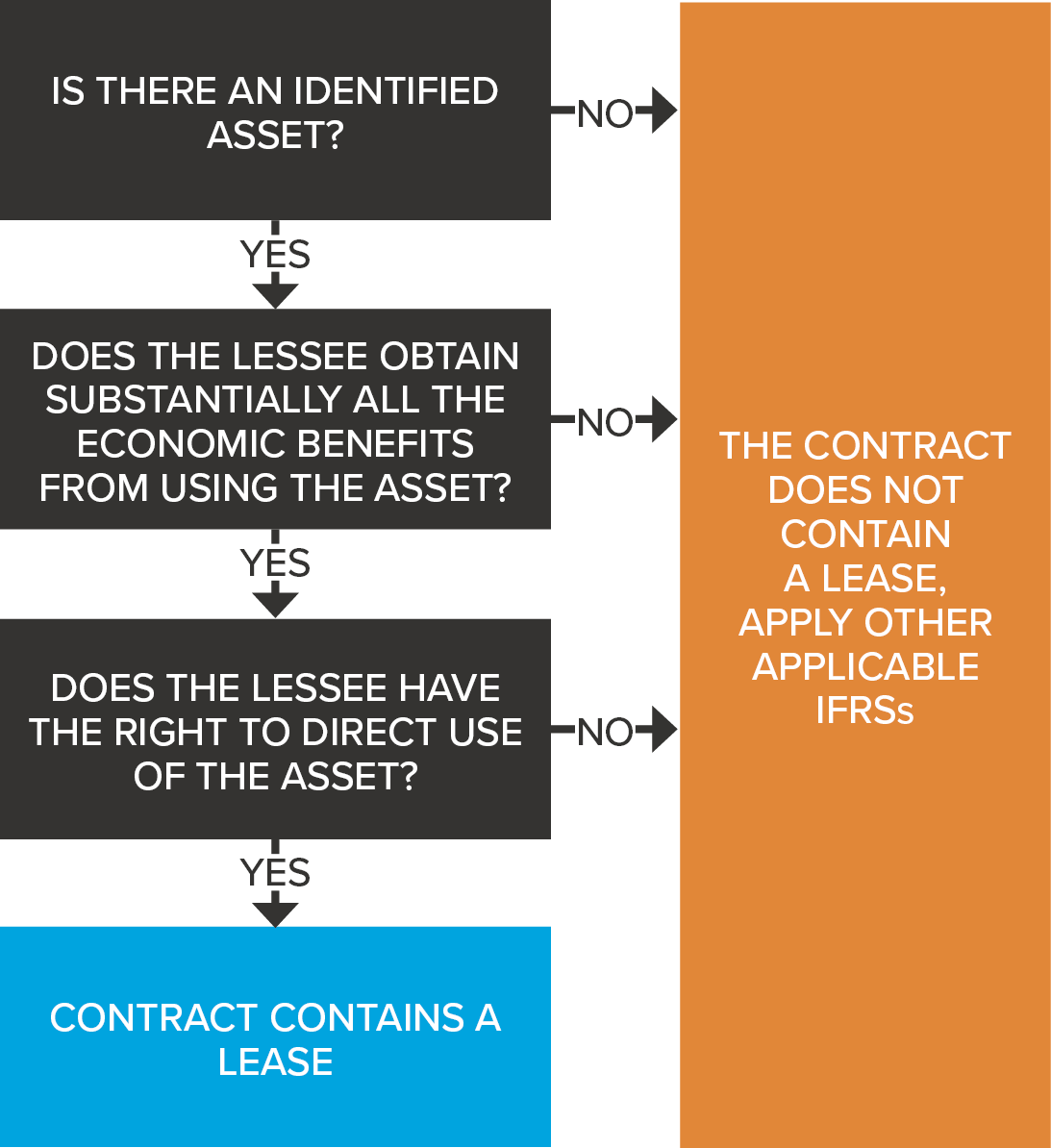

What is a ‘lease’?

Three key issues need to be considered when determining if an agreement contains a ‘lease’. These are illustrated in the diagram below.

