What’s new for 30 June 2017 reporting season?

The good news

The good news is that while there are several amendments applying for the first time to your June 2017 annual financial statements, most entities will only be impacted by the ‘decluttering’ changes.

Changes impacting specific entity types

Specific types of entities may be impacted by changes to standards and regulations for the first time at 30 June 2017, including:

- Superannuation entities - AASB 1056 Superannuation Entities

- Agricultural entities – changes to accounting for bearer plants

- Small businesses - the reduction to corporate tax rates from 30 June 2017

- Australian subsidiaries of ‘significant global entities’ - required to lodge general purpose financial statements with the ATO

- Public sector entities - required to disclose more information about related party transactions but less information about level 3 fair values.

Other changes

Otherwise, changes included in new standard AASB 14 Regulatory Deferral Accounts and the other amending standards are transaction/balance specific, and therefore unlikely to impact your accounts except in specific circumstances.

However, you should note that the Australian Securities and Investments Commission (ASIC), as part of its financial reporting surveillance programme, continues to focus on particular risk areas in both listed and unlisted entities, and ‘naming and shaming’ entities required to restate financial statements as a result of these surveillance enquiries. Our article, 'ASIC calls on preparers to focus on the quality of financial information', includes more details on ASIC's focus areas for its surveillance of 30 June 2017 financial statements.

Half-years

For listed entities reporting half-year results at 30 June 2017, there are no new standards that will impact your interim financial report for the first time, but you may be impacted by the recent IFRS Interpretations Committee agenda decision on deferred tax liabilities for indefinite-lived intangibles.

The calm before the storm

This is the calm before the storm, with AASB 9 Financial Instruments and AASB 15 Revenue from Contracts with Customers (including the AASB 2016-3 amendments to AASB 15) effective for the first time for your 30 June 2019 annual periods, and AASB 16 Leases effective for the first time for 30 June 2020 annual periods. For insurance companies, IFRS 17 Insurance Contracts will impact you for the first time for 30 June 2022 financial years.

ASIC continues, as part of its financial reporting surveillance programme, to focus on disclosures in the financial statements about the impacts of these standards and amendments that have been issued, but not yet effective. In its December 2016 Media Release 16-442, ASIC reminds companies that it expects them to be able to quantify the impacts of AASB 9 and 15 in their June 2017 annual financial statements where adjustments for application of the new standards will be made on a fully retrospective basis.

What are the changes?

You need to consider the following accounting standards, amending standards and other legislative changes/decisions when preparing your 30 June 2017 annual financial statements:

- Decluttering (AASB 2015-2 Amendments to Australian Accounting Standards — Disclosure Initiative: Amendments to AASB 101)

- Bearer plants (AASB 2014-6 Amendments to Australian Accounting Standards — Agriculture: Bearer Plants)

- Accounting for the acquisition of joint operations (AASB 2014-3 Amendments to Australian Accounting Standards — Accounting for Acquisitions in Joint Operations)

- Clarification of acceptable methods of depreciation or amortisation (AASB 2014-4 Amendments to Australian Accounting Standards — Clarification of Acceptable Methods of Depreciation and Amortisation)

- Equity method in separate financial statements (AASB 2014-9 Amendments to Australian Accounting Standards — Equity Method in Separate Financial Statements)

- Investment entities: applying the consolidation exemption (AASB 2015-5 Amendments to Australian Accounting Standards — Investment Entities: Applying the Consolidation Exemption)

- Annual improvements (AASB 2015-1 Amendments to Australian Accounting Standards — Annual Improvements to Australian Accounting Standards 2012-2014 Cycle)

- AASB 14 Regulatory Deferral Accounts

- Calculation of deferred tax on an indefinite life intangible asset (IFRS Interpretations Committee agenda decision)

- New ASIC Legislative Instrument for wholly-owned companies

- Significant global entities required to lodge general purpose financial statements

- Changes to company tax rates for small businesses.

While many of the above accounting standards and amending standards applied for the first time to entities with years ending 31 December 2016, this is the first time these standards will apply to entities with an annual reporting period ending 30 June 2017.

