IFRS 18: Disclosures about management-defined performance measures in notes to the financial statements

In addition to changing the way income and expenses are classified in the statement of profit or loss, IFRS 18 Presentation and Disclosure in Financial Statements, the new financial statements presentation standard that replaces IAS 1 Presentation of Financial Statements, also requires extensive disclosure about management-defined performance measures (MPMs).

Entities will need to develop systems and processes to identify measures used in public communications that meet the definition of MPMs. Entities would typically have systems in place to monitor their public communications to ensure compliance with regulatory requirements. Entities may need to modify these systems to identify MPMs. In some cases, the disclosure requirements for reconciling MPMs, including the income tax and non-controlling interest (NCI) effects of reconciling items, may involve significant additional effort. Entities need to carefully consider these requirements before using measures that meet the definition of MPMs in their public communications.

What is a management-defined performance measure (MPM)?

A management-defined performance measure (MPM) is a subtotal of income and expenses that:

- An entity uses in public communications outside financial statements

- An entity uses to communicate to users of financial statements management’s view of an aspect of the financial performance of the entity as a whole, and

- Is not listed in paragraph 118 of IFRS 18 or specifically required to be presented or disclosed by Australian Accounting Standards.

You can find an in-depth discussion on this in our previous article.

Why disclose information about MPMs?

IFRS 18 identifies two disclosure objectives for MPM disclosures, i.e. to provide information to help financial statement users understand:

- The aspect of financial performance that, in management’s view, is communicated by an MPM, and

- How the MPM compares with the measures defined by IFRS® Accounting Standards.

What to disclose?

Key points to note when disclosing information about MPMs:

- Disclosure is required for all measures that meet the definition of a MPM.

- Disclosures for all MPMs must be shown in a single note in the financial statements.

- The MPM note must include a statement that the MPMs provide management’s view of an aspect of the financial performance of the entity as a whole, and are not necessarily comparable with measures sharing similar labels or descriptions provided by other entities.

- MPMs must be labelled and described clearly so as not to mislead users of financial statements.

Figure 1 summarises the required disclosures.

|

← |

What is the MPM? |

| How is the MPM calculated? |

← |

Method of calculation |

A reconciliation between the MPM and:

|

← |

Comparison with measures defined by IFRS Accounting Standards |

For each reconciling item:

|

← |

Income tax and non-controlling interests (NCI) effects |

| A description of how IFRS 18, paragraph B141* is applied to determine the income tax effect |

← |

How the income tax effect is determined |

*IFRS 18.B141 permits an entity to determine the income tax effect using the statutory rate applicable to the transaction, or based on a reasonable pro rata allocation of the current and deferred tax, or another method that achieves a more appropriate allocation.

Source: IFRS Accounting Standards in Practice IFRS 18 Presentation and Disclosure in Financial Statements

Single note

It is important to note that IFRS 18 requires MPM disclosures in a single note. The entity cannot disclose MPM information by cross-referencing to other notes in the financial statements, neither can information about different MPMs be disclosed in separate notes. You cannot disclose information about one MPM in Note 5 and another in Note 16. They must all be disclosed in one note. This is to prevent the fragmentation of information disclosed and to improve transparency.

IFRS 18 does not prohibit an entity from disclosing other information in the note that includes the MPM disclosures. But, in this case, the entity is required to label the information so that it clearly distinguishes the disclosures related to MPMs.

Labelling of MPMs

Each MPM must be labelled and described clearly so as not to mislead users. In this regard, users must be able to understand which income and expense items have been included or excluded from the MPM subtotal.

The label should properly represent the characteristics of the MPM. For example, the label of earnings before interest and tax (EBIT) would only be used where amortisation is excluded from the MPM, otherwise earnings before interest, tax, depreciation and amortisation (EBITDA) would be considered a more appropriate description of the MPM.

When users may not understand the description, the entity should explain the meaning of the terms used to describe the MPM (for example, what items are excluded from an MPM described as ‘underlying’ EBITDA).

What if there is a difference in the way MPMs are calculated compared to accounting policies?

If the method of calculating the MPM differs from the accounting policies applied in the statement of financial performance, the following specific disclosures are required:

|

Scenario |

Disclosure requirement |

|

The method of calculation of the MPM differs from the accounting policies applied for the items in the statement of financial performance, but the method of calculation is permitted by IFRS Accounting Standards |

|

|

Method of calculation of the MPM differs from the accounting policies required or permitted by IFRS Accounting Standards |

|

What if there are changes to MPMs?

