IFRS 18: Financing category differences for entities with specified main business activities

IFRS 18 Presentation and Disclosure in Financial Statements is a new financial statements presentation standard that replaces IAS 1 Presentation of Financial Statements. Under IFRS 18, all entities will have to change the way they classify expenses in the statement of profit or loss, allocating them to one of five categories: investing, financing, income taxes, discontinued operations and operating.

Why are special rules needed for classifying income and expenses in the statement of profit or loss?

Income and expenses are generally classified into one of the five categories based on the characteristic of the expense (i.e. the type of asset or liability to which the income or expense relates). Without special rules for classifying the income and expenses of entities with specified main business activities, operating profit would not include all items of income and expenses related to the entity’s main business activities, e.g. for banks and financial institutions. IFRS 18, therefore, contains exceptions so that entities with specified main business activities will classify some income and expense items in the operating category that would otherwise have been classified in the investing and/or financing categories.

What are specified main business activities?

IFRS 18 defines a specified main business activity as one where the main business activity of the entity is:

- Investing in particular types of assets, or

- Providing financing to customers.

Last month, we looked at how the IFRS 18 profit or loss investing category may differ for entities with specified main business activities. This month, we focus on changes to the financing category where the entity has a specified main business activity of providing financing to customers.

Financing category – entities without specified main business activities

Our previous article considers in some detail how income and expenses relating to liabilities are classified in profit or loss where the entity has no specified main business activities. Classification depends on the type of liability, i.e. those that:

- Involve only the raising of finance (sometimes referred to as ‘pure financing’ liabilities) – income and expenses are classified in the financing category

- Do not involve only the raising of finance – the interest portion of income and expenses is classified as financing, as well as income and expenses arising from changes in interest rates, but only if the entity identifies such income and expenses for the purpose of applying other requirements in IFRS® Accounting Standards.

Financing category – entities with specified main business activities that provide financing to customers as a main business activity

Things change somewhat for entities with a specified main business activity of providing financing to customers.

Liabilities do not involve only the raising of finance (dual purpose transactions)

Regardless of whether the entity provides financing to customers as a main business activity, interest income and expenses from liabilities that do not involve only the raising of finance (for example, ‘dual purpose’ transactions such as trade payables, leases, etc.) are classified in the financing category.

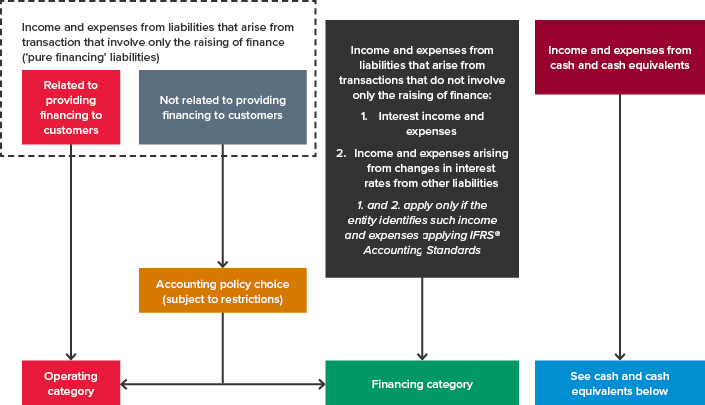

‘Pure financing’ liabilities

However, the rules may differ for ‘pure financing’ liabilities if an entity provides financing to customers as a main business activity. Income and expenses relating to ‘pure financing’ liabilities will be classified in the operating category instead of the financing category if the liability is incurred in order to provide financing to customers. This is shown in the diagram above.

‘Pure financing’ liabilities must be sub-categorised into:

- Liabilities that relate to providing financing to customers (income and expenses are always classified in the operating category), and

- Liabilities that do not relate to providing finance to customers (there is an accounting policy choice to classify income and expenses in either the operating or financing category, but there are two restrictions on this policy choice – discussed in more detail below).

Example

Bank A borrows money from Lender B in order to lend those funds to its customers.

Bank A’s goal is to earn a margin on the interest rate differential between the loans payable to Lender B and the loans receivable from its customers.

As Bank A has borrowed money from Lender B in order to lend the proceeds to its customers, that borrowing would be ‘related to providing financing to customers’. The income and expenses would, therefore, be classified in the operating category.

Restrictions on accounting policy choice where ‘pure financing’ liabilities do not relate to providing financing to customers

In practice, it may be challenging to determine whether ‘pure financing’ liabilities are related to providing financing to customers or whether they have a dual purpose. Where ‘pure financing’ liabilities are not for providing financing to customers, entities have an accounting policy choice to classify the related income and expenses in either the operating category or the financing category. However, there are two restrictions on this accounting policy choice:

- If the entity cannot distinguish between the liabilities that relate to providing financing to customers and those that don’t, it must classify income and expenses from all these liabilities in the operating category

- It must be consistent with the accounting policy the entity chose for classifying income and expenses related to cash and cash equivalents, which do not relate to providing finance to customers.