Public sector entities

Public sector entities will also need to consider the following amending standards which may impact their 30 June 2017 financial statements for the first time:

- Related party disclosures (AASB 2015-6 Amendments to Australian Accounting Standards – Extending Related Party Disclosures to Not-for-profit Public Sector Entities)

- Fair value disclosures (AASB 2015-7 Amendments to Australian Accounting Standards — Fair Value Disclosures of Not-for-Profit Public Sector Entities)

Superannuation entities

Superannuation entities will need to consider new standard, AASB 1056 Superannuation Entities for the first time at 30 June 2017.

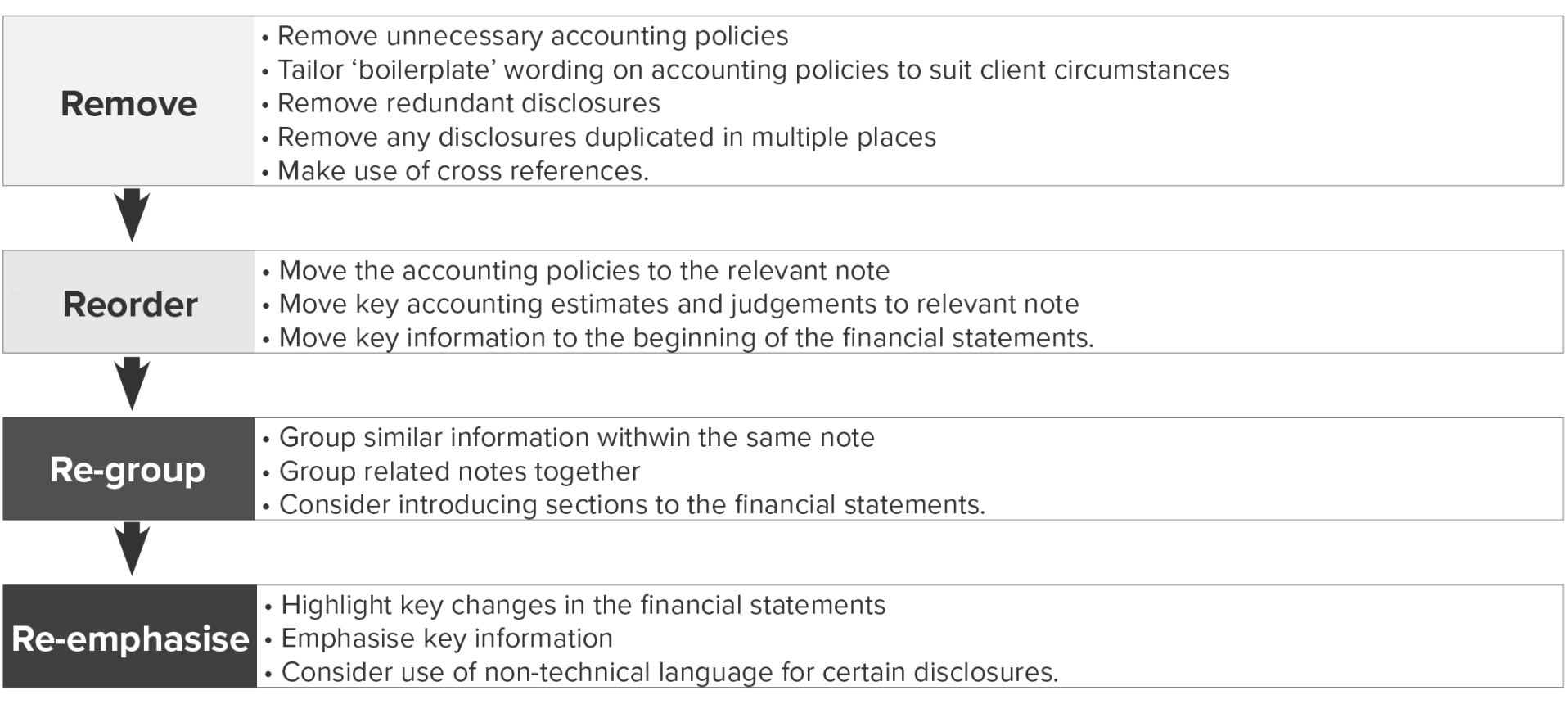

Decluttering

As part of the International Accounting Standards Board’s initiative to improve disclosures in financial statements (Disclosure Initiative), amendments have been made to AASB 101 Presentation of Financial Statements to facilitate ‘decluttering’ of financial statements by allowing preparers to apply judgement when deciding which mandatory disclosures are relevant to users, and which are not.

Besides full general purpose financial statements, this ‘decluttering process’ should also be applied to financial statements prepared using the reduced disclosures, and special purpose financial statements.

For a reminder on how to implement these changes and our ‘4R’ process, please refer to our November 2016 Accounting News article, Time is running out to ‘declutter’ your financial statements — 31 December 2016 financial statements must be ‘decluttered’.

Bearer plants (AASB 2014-6)

A bearer plant is a living plant that is used in the production process of agricultural produce, is expected to bear produce for more than one period, and has a remote likelihood of being sold (AASB 141, paragraph 5). Entities growing produce for sale on plants such as grape vines, fruit trees, oil palms or tea bushes will be affected by these amendments.

AASB 2014-6 significantly changes the way entities account for bearer plants. The entire plant is no longer accounted for at fair value with gains and losses reported in profit or loss, but separated into the bearer plant, and the produce on the bearer plant.

The produce on the bearer plant remains within the scope of AASB 141, and continues to be accounted for at fair value. The bearer plant itself now falls within the scope of AASB 116 Property, Plant and Equipment, is initially measured at cost, and then subsequently accounted for under either the cost or revaluation model.

Action points

