More disclosure when presenting operating expenses by function under IFRS 18

More disclosure when presenting operating expenses by function under IFRS 18

IFRS 18 Presentation and Disclosure in Financial Statements, the new financial statements presentation standard that replaces IAS 1 Presentation of Financial Statements, will result in entities having to classify income and expenses in the statement of profit or loss in one of five categories, with special rules for the investing and financing categories of entities with specified main business activities. The five categories are: operating (a residual category if items don’t belong in any of the other four categories); investing; financing; discontinued operations; and income taxes.

Last month, we noted that operating category expenses on the face of the statement of profit or loss must be classified and presented in a way that provides the most useful structured summary of the expenses. This can be by nature, by function, or using a mixed presentation, with some expenses classified by nature and others by function.

This month, we illustrate some of the additional IFRS 18 disclosures required where an entity classifies some or all its expenses by function. When expenses are classified by function, entities aggregate different types (nature) of expenses to reflect the activities of the function. Examples of ‘by function’ expenses include cost of goods sold, research and development, occupancy, and administrative expense, etc.

Because of the lack of visibility over the types of expenses recognised in each function, IFRS 18 requires additional disclosure about the nature and amounts of expense items recognised in the operating category. These additional disclosures are discussed in more detail below.

Disclose total inventory expenses if there is a cost of sales function

If an entity presents a ‘cost of sales’ function in its statement of profit or loss, the ‘cost of sales’ line item must include the total of the inventory expense described in paragraph 38 of IAS 2 (refer paragraph 82(a) of IFRS 18). This includes:

- Costs of measuring inventory that has now been sold (for example, costs of purchasing or manufacturing finished goods)

- Unallocated production overheads and abnormal amounts of production costs of inventories (which were not previously included when measuring the cost of inventories).

Cost of sales may also include costs directly associated with fulfilling performance obligations under IFRS 15 Revenue from Contracts with Customers that have not been previously included in the measurement of inventory. For example, an entity that provides services to customers may include direct labour, direct materials and direct overheads as part of cost of sales. And in some cases, distribution costs might also be included where the entity has a separate performance obligation to physically transport goods to a customer.

What is included in each function line item?

If an entity presents any line items in the operating category of the statement of profit or loss by function, it must also disclose a qualitative description of the nature of expenses included in each function line item (refer to paragraph 82(b) of IFRS 18).

Example 1 – Qualitative description of functions

An example of this disclosure for Entity ABC is illustrated in footnotes (a) to (d) below.

|

|

$ |

|

Revenue |

4,000 |

|

Cost of sales (a) |

(1,000) |

|

Gross profit |

3,000 |

|

Occupancy (b) |

500 |

|

Sales and marketing (c) |

250 |

|

Administration (d) |

600 |

|

Operating profit |

1,650 |

|

Rental income from investment property |

350 |

|

Depreciation of investment property |

(100) |

|

Profit before financing and income taxes |

1,900 |

|

Notes:2

1: See paragraph 82(a) of IFRS 18 – cost of sales line must include the total inventory expensed 2: See paragraph 82(b) of IFRS 18 – qualitative description of the nature of expenses included in each function line |

|

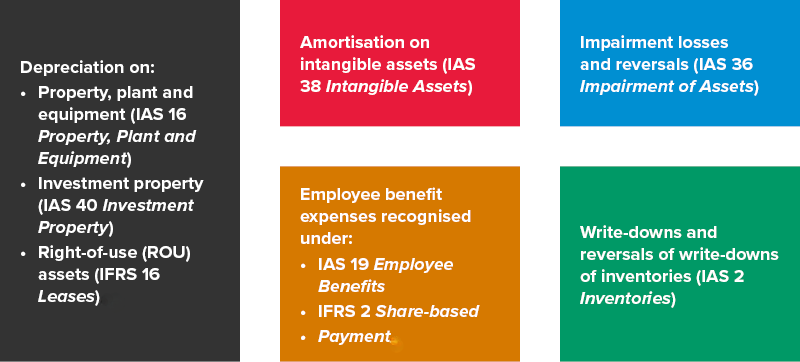

Specific expenses by nature

When the operating category in the statement of profit or loss includes line items of expenses that are classified by function, the entity must disclose, in a single note in the financial statements, the total for each of the following (refer paragraph 83 of IFRS 18):

In addition, for the items shown above, the entity must disclose:

- The amount related to each line item in the operating category

- A list of line items outside the operating category that include these expense/income items.