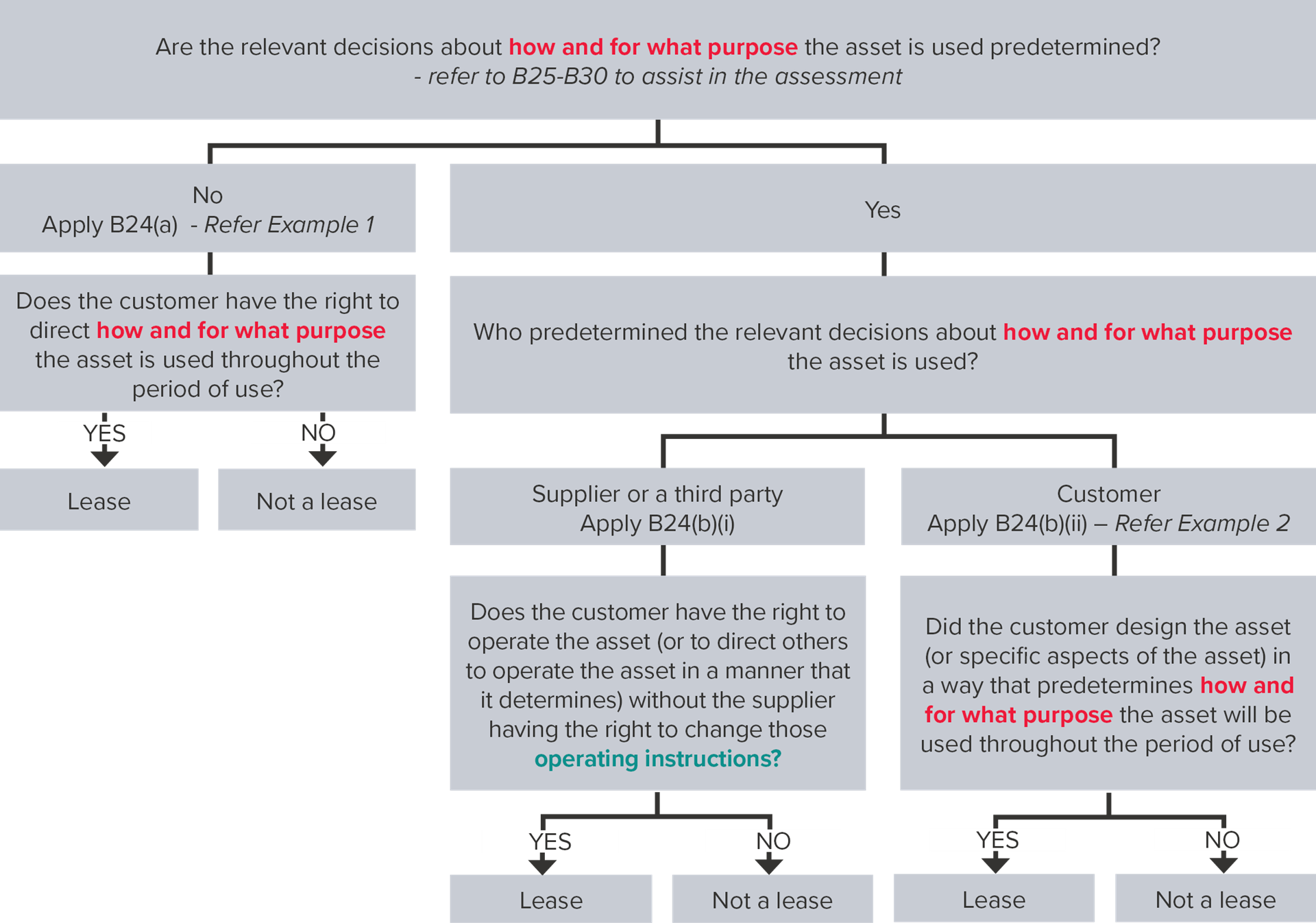

We considered the first two questions in November and December 2019 Accounting News articles. This month we take a look at the last question: ‘Does the lessee have the right to direct the use of the asset?’

In order to determine who has the right to direct the use of the identified asset, the diagram below shows how we need to determine who directs how and for what purpose the asset is used throughout the period of use. These requirements are encapsulated in IFRS 16, paragraph B24.

A customer has the right to direct the use of an identified asset throughout the period of use only if either:

- the customer has the right to direct how and for what purpose the asset is used throughout the period of use (as described in paragraphs B25–B30); or

- the relevant decisions about how and for what purpose the asset is used are predetermined and:

- the customer has the right to operate the asset (or to direct others to operate the asset in a manner that it determines) throughout the period of use, without the supplier having the right to change those operating instructions; or

- the customer designed the asset (or specific aspects of the asset) in a way that predetermines how and for what purpose the asset will be used throughout the period of use.

IFRS 16, paragraph B24

Does customer direct use (paragraph B24(a))?

A customer has the right to direct how and for what purpose an asset is used if, within the scope of its right-of-use defined in the contract, it can change how and for what purpose the asset is used throughout the period of use. Certain decision making rights are clearly more relevant than others. Those that affect the economic benefits derived from using the asset (refer December 2019 Accounting News article) are the most relevant.