An entity may change the method of calculating an MPM, add a new MPM, cease using a previously disclosed MPM or change the approach used for determining the income tax effects of the reconciling items. In such cases, the entity must disclose:

- An explanation that enables users to understand the change, addition or cessation and its effects

- The reasons for the change, addition or cessation, and

- Restated comparative information to reflect the change, addition or cessation unless it is impracticable to do so. If impracticable, the entity must disclose that fact. The IAS 8 requirements apply when assessing whether restating the comparative information is impracticable (IFRS 18, paragraph 124(c)).

The following are not considered changes in accounting policies:

- Selecting which MPMs to use

- The method for calculating an MPM

- The method of determining the income tax effect on the reconciling items.

Therefore, the IAS 8 disclosure requirements for changes in accounting policies do not apply.

Reconciliations

IFRS 18 requires extensive disclosures regarding the reconciliation of MPMs. Firstly, the entity must determine which is the most directly comparable subtotal, and then a number of disclosures are required for each reconciling item.

Which subtotal is an MPM reconciled to?

IFRS 18 requires an entity to reconcile each MPM to either:

- The most directly comparable subtotal listed in IFRS 18, paragraph 118, or

- A total or subtotal specifically required to be presented or disclosed by IFRS Accounting Standards.

|

Subtotals listed in IFRS 18, paragraph 118 |

Totals or subtotals specifically required by IFRS Accounting Standards |

Note: A secondary reconciliation may be required. |

|

Reconciling items are aggregated or disaggregated applying the principles in IFRS 18.

What information must be disclosed for each reconciling item?

IFRS 18, paragraph B137 outlines what must be disclosed for each reconciling item:

|

Disclosure requirement |

How it applies? |

|

Applies to each reconciling item, irrespective of how many reconciling items there are |

|

Applies if there is more than one reconciling item and each reconciling item is either:

|

An example of the disclosure requirement in (b) is an entity that calculates an MPM by excluding items of expenses for two reasons:

- They were outside management’s control

- They are non-recurring.

In order to explain how each reconciling item contributes to the MPM providing useful information, the entity must disclose, for each reconciling item, how it contributed to each type of adjustment (i.e. being outside management’s control or non-recurring).

However, if there is one explanation for multiple reconciling items (for example, where there are several items excluded as non-recurring), a single narrative explanation that includes the entity’s definition of ‘non-recurring’ might suffice.

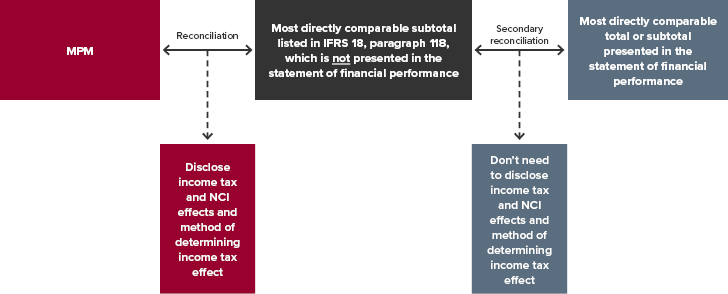

When is a secondary reconciliation required?

MPMs reconciled to subtotals required by IFRS Accounting Standards require no further reconciliation because they appear in the statement of financial performance. However, if MPMs are reconciled to the most directly comparable subtotal listed in IFRS 18, paragraph 118, sometimes these subtotals may not be presented in the statement of financial performance. In such cases, the entity must also reconcile that paragraph 118 subtotal to the most directly comparable total or subtotal presented in the statement of financial performance (secondary reconciliation). However, the income tax and non-controlling interest (NCI) impacts are not required in this secondary reconciliation. This is shown in the diagram below.

Example 1

- Entity A uses an MPM being ‘operating profit before depreciation, amortisation, impairments and non-recurring expenses’ in its public communications outside its financial statements

- Entity A elects to reconcile the MPM to ‘operating profit before depreciation, amortisation and impairments within the scope of IAS 36’, which is a subtotal listed in paragraph 118

- Entity A does not present ‘operating profit before depreciation, amortisation and impairments within the scope of IAS 36’ in its statement of financial performance.

