This article was originally published 23 April 2020.

ASIC has recently noted concerns with mineral asset valuation methodologies that appear to be selectively employed by Technical Specialists to support a subjective assessment. In its Report1 released on 20 April 2020, ASIC cited a case study whereby a Technical Specialist had applied subjective discounts and premiums to technical valuations without providing a ‘reasonable basis’ for the adjustments. The use of the multiples of exploration expenditure and geoscientific approaches were referenced. The transaction was ultimately withdrawn.

ASIC expressed its view that:

“In circumstances where an entirely subjective valuation is completed, practitioners must ensure they clearly:

- disclose that the valuation completed is entirely subjective and not provided for in the VALMIN Code (2015). This may include following the relevant processes for transparency and non-compliance : see cl 12.1 of the VALMIN Code

- explain why none of the methodologies set out in the VALMIN Code can be applied

- describe the information relied on in arriving at the subjective valuation”

What is clear and has always been the case is that when employing a methodology an expert must adequately disclose the assumptions and inputs relied upon and demonstrate the basis, which must be ‘reasonable’, for the assumptions and conclusions drawn.

The methodologies used – rule of thumb

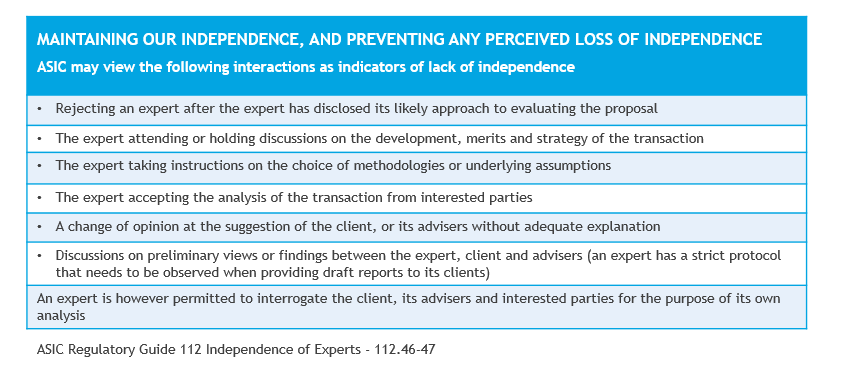

A question often asked is what methodologies we’ll be using, in particular, will we be using Discounted Cash Flow. Although we need to observe some clear regulatory requirements on these discussions so that we can protect your transaction from a compromise of our independence, we can provide a rule of thumb.

The valuation approaches chosen will depend on stage of development of your assets and will determine who needs to value what.

Who values what

BDO (an Independent Expert) has the specialist knowledge and skills to value the companies involved in the transaction. To value a company and its securities, the company’s assets generally also need to be valued. Sometimes BDO will engage an Independent Technical Specialist to value a company’s assets. BDO will then rely on their valuation to value the entities that are part of the transaction to arrive at an opinion on whether the transaction is fair and reasonable to non-associated shareholders.

For mining and resources companies the valuation methodologies depend on the stage of development of the mineral asset. They will be valued by a mining valuation Specialist who will be guided by the VALMIN Code 20152 in choosing the most appropriate valuation approach (market, income, or cost).

For a Technical Specialist's explanation on valuing mineral assets, follow this link: https://www.csaglobal.com/valuation-for-mineral-projects-part-1/

Some clients ask if they can choose the Independent Technical Specialist, because they know the company’s assets well, have done work for the company before, or can engage them for a low fee.

It is the Independent Expert’s responsibility to choose and instruct a Technical Specialist so that we can ensure they are independent, remain independent during the course of the work, and have the qualifications and experience relevant to the asset to be able to arrive upon a reliable opinion.

A mining valuation Specialist must fully understand and have the experience with the disclosure obligations under VALMIN 2015, and JORC 2012. If not, what seems low cost up front may end up costing in time and possibly reputation if the report is unlikely to meet the standard of VALMIN and JORC disclosure that the regulators require.

