For-profit entities: Find your appropriate financial reporting framework

For-profit entities: Find your appropriate financial reporting framework

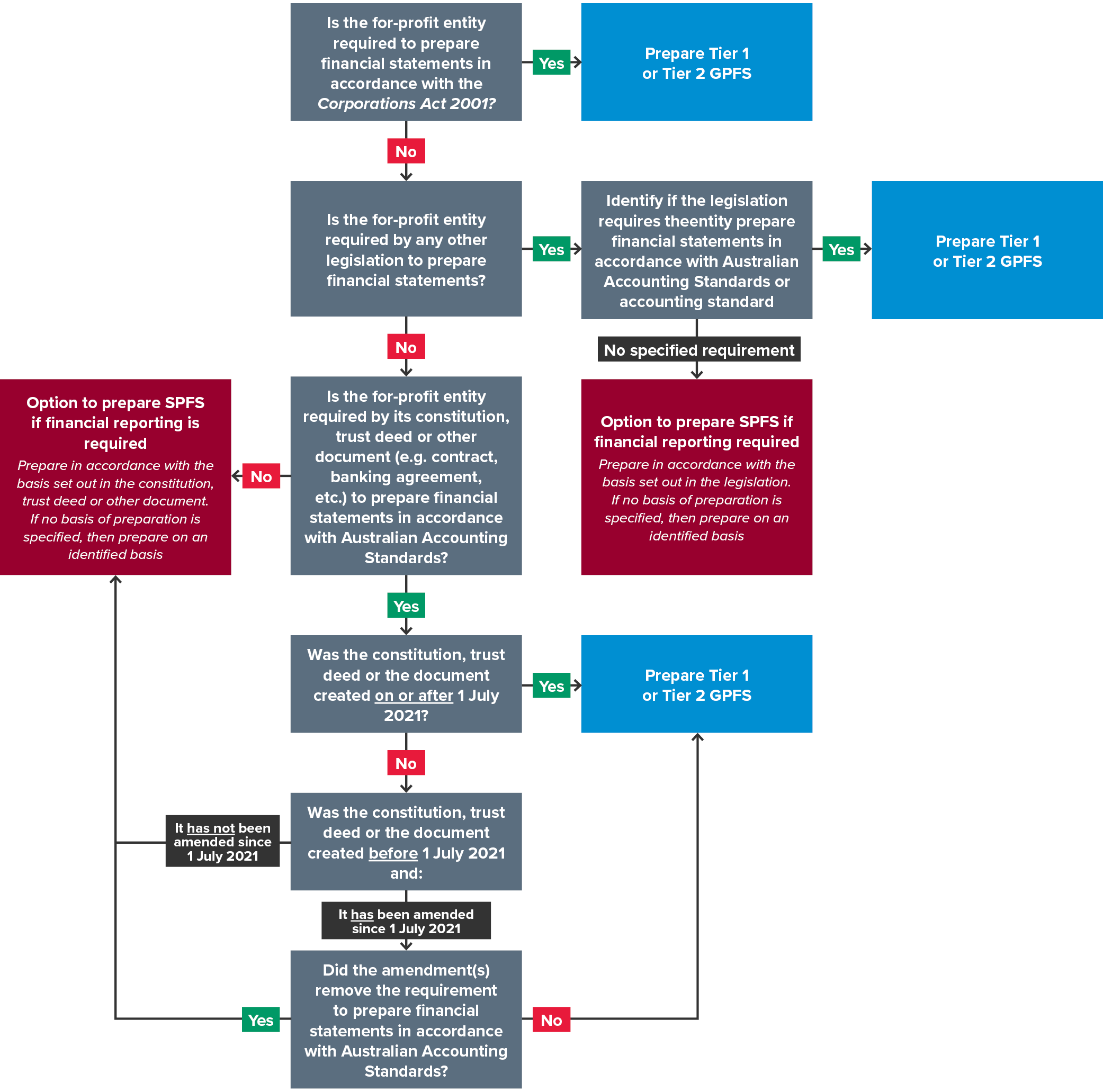

Most for-profit private sector entities required to prepare financial statements in accordance with Australian Accounting Standards must prepare general purpose financial statements (GPFS). However, there are exceptions where the driver for financial statements is not set out in legislation, but rather in other contracts and agreements.

