Expired leases in ‘hold over’ are not short-term leases

Expired leases in ‘hold over’ are not short-term leases

IFRS 16 Leases does not require short-term leases to be capitalised on the balance sheet, so there is a temptation to structure lease terms as being ‘month-to-month’ to apply this short-term lease exemption. Last month, we noted how month-to-month leases are not always short-term leases. This month, we tackle situations where leases are in ‘hold over’ status, and conclude that these are also not considered short-term leases.

What does it mean if your lease goes into ‘hold over’?

A ‘hold over’ period is the period during which the lease has expired, but its terms are still in effect. During the hold over period, the lessee continues to pay rent and maintain the premises as per the lease terms. The hold over period gives the lessee the opportunity to negotiate a new fixed-term lease with the lessor, or to find other premises. Without a hold over period, tenants would, in the absence of having formally signed a new lease, or modified the existing lease, be forced to vacate the premises on the date the lease expires.

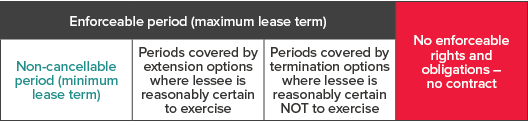

The hold over period is therefore essentially an extension option for the lessee.

How does the hold over period in a lease affect the lease term?

Although the hold over period is not part of the non-cancellable period of the lease (minimum lease term), entities should consider whether it forms part of the enforceable period (maximum lease term) because this will affect:

- How much to capitalise as the initial right-of-use asset and lease liability

- The amortisation period for the right-of-use asset.

IFRS 16, paragraph B34 notes that a lease is no longer enforceable when the lessee and lessor each have the right to terminate the lease without permission from the other party, with no more than an insignificant penalty.

Hold over periods generally do not continue indefinitely on a month-to-month basis. The lease term for month-to-month leases is determined as noted in our article, month-to-month leases are not always short-term leases. At the end of the hold over period, the lessee will have to vacate the premises. In a jurisdiction where the statutory hold over period is only six months, at the inception of the lease, a lessee may therefore assess that the lease is no longer enforceable during the hold over period because it has the right to terminate the lease, and any penalty would be insignificant.

Example 1 – Leasehold improvements

Entity A leases retail space in a shopping mall. The lease is for a non-cancellable period of five years, and the law in the jurisdiction where Entity A operates automatically allows for a six-month hold over period at the end of the lease. At the beginning of the lease, Entity A installs leasehold improvements with an economic life of five to six years.

In assessing the lease term at the beginning of the lease, Entity A determines that the lease term is only five years, being the non-cancellable lease period. This is because the store fit-out will be near the end of its useful life, so any penalty for exiting the lease will be insignificant.

Example 2 – Importance of asset to lessee’s operation (favourable shop location)

Assume the same facts as Example 1. In addition, Entity A’s retail shop is situated on a busy thoroughfare next to the anchor tenant and Entity A benefits from the increased foot traffic that this location has. In this case, Entity A determines that the lease term is five years and six months. This is because Entity A would incur a penalty that is more than insignificant if it were to vacate the store in a favourable location early.

Example 3 – Importance of asset to lessee’s operation (specialised equipment)

The Mining Entity is based in a remote area in Western Australia. It leases excavators for a non-cancellable period of two years, but the lead time for delivery of new replacement excavators is also two years.

In this case, the Mining Entity is likely to assess the lease term as four years at the inception of the lease, comprising the two-year non-cancellable period, plus the two-year hold over period. The hold over period is included in the lease term because if the Mining Entity terminates the lease after two years, it will be one excavator short and, therefore, will face significant economic penalties.

The hold over period is not a new short-term lease

In Examples 2 and 3 above, we assumed that the lessee included the hold over period in the lease term at inception because it anticipated that economic penalties from not continuing the lease for the hold over period, would be more than insignificant.

But what happens if the hold over period is not included in the initial lease term, and the lessee continues to occupy the leased premises or use the leased asset during the hold over period?