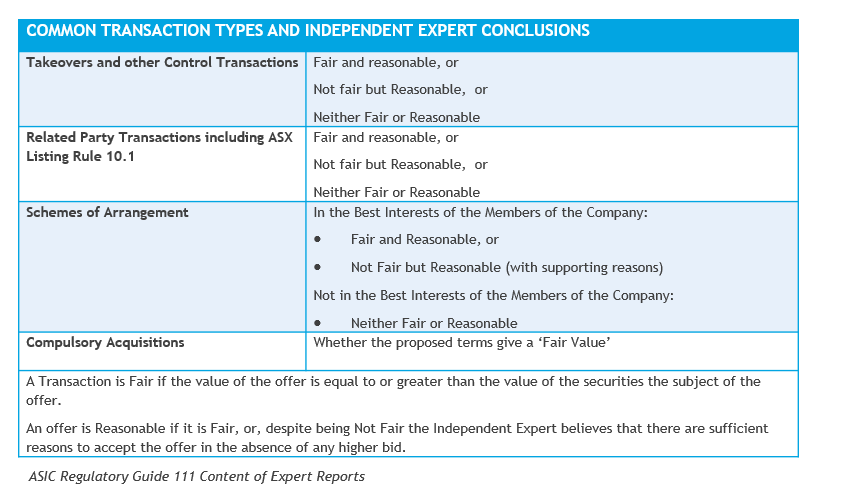

The Independent Expert values the corporate entity or entities using the asset values provided by the Technical Specialist and incorporating them into a chosen methodology. The approach is chosen by the Independent Expert and is dependent on the transaction type (takeover, related party, item 7 s611) and the requirements of the corporate regulator under ASIC Regulatory Guide 111 Content of Expert Reports.

Generally at least two valuation methodologies will be chosen by each expert. One approach is used as the primary, and the second as a cross-check. Differences in outcome are presented as a range and explained.

For example, a mining valuation Specialist will typically use at least two methodologies for each group of assets at similar stages of development (exploration, pre-development, development and production). The Independent Expert will then incorporate the Technical Specialist’s conclusion on value in at least one valuation approach.

The methodologies chosen will also depend upon the amount of data available, and its reliability.

Use of DCF

Questions often arise from mining and resources companies on when a DCF can be used as a methodology.

For mining and resources companies this is best understood by referring to ASIC Info Sheet 214 Mining and Resources – Forward looking statements. A Rule of Thumb however, is that we generally use a DCF for those projects that have a declared Ore Reserve as the work on these areas is likely to be sufficiently advanced to provide the greatest level of confidence that the underlying inputs, or assumptions are soundly based.

A Technical Specialist is engaged to review and assess the reasonableness of the technical inputs and assumptions within the company’s base cash flow model. For mining companies this is the resources, reserves, mining and processing physicals, production costs, operating costs, and capital expenditure used by the company in its base cash flow model.

As the Independent Expert, we provide the economic inputs for the model based on our host of research databases as well as our in-house economic and industry knowledge. These economic inputs include, but are not limited to, the discount rate, forecast pricing, forecast exchange rates and forecast inflation. The Independent Expert will also interrogate the model to ensure it is calculating correctly and will build in suitable sensitivities.

Using DCF when results are imminent

The challenge arises when a company is continuing to work on the project and an announcement on a Pre-Feasibility, Feasibility, or study upgrade is imminent. At the same time the company is in the midst of a transaction that requires an independent expert’s report.

Material results that are not sufficiently advanced or reliable to announce to the market, are generally not sufficiently reliable for the Independent Expert to use and publish in its report.

The Independent Expert is always very careful not to publish any confidential information in its report. Sometimes, a methodology other than DCF must be used unless the expert has the confidence that the results of a study will be finalised and disclosed before the IER is published.

In these circumstances it is important to be aware that after the announcement is made, and prior to the finalisation of the IER, the expert will need to check the previously provided draft information against the final information that is announced.

It is also important to be aware that any material information disclosed after the publication of an IER and before approval of the transaction or close of the offer may require a review of the IER and issue of a supplementary report by the Independent Expert. This is because the newly released information may be material to the content of the IER and the Independent Expert’s conclusions.

Follow these links to articles published by BDO after previous Independent Expert Report Breakfasts.

If you would like to get in touch to discuss any of the information contained here or have further questions around how we can help your business, please get in contact.

1 Report 659: ASIC regulation of corporate finance: July to December 2019

2 The VALMIN Code 2015 Edition – Australasian Code for Public Reporting of Technical Assessments and Valuations of Mineral Assets