Data quality in the age of mandatory carbon reporting

Data quality in the age of mandatory carbon reporting

When a business prepares its carbon footprint for the first time, various limitations, estimates, and assumptions are expected to be applied.

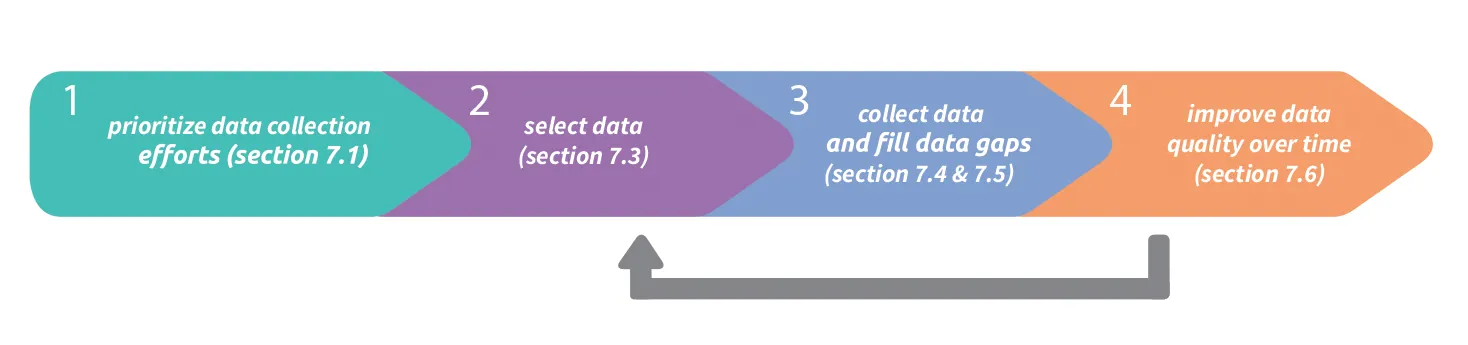

In fact, this expectation is so widely accepted by the industry that various tools have been built into the GHG Protocol: Corporate Value Chain (Scope 3) Accounting and Reporting Standard to assist businesses with effectively managing this challenge. The figure below summarises the processes outlined in the GHG Protocol, which is intended to provide guidance on moving from ‘reasonable estimate’ to ‘reliable data point’.

Figure [7.1] Iterative process for collecting and evaluating data

This is further underpinned by a set of data quality indicators, a list of criteria that should be used to assess the inputs into your carbon footprint measurement. These also provide useful guidance to determine appropriate assumptions when preparing estimates needed to fill data gaps.

Table [7.6] Data quality indicators

| Indicator | Description |

| Technological representativeness | The degree to which the data set reflects the actual technology(ies) used |

| Temporal representativeness | The degree to which the data set reflects the actual time (e.g., year) or age of the activity |

| Geographical representativeness | The degree to which the data set reflects the actual geographic location of the activity (e.g., country or site) |

| Completeness | The degree to which the data is statistically representative of the relevant activity. Completeness includes the percentage of locations for which data is available and used out of the total number that relate to a specific activity. Completeness also addresses seasonal and other normal fluctuations in data. |

| Reliability | The degree to which the sources, data collection methods and verification procedures used to obtain the data are dependable. |

The message is clear: if your business's carbon footprint isn’t perfect at first, that’s okay. In fact, it’s to be expected, and the GHG Protocol provides us with the tools to help manage this challenge.

However, now that we’re entering a new age of mandatory sustainability reporting, the implications are a bit more complex.

Following 31 December 2025, climate-related information that has never been required to be reported before will begin to be published. This information includes Scope 1 and Scope 2 GHG emissions in a business’s first year of reporting and Scope 3 GHG emissions in the second year of reporting. Target setting isn’t mandated; however, if a business has set targets, mandatory reporting requires these to be disclosed.

As information becomes more accessible, scrutiny over what is being reported – or potentially not reported if targets haven’t been set - is also expected to increase.

AASB S2 Climate-related Disclosures checklist

AASB S2 Climate-related Disclosures checklist

Support your climate reporting journey with a structured, step-by-step guide to AASB S2. Designed to help organisations meet Australia’s new sustainability standards with clarity and confidence.

Setting targets in an imperfect data world

So, we know that it’s acceptable to base your carbon footprint on reasonable estimates where data isn’t available. The following are trends a business should expect to see over time:

- The percentage of emissions derived from estimates decreases over time, as effort is invested in data collection activities

- The quality of data increases as more complete, reliable and appropriate data is collected

- The accuracy of your business’s carbon footprint increases.

The five data quality indicators from the GHG Protocol provide a framework for building confidence in your numbers, so you can set targets that drive real progress. But at what point is your business’s carbon footprint of sufficient quality to set meaningful targets?

The perfectionist: One approach involves developing and executing a comprehensive data collection and improvement strategy, including implementing controls, and then, once perfected, setting targets. This ensures that ROI against effort is accurately measurable; however, it may take multiple reporting cycles before target setting takes place.

The optimist: An alternative approach involves setting targets immediately and observing the impact of any data improvements, simultaneously with emissions reduction strategies. Stakeholder expectations can be effectively managed as targets, and the related progress against these can be reported; however, impacts may be difficult to attribute to initiatives, and insufficient internal controls may expose businesses to the risk of misreporting progress.

In reality, these represent opposite ends of a spectrum. As scrutiny increases over reporting and business contributions to climate action, most businesses will find they’re somewhere in between. As mandatory reporting approaches, has your business considered:

- How well does your team understand and apply data quality concepts?

- How is your business making use of the data quality tools laid out by the GHG Protocol to set your business up for success?

- Will your business’s first mandatory reporting period be the first year you calculate your carbon footprint?

Need help getting started?

Our team of sustainability experts is experienced in carbon accounting. Contact our team for pragmatic advice on improving the quality of your carbon footprint and setting your business up for success.

Need help? Download our structured, step-by-step guide to AASB S2. Designed to help organisations meet Australia’s new sustainability standards with clarity and confidence.