This article will help you assess which reporting framework is appropriate for you, depending on whether your for-profit entity’s financial statements are required by:

- The Corporations Act 2001

- Other legislation

- A constitution, trust deed or another document, such as a contract or banking agreement.

These three scenarios are shown in the decision tree below.

Corporations Act

Section 292 of the Corporations Act 2001 requires the following types of for-profit entities to prepare financial statements:

- Disclosing entities

- Unlisted public companies

- Registered schemes

- Large proprietary companies

- Small foreign-controlled proprietary companies not applying ASIC Corporations (Foreign-Controlled Company Reports) Instrument 2017/204

- Small proprietary companies undertaking crowd-sourced funding.

Section 296 then requires all entities preparing financial statements under Chapter 2M to apply Australian Accounting Standards.

Both listed and unlisted disclosing entities, as well as registered managed investment schemes, must prepare Tier 1 GPFS applying all Australian Accounting Standards. The requirement to prepare Tier 1 GPFS for these entities is set out in AASB 1053 Application of Tiers of Australian Accounting Standards.

Unlisted public companies (excluding companies limited by guarantee because these are usually not-for-profit entities) and proprietary companies may prepare Tier 2 GPFS if they are not ‘Tier 1’ publicly accountable entities. Recognition and measurement for ‘Tier 2’ is per Australian Accounting Standards, but there are simplified disclosures (see AASB 1060 General Purpose Financial Statements – Simplified Disclosures for For-Profit and Not-for-Profit Tier 2 Entities).

Note that the thresholds for determining whether a proprietary company is large or small are outlined in section 45A of the Corporations Act 2001 and Regulation 1.0.02B Proprietary company thresholds (Act s 45A). These are shown in the table below. However, the 2026 Federal Budget is considering doubling the revenue and asset thresholds but at the time of writing, this has not been legislated.

|

Criteria |

Current thresholds |

Federal Budget 2026 proposed thresholds |

|

Consolidated revenue for the financial year |

$50 million or more |

$100 million |

|

Consolidated gross assets at the end of the financial year |

$25 million or more |

$50 million |

|

Group employees at the end of the financial year |

100 or more |

No change |

Other legislation

If other legislation requires financial statements in accordance with Australian Accounting Standards or ‘accounting standards’, the for-profit entity must prepare either Tier 1 (if publicly accountable under AASB 1053) or Tier 2 GPFS.

If Australian Accounting Standards or ‘accounting standards’ are not required, the for-profit entity can prepare special purpose financial statements (SPFS), applying the basis set out in the legislation, or if no basis is specified, as per the accounting policies disclosed in Note XX.

Constitution, trust deed or another document

If the constitution, trust deed, or other agreement does not specify that financial statements must be prepared by applying Australian Accounting Standards, the for-profit entity can choose to prepare either:

- GPFS (Tier 1 or Tier 2), or

- SPFS as per the accounting policies disclosed in Note XX.

Australian Accounting Standards specified

However, if the constitution, trust deed, or other agreement (document) refers to Australian Accounting Standards, the type of financial statements required is driven by the date the document was created or last updated:

- Created on or after 1 July 2021: Prepare GPFS Tier 1 or Tier 2

- Created before 1 July 2021 and not amended since: Can prepare SPFS, applying the basis set out in the document, or if no basis is specified, as per the accounting policies disclosed in Note XX

- Created before 1 July 2021 and amended since, with the requirement to apply Australian Accounting Standards remaining: Prepare GPFS Tier 1 or Tier 2

- Created before 1 July 2021 and amended since, with the requirement to apply Australian Accounting Standards removed: Can prepare SPFS, applying the basis set out in the document, or if no basis is specified, as per the accounting policies disclosed in Note XX.

Need assistance?

Getting your financial reporting framework right is vital, particularly given ASIC’s recent drive to fine entities that fail to lodge financial reports. Our IFRS & Corporate Reporting team can help you navigate these complex rules when determining the appropriate financial reporting framework for your for-profit entity.