You will need to account for these changes retrospectively in accordance with AASB 108 Accounting Policies, Changes in Accounting Estimates and Errors, however the amendment includes certain transitional relief, such as being able to revert to the cost model, or using fair values at transition date as deemed cost.

Accounting for the acquisition of joint operations (AASB 2014-3)

As a result of diversity in practice, AASB 11 Joint Arrangements was amended by AASB 2014-3 to include guidance on the accounting for an acquisition of a joint operation that constitutes a business.

If an entity acquires an interest in a joint operation that is a business, it will follow the acquisition approach in AASB 3 Business Combinations, provided the principles do not conflict with any guidance in AASB 11. This means that the entity will recognise:

- Assets and liabilities as its share of the fair values, including its share of the related deferred tax assets and liabilities

- Acquisition-related costs as expenses in profit or loss, and

- Goodwill as the excess of the consideration over the fair value of the identifiable net assets acquired.

Action points

Entities only need to apply this amendment prospectively. If you acquire a joint operation that constitutes a business from 1 July 2016, you will need to account for this transaction using the acquisition method prescribed in AASB 11.

For more information, refer to our May 2014 Accounting News article, ‘Changes to IFRS 11 Joint Operations — Accounting for acquisition of interests in joint operations’.

Clarification of acceptable methods of depreciation or amortisation (AASB 2014-4)

The amendment to AASB 116 Property, Plant and Equipment clarifies that a revenue-based depreciation model is never permitted for items of property, plant and equipment because revenue generated by the asset does not adequately capture the consumption of the economic benefits embodied within the asset. For example, it may be appropriate to depreciate a production machine based on the number of widgets it produces, but it would not be considered appropriate to depreciate the production machine based on revenue from the widgets because the entity can sell the widgets for a range of different prices.

A similar amendment made to AASB 138 Intangible Assets clarifies that a revenue-based amortisation model is only permitted in very limited circumstances, including:

- Where an intangible asset is a measure of revenue — for example a toll road operator may have the right to operate a toll road up until the point that a certain amount of revenue has been generated, or

- Where revenue and consumption of the economic benefits are highly correlated — for example where an entity holds a concession to explore and extract gold from a gold mine that expires when total cumulative revenue reaches a certain threshold.