The hold over period is essentially an extension option for the lessee during which time negotiations for a subsequent lease take place. IFRS 16, paragraph 20 requires a lessee to reassess whether a lessee is reasonably certain to exercise an extension option upon the occurrence of a significant event or significant change in circumstances that:

- Is within the lessee’s control, and

- Affects whether the lessee is reasonably certain to exercise the extension option that was not previously included when determining the lease term.

Lessee reassesses the lease term before the end of the non-cancellable lease period

When a lease is approaching the end of the non-cancellable lease period, if it has not already done so, lessees must reassess the lease term in accordance with IFRS 16, paragraph 20. In Example 1 above, Entity A assessed the lease term as five years. Assume that after four years and nine months, Entity A decides to renegotiate a new lease for a similar space in the shopping mall. It anticipates that it will take most of the hold over period to complete the negotiations for a new lease. IFRS 16, paragraph 20, requires Entity A to reassess the lease term, with nine months remaining on the lease instead of three.

It is important to note that extending the lease for the hold over period is an extension option and not a new lease. The hold over period therefore cannot be accounted for as a short-term lease because it is not a new lease. Instead, Entity A will:

- Remeasure the remaining lease liability, including lease payments for the remaining nine months, discounted using a revised discount rate

- Recognise any difference between the carrying amount of the lease liability before and after remeasurement as an adjustment to the right-of-use-asset

- Extend the useful life of the right-of-use asset by an extra six months.

At first glance, it may seem that extending the lease term for a six-month or nine-month hold over period may not result in material adjustments to the right-of-use asset and lease liability. However, this may not always be the case. Particularly for retailers or other groups with multiple outlets and similar hold over terms in lease arrangements, adjustments can be material at a group level.

Lessee reassesses the lease term only once lease goes into hold over

Suppose the lessee only commences negotiations with the landlord once the lease has gone into hold over. In that case, an event has occurred that contractually obliges the lessee to exercise an option not previously included in the entity’s determination of the lease term (see IFRS 16, paragraph 21(c)). In Example 1 above, as soon as Entity A goes into hold over, it must reassess the remaining lease term as being for six months. Again, this is not a new short-term lease, but merely an extension of the original lease term. Therefore, Entity A cannot simply expense the remaining six months of lease payments. It must remeasure the lease liability and adjust the right-of-use asset as described above.

Similarly, if the lessee does not intend to negotiate with the landlord to enter a new lease but will remain in the premises until the end of the six-month hold over period, this is also not a short-term lease. The hold over period is an extension of the original lease term, and the lease liability is remeasured, with a corresponding adjustment to the right-of-use asset. The lease charges during the hold over period cannot be expensed as a short-term lease expense.

New lease renegotiated during the hold over period

If a new lease is negotiated during the hold over period for the same asset (i.e. the same retail store, or the same excavator as per our examples), this is accounted for as a lease modification and not a new lease. Our previous article contains more information on this.

More information

Our updated IFRS in Practice publication serves as a comprehensive guide featuring dozens of illustrative examples, flowcharts and practice aids to help you understand crucial topics in IFRS 16 such as lease term, lease payments, lease remeasurements and lease modifications.

Please also refer to the following articles for more information about lease accounting and examples of short-term leases:

- Month-to-month leases are not always short-term leases

- How does the short-term lease exemption work in IFRS 16?

- Think you don’t have a lease – Think again – Implications of the IFRIC agenda decision – Determining the ‘lease term’ for cancellable and renewable leases

- Entering into a new lease contract for the same premises before the end of the lease term is a lease modification.

Need assistance?

Our website contains information about how BDO can help you with your lease accounting. We have a cloud-based lease management system called ‘BDO Lead’ to help you manage the complexities around implementing IFRS 16 in practice. We also provide outsourced lease management services where we manage lease accounting on your behalf using BDO Lead.

Please contact BDO’s IFRS & Corporate Reporting team if you require assistance with your lease accounting.