Example 2 - Specific expenses by nature (paragraph 83)

Entity ABC classifies all its operating expenses by function in its statement of profit or loss. It also owns an investment property, that generates returns independently of its other resources. Income and expenses relating to the investment property are, therefore, disclosed in the investing category in the statement of profit or loss.

Entity ABC’s statement of profit or loss is as shown in Example 1.

The table below illustrates how Entity ABC can present the disclosures required by paragraph 83.

|

|

Depreciation of PPE, investment property and ROU assets |

Employee benefits |

Impairment |

|

|

$ |

$ |

$ |

|

Operating category |

|

|

|

|

Cost of sales |

200 |

100 |

50 |

|

Occupancy |

100 |

- |

- |

|

Sales and marketing |

- |

150 |

- |

|

Administration |

200 |

200 |

100 |

|

Total operating Note 1 |

500 |

450 |

150 |

|

Investing category |

|

|

|

|

Depreciation of investment property Note 2 |

100 |

- |

- |

|

The amounts disclosed are those the entity recognised as expenses in the statement of profit or loss for the year, except for depreciation and employee benefits. The amounts disclosed for depreciation include amounts that have been capitalised by including them in the carrying amount of inventory at the end of the reporting period. Paragraph B84 permits this treatment because it says that the amounts disclosed under paragraph 83 need not be the amounts recognised as an expense in the period. They could include amounts that have been recognised as part of the carrying amount of an asset. The amounts disclosed for employee benefits are the costs incurred for the year, including for employee services, calculated in accordance with IAS 19 Employee Benefits and IFRS 2 Share-based Payment. These include amounts that have been capitalised by including them in the carrying amount of inventory at the end of the reporting period. Paragraph B84 permits this treatment because it says that the amounts disclosed under paragraph 83 need not be the amounts recognised as an expense in the period. They could include amounts that have been recognised as part of the carrying amount of an asset. Note 1: Paragraph 83(a) requires the total for each of the specific items listed in paragraph 83(a)(i) to (v) that are included in the operating category, i.e. depreciation, amortisation, employee benefits, impairment losses and reversals and write-downs of inventories and reversals. Note 2: Depreciation of investment property is not presented by function because it is classified in the investing category. Only expenses classified in the operating category may be presented by function. The disclosure of the amount of depreciation of investment properties is, therefore, not required to be disclosed under paragraph 83(b) or (b). |

|||

Do operating expense line items by function need to be disaggregated?

No. Although paragraph 41 of IFRS 18 has a general requirement for an entity to disaggregate items to provide material information, paragraph 84(a) provides exemptions to this rule.

Exception #1

Where an entity presents expenses in the operating category by function in the statement of profit or loss, it generally does not need to disclose disaggregated information for each function line item.

For example, if administration costs are a material amount, the entity need not provide a disaggregation in the notes to the financial statements which explains the nature and amount of each item making up administration costs. However, if administration costs include depreciation, the depreciation expense must be disclosed as noted in Example 2 above.

Exception #2

Where an entity presents expenses in the operating category by function in the statement of profit or loss, it may still be required by other IFRS® Accounting Standards to disclose by nature expenses. Examples include:

- Total share-based payment expenses (refer paragraph 51(a) of IFRS 2)

- Amounts of exchange differences recognised in profit or loss, except for those arising on financial instruments measured at fair value through profit or loss in accordance with IFRS 9 (refer paragraph 52(a) of IAS 21 The Effects of Changes in Foreign Exchange Rates)

- Losses on biological assets from the change in fair value less costs to sell (paragraph 40 of IAS 41 Agriculture).

However, the entity is not required to provide disaggregated information about the amounts of these expenses included in each function line in the operating category in the statement of profit or loss. It is only required to disaggregate nature expenses by function for the five types of expenses shown above.

Next month

Next month, we will use the same example to illustrate how the statement of profit or loss differs depending on whether the entity presents operating expenses by nature, by function, or using a mixed approach.

More information

You can find more articles about IFRS 18 challenges on our IFRS 18 topic page. Additionally, our publication and webinars will help you on your IFRS 18 implementation journey.