Action points

If your current accounting policy is to depreciate property, plant and equipment or amortise intangible assets based on revenue, you need to assess whether to change this policy from 1 July 2016 to another acceptable method (e.g. straight line, or units of production) that is permitted under AASB 116 or AASB 138.

Changes to depreciation methods will be accounted for prospectively as changes in an accounting estimate.

Equity method in separate financial statements (AASB 2014-9)

AASB 2014-9 amends AASB 127 Separate Financial Statements to allow entities to measure their investments in subsidiaries, associates or joint ventures using the equity method (as described in AASB 128 Investments in Associates and Joint Ventures) in their separate financial statements.

AASB 127 previously only allowed entities to measure investments in subsidiaries, associates or joint ventures at either cost or fair value, in accordance with AASB 139 Financial Instruments: Recognition and Measurement (or AASB 9 Financial Instruments, if early adopted).

These amendments apply retrospectively.

Action points

When first adopting these amendments, you may choose to continue with your accounting policy to hold your investments at cost or fair value, or you may choose to adopt the new equity accounting option, which will result in an increase in investments, retained earnings and other reserves on transition date.

Investment entities: applying the consolidation exemption (AASB 2015-5)

These changes clarify a number of different aspects of accounting for investment entities, as follows:

Intermediate parent entity consolidation exemption

Previously, intermediate entities were relieved from preparing consolidated financial statements where the ultimate parent prepared consolidated financial statements that complied with IFRS, which were available for public use.

The first amendment in AASB 2015-5 extends these exemptions where the ultimate parent entity is an investment entity, and therefore does not prepare consolidated financial statements, instead measuring investments in subsidiaries at fair value.

Subsidiaries that provide investment-related services

The second amendment clarifies that an investment entity must consolidate subsidiaries, rather than measure them at fair value through profit or loss, if they provide investment-related services. Such a subsidiary will only be consolidated if:

- It is not itself an investment entity, and

- Its main purpose is to provide investment-related services.

Equity accounting investment entities

If you are equity accounting an associate or joint venture that is an investment entity, you may choose to retain the fair value measurement applied by the associate or joint venture to its investments in subsidiaries. This means that no adjustments need to be made to unwind fair value measurement.

Action points

Consider if you are able to take advantage of the relief provided by these amendments.

Annual improvements (AASB 2015-1)

The International Accounting Standards Board’s 2012-2014 annual improvements in AASB 2015-1 are not expected to have a major impact on current practice. These are summarised in the table below:

| Standard | Impact of Amendments |

| AASB 5 Non-current Assets Held for Sale and Discontinued Operations | If you reclassify an asset/disposal group from being held for sale to being held for distribution to owners, or from being held for distribution to owners to being held for sale, this is considered to be the continuation of the original plan of disposal. If an asset ceases to be held for distribution to owners, the usual AASB 5 requirements for assets that cease to be classified as held for sale apply. |

| AASB 7 Financial Instruments: Disclosures | When disclosing details of transferred financial assets under AASB 7.42D to 42G, there will be ‘continuing involvement’ for a service contract where the servicing fee is dependent on the amount or timing of cash flows collected from the transferred asset. Offsetting disclosures required by AASB 7.13A to 13F are not explicitly required in interim periods but may be required if significant under AASB 134 Interim Financial Reporting. |

| AASB 119 Employee Benefits | High quality corporate bonds or national government bonds used to determine the discount rate must be denominated in the same currency as the benefits that will be paid to the employee. |

| AASB 134 Interim Financial Reporting | If the disclosures required by AASB 134.16A (mandatory interim disclosures) are included elsewhere in the interim financial statements (e.g. management commentary), a cross-reference is required to this information in the interim financial report. |

AASB 14 Regulatory Deferral Accounts

AASB 14 Regulatory Deferral Accountsis unlikely to impact any Australian entities because it only applies to first time IFRS adopters that are conducting rate-regulated activities and recognise associated assets and liabilities in accordance with their current national GAAP.