Examples of decision-making rights that may grant a customer the right to change how and for what purpose an asset is used (depending on the circumstances), include rights to change:

- The type of output that is produced by the asset (e.g. what type of food certain food processing equipment produces)

- When the output is produced (e.g. the regular operating hours for equipment)

- Where the output is produced (e.g. the physical location of machinery or destinations and routes for transport equipment), and

- Whether the output is produced, and the quantity of the output (e.g. to decide whether to produce energy from a power plant and how much energy to produce).

Decision-making rights relating to operating or maintaining an asset do not grant the right to change how and for what purpose the asset is used.

Pre-determined use (paragraph B24(b))

Where, due to the nature of the asset, decisions about how and for what purpose the asset is to be used are pre-determined, it is a bit more complicated to determine whether the customer will have the right to direct the use of the asset throughout the period of use. The diagram below assists in in this decision-making process.

The examples below illustrate these principles.

Example 1 – Customer directs use

Customer A enters into a five-year contract with a supplier where Customer A will purchase up to 100% of the energy produced by a bio-mass facility.

The energy must be produced from this particular facility and the supplier does not have substantive substitution rights to provide energy from a separate facility.

Alternative arrangements can only be made in extraordinary circumstances (e.g. emergency situations rendering the facility inoperative).

Under the contract:

- Customer A tells the supplier how much energy to produce and when to produce it

- The supplier must stand ready to operate the facility to meet Customer A’s needs

- To the extent there is spare capacity, the supplier is not allowed to generate energy for sale to other customers, and

- The supplier must therefore stand ready to provide all of the power output to the customer if needed.

The supplier designed the facility when it was constructed some years before entering into the contract with Customer A, who had no involvement in the original design.

Assessment

Step one: Is there an identified asset?

It is clear that the bio-mass facility is identified in the contract.

Step two: Does the customer obtain substantially all of the economic benefits from using the asset throughout the contract period?

It is also clear that Customer A obtains substantially all of the benefits from using the asset throughout the contract period because it obtains substantially all of the economic output (it can take any amount up to 100% of the production capacity without anyone else being able to benefit from any spare capacity).

Step three: Does the customer have the right to direct the use of the asset (bio-mass facility)?

Customer A makes the relevant decisions as to how and for what purpose the bio-mass facility is used because it decides when and how much power is produced. The supplier’s staff simply follow the directions of Customer A. The fact that Customer A had no involvement in the design of the underlying asset is only relevant when decisions about how and for what purpose the asset will be used are predetermined (refer Example 3 below).

Under IFRS 16.B24(a), the contract CONTAINS A LEASE for the bio-mass facility because Customer A has the right to direct its use.

Example 2 – Predetermined use – Customer designed the asset

Customer B enters into a contract with a supplier where the customer will purchase 100% of the energy produced by a bio-mass facility.

Customer B designed the bio-mass facility before it was constructed by hiring experts in the field to assist in determining the location of the facility and the engineering of the equipment to be used.

The supplier is responsible for building the facility to the customer’s specifications, and then operating and maintaining it.

There are no decisions to be made about whether, when or how much electricity will be produced because the design of the asset has predetermined those decisions.

Assessment

Step one: Is there an identified asset?

It is clear that the bio-mass facility is identified in the contract.

Step two: Does the customer obtain substantially all of the economic benefits from using the asset throughout the contract period?

It is also clear that Customer B obtains substantially all of the benefits from using the asset throughout the contract period because it obtains substantially all of the economic output (100% of the energy produced by the bio-mass facility).

Step three: Does the customer have the right to direct the use of the asset (bio-mass facility)?

In this case, the functionality of the facility is predetermined based on its design, and those predeterminations were made by the customer. Therefore, the customer has the right to direct its use.

Under IFRS 16.B24(b)(ii), the contract CONTAINS A LEASE for the bio-mass facility because Customer B has the right to direct its use.

Concluding thoughts

Determining whether a contract is, or contains, a lease, is usually a straightforward matter. However, in practice, complex situations may arise that require the application of considerable professional judgement, including determining whether the entity has the right to direct the use of the relevant asset throughout the contract period. This can vary for similar types of assets, depending on the specific terms and conditions of individual agreements, which should not automatically be assumed to result in the same outcome. To enable such judgements to be made, finance teams will need to ensure that they are able to access all underlying contracts. If such contracts are not currently centrally stored, finance teams should commence the process of ensuring that all contracts are available for analysis well prior to the adoption of IFRS 16.