Entity A must present two reconciliations:

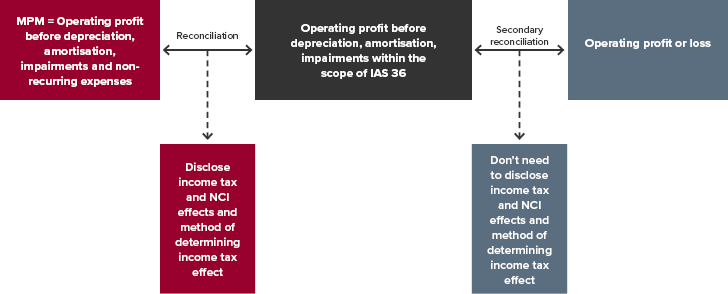

Example 2

Assume the same facts as Example 1, except that Entity A presents a subtotal for ‘operating profit before depreciation, amortisation and impairments within the scope of IAS 36’ in its statement of financial performance as an additional subtotal.

In this scenario, Entity A only reconciles its MPM of ‘operating profit before depreciation, amortisation, impairments and non-recurring expenses’ to its paragraph 118 subtotal ‘operating profit before depreciation, amortisation and impairments within the scope of IAS 36’, but it must provide the income tax and NCI effects for each reconciling item. A secondary reconciliation is not required.

Presentation of the secondary reconciliation

In our view, the ‘secondary reconciliation’ between the IFRS 18, paragraph 118 subtotal and the most directly comparable total/subtotal in the statement of financial performance may be disclosed as part of the initial reconciliation between the MPM and the paragraph 118 subtotal.

This can be achieved by presenting the combined reconciliation in a tabular format and adding additional columns or rows, as appropriate.

Income tax effect and the effect of NCI

When disclosing each reconciling item, i.e. its amount, entities must also disclose the income tax effect and the effect on NCI.

The income tax effect and the effect on NCI cannot be disclosed on a cumulative basis for all reconciling items together. This is because the income tax effect and the effect on NCI may be different for each reconciling item. For example, XYZ Group uses an MPM ‘operating profit before impairments and restructuring expenses’. In XYZ Group’s consolidated financial statements, it has recognised impairments and restructuring expenses in multiple group entities in various jurisdictions. The income tax rules applying to these adjustments may vary by jurisdiction or by nature of the adjustment within the same jurisdiction. Similarly, the effect on NCI may differ for each group entity depending on each entity’s proportion of non-controlling interests in the entity.

The International Accounting Standards Board decided to require this disclosure to enable users of financial statements to calculate an adjusted earnings per share measure.

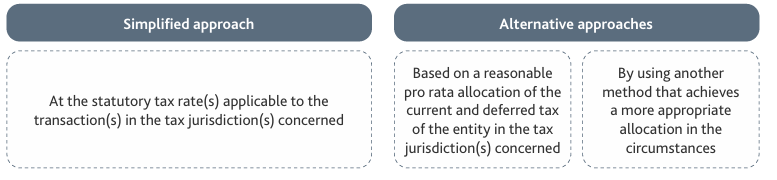

How to calculate the income tax effect of reconciling items?

For each reconciling item, an entity can use a simplified approach or one of the alternative approaches as shown below:

It must describe the approach used, and if it uses more than one, it must disclose how it determined the tax effects for each reconciling item.

The income tax effect must be disclosed, even if the MPM is a pre-tax subtotal, because the intention behind the requirement is to provide users with information about the tax effects of adjustments made to arrive at the MPM.

Example MPM disclosures

You can find an illustration of MPM disclosures in section 6.5 of our publication.

More information

Places are still available for our IFRS 18 Masterclass ‘Transitioning to management-defined performance measures’ (IFRS 18 masterclass series - BDO), to be held on Friday 31 July 9am-1pm (AEST), in which we will work through practical examples of entities transitioning their MPMs to AASB 18. You can also find more articles about IFRS 18 challenges on our IFRS 18 topic page, which includes resources such as our publication and webinars.

Need help

Our recent articles on IFRS 18 demonstrate the complexity of applying IFRS 18 in practice. Reach out to our team of experts for assistance with understanding the latest requirements in IFRS 18.