This is an interim standard, pending the outcome of the IASBs comprehensive project on rate-regulated activities.

Calculation of deferred tax on an indefinite life intangible asset

At its November 2016 meeting, the IFRS Interpretations Committee clarified, for the purpose of calculating deferred tax, how an entity should determine the expected manner of recovery of an intangible asset that has an indefinite useful life. Diversity exists in practice on how entities account for this Deferred Tax Liability (DTL).

As part of the Committee’s analysis of this issue, it noted that the existing guidance in IFRS is clear that the deferred tax on an intangible asset with an indefinite life should be calculated based on how the entity expects to recover the asset, i.e. either through use or through sale.

In our view, if the adjustment to recognise a DTL on an indefinite-lived intangible asset (not previously recognised) is made in the first annual reporting period ending after November 2016, you can change your accounting policy and retrospectively restate your financial statements in accordance with AASB 108 Accounting Policies, Changes in Accounting Estimates and Errors. However, if you do not make the adjustment in the first annual reporting period after November 2016, you will need to recognise the adjustment as an error in accordance with AASB 108.

Simple example

During the current financial year, Company A purchased Company B’s business, including all of its operations, stores and brand names which it intends to use. This transaction meets the definition of a business combination under AASB 3 Business Combinations.

As part of the purchase price allocation, brand names are assigned a fair value of $500 million.

The carrying amount of the brand name in the books of Company B (acquiree) is NIL.

The tax base of the brand name is NIL if used, and $500 million if sold.

The brand names are considered to have an indefinite life under AASB 138 Intangible Assets.

Company A has a 30 June 2017 year end.

Company A should recognise a DTL for the brand name because there is no exemption in AASB 112 Income Taxes for recognising DTLs that arise from assessable temporary differences on a business combination.

If Company A had not recognised the DTL for the brand name that will be recovered through use, then the journal entry to record the deferred tax liability would be (assuming goodwill is not impaired):

| Dr | Goodwill | $150 million | |

| Cr | Deferred tax liability | $150 million | |

| 30% of ($500 million less NIL tax base) |

However, if Company A intended to hold the business short term, and then sell the business and brand name, it should instead recognise the DTL using the tax base on sale of the asset.

Action points

If you have indefinite-lived intangible assets on your balance sheet from a previous business combination, consider if you have correctly recognised a DTL as part of the business combination accounting. If not, you will need to recognise a DTL based on your expected manner of recovery (i.e. through use or through sale), and retrospectively recognise this liability in your 30 June 2017 financial statements.

New ASIC Legislative Instrument for wholly owned companies

ASIC Legislative instrument 2016/785 provides wholly-owned entities party to a deed of cross guarantee with relief from the requirement to prepare, have audited and lodge financial statements with ASIC, provided certain conditions are met.

This instrument replaces Class Order 98/1418, and was re-made substantially unaltered because it was operating effectively.

Action points

Although the disclosure requirements in the financial statements remain largely unchanged, you will need to update the reference in your financial statements and directors’ declaration from CO 98/1418 to Legislative Instrument 2016/785.

Significant global entities required to lodge general purpose financial statements

The Tax Laws Amendments (Combating Multinational Tax Avoidance) Bill 2015 is effective for the first time to 30 June 2017 year end and aims to combat multinational tax avoidance in Australia by seeking to improve the transparency about whether Australian subsidiaries of significant global entities are paying sufficient tax in Australia.

Australian subsidiaries of ‘significant global entities’ (entities with A$1 billion or more of global income) will be required to lodge general purpose financial statements with the Commissioner of Taxation in Australia (ATO) if they currently are not required to lodge general purpose financial statements with ASIC under current Australian reporting requirements.

When the ATO receives these general purpose financial statements, it is required to pass them onto ASIC to put on its database so that they will be available on public record.

As a result of these changes, large ‘grandfathered’ proprietary companies that are part of a A$1 billion group, will effectively lose their non-lodgement status if they only trade in Australia.