Cash and cash equivalents

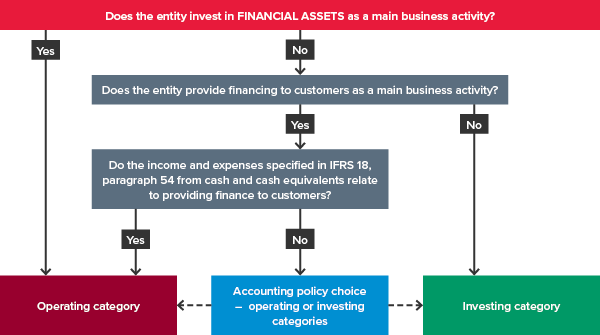

For entities with specified main business activities, the classification requirements for income and expenses relating to cash and cash equivalents (e.g. interest income) are summarised in the decision tree below:

Where an entity does not invest in financial assets as a main business activity, but does provide financing to customers as a main business activity, it must determine if the income and expenses from cash and cash equivalents relate to providing financing to customers (IFRS 18.56(b)):

- If they do, income and expenses are classified in the operating category (this is consistent with the treatment of the income and expenses related to ‘pure financing’ liabilities shown in the diagram above)

- If they don’t, there is an accounting policy choice to classify income and expenses either in the operating or the investing category, subject to two restrictions (see below).

Restrictions on accounting policy choice

The accounting policy choice noted above for classifying income and expenses related to cash and cash equivalents is subject to two restrictions:

- It must be consistent with the accounting policy choice selected for ‘pure financing’ liabilities that do not relate to providing financing to customers (see above), and

- If an entity cannot distinguish between cash and cash equivalents that relate to providing financing to customers and those that do not, it must classify income and expenses from all cash and cash equivalents in the operating category.

To summarise

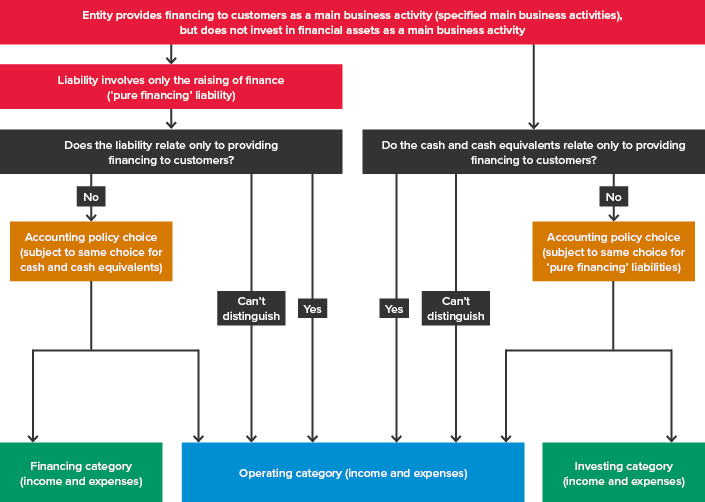

The following diagram provides a snapshot of what happens when entities whose main business is to provide financing to customers borrow money to lend to customers.

For example:

- If the borrowing is a ‘pure financing’ liability entered into only for the purpose of providing financing to customers, interest accrued on the borrowing will be classified in the operating category.

- Similarly, interest earned on cash balances held only for the purpose of lending money to customers will also be classified in the operating category.

- If the entity has general borrowings and only one bank account, and is therefore unable to distinguish what relates to customer financing and what doesn’t, all interest income and expenses will be classified in the operating category.

- If the entity enters into a separate ‘pure financing’ loan arrangement to meet its general working capital needs (i.e. not for the purpose of providing financing to customers), it can choose to either classify interest expenses in the financing or operating category, providing that it makes a similar choice for general cash and cash equivalent balances above.

More information

Previously, we explored how income and expense classification changes for the investing category where an entity has a specified main business activity of investing in assets. Stay tuned for future Corporate Reporting Insights during 2025 as we continue our deep dive into IFRS 18 to demystify some of its complexities.

Need help

Entities should start preparing now for IFRS 18 Presentation and Disclosure in Financial Statements because it is a complicated standard. Charts of accounts will need to change to appropriately tag income and expenses to the five categories, and transition dates start from 1 January 2026.

Implementing new accounting standards can be challenging. Reach out to our team for help with understanding the latest requirements in IFRS 18.