Action points

If your entity is part of a group with A$1 billion or more in global revenue and currently does not lodge general purpose financial statements with ASIC, for the year-ending 30 June 2017 it will need to prepare general purpose financial statements (either Tier 1 or Tier 2) and lodge these financial statements with the Commissioner of Taxation in Australia.

Small foreign controlled proprietary companies that are subsidiaries of ‘significant global entities’ currently applying Legislative Instrument 2017/204 (old Class Order 98/98), and therefore not preparing any financial statements, will need to upgrade to at least Tier 2 (RDR) general purpose financial statements.

Changes to company tax rates for small businesses

On 9 May 2017, the Treasury Laws Amendment (Enterprise Tax Plan) Bill 2016 was passed through the House of Representatives for a second time after various changes requested by the Senate in March 2017. This date is considered to be ‘substantive enactment’ for the purpose of determining current and deferred taxes under AASB 112 Income Taxes.

This Bill reduces the company tax rate to 27.5% for smaller companies carrying on a business with an aggregate turnover* not exceeding:

- $10 million for the income tax year ending 30 June 2017

- $25 million for the income tax year ending 30 June 2018, and

- $50 million for the income tax year ending 30 June 2019.

*Aggregate turnover includes turnover of connected entities (including parent companies, subsidiary companies and sister subsidiary companies)

AASB 112 requires a reduction in the corporate tax rate to impact the measurement of current tax in the year in which the new rate becomes effective. However, deferred tax assets and liabilities are measured at tax rates expected to apply in the period when the asset is realised, or the liability is settled.

Action points

If it is likely that your entity will meet the revenue thresholds for the lower 27.5% tax rate in future years, you will need to recalculate deferred tax on temporary differences using the new rate when assessable or deductible temporary differences are expected to be settled or realised.

If you expect your tax rate to reduce over the next three years, you will need to:

- Calculate current tax at 27.5% in the year that it first applies, and

- Recalculate your deferred tax balances now based on the timing of when you expect to realise the asset or settle the liability.

For further information, refer to our May 2017 Accounting News Article ‘Reduction of tax rates for small business is now law (substantive enactment)’.

Related party disclosures for not-for-profit public sector entities (AASB 2015-6)

Amending standard AASB 2015-6 Amendments to Australian Accounting Standards – Extending Related Party Disclosures to Not-for-profit Public Sector Entities removes the scope exemption in AASB 124 Related Party Disclosures for not-for-profit public sector entities. This means that not-for-profit public sector entities are now required to include all related party disclosures in their financial statements. The amendments include an appendix of Australian guidance to help apply the changes in practice.

Fair value disclosures for not-for-profit public sector entities (AASB 2015-7)

AASB 2015-7 Amendments to Australian Accounting Standards — Fair Value Disclosures of Not-for-Profit Public Sector Entities reduces the disclosure requirements in AASB 13 Fair Value for not-for-profit public sector entities. Disclosures about level 3 fair value assumptions on items of property, plant and equipment for which future economic benefits are not primarily dependent on the asset’s ability to generate cash flows (e.g. roads and infrastructure assets such as for the supply of water) are no longer required.

AASB 1056 Superannuation Entities

AASB 1056 Superannuation Entities replaces AAS 25 Financial Reporting by Superannuation Plans and applies only to large superannuation entities regulated by APRA, as well as public sector superannuation entities. While it does not need to be applied to small APRA funds or self-managed super funds, these smaller funds could choose to apply this standard.

AASB 1056 will substantially change reporting for superannuation entities because it:

- Prescribes a new format (and content) for the financial statements

- Requires all assets and liabilities be measured at fair value in accordance with the requirements in AASB 13 Fair Value, instead of at net market value

- Introduces new requirements for the recognition and measurement of member liabilities

- Requires an employer-sponsored receivable to be recognised (i.e. the difference between defined benefit member liability short-fall and the fair value of assets), and

- Introduces additional disclosure requirements

Please refer to our May 2017 Accounting News article ‘Guidance for superannuation entities applying the new Accounting Standard AASB 1056 Superannuation Entities for the first time’ for further information.