Specified main business activities under IFRS 18: Why they matter more than you might expect

In February, we continued our 2026 IFRS and Corporate Reporting webinar series with Business activities and IFRS 18: Why they’re central to implementation. That session focussed on one of the most consequential judgements entities will need to make when applying IFRS 18 Presentation and Disclosure in Financial Statements, whether they have a specified main business activity.

This assessment matters because IFRS 18 introduces different presentation requirements for entities with specified main business activities, meaning that income and expenses many users regard as part of “ordinary” operations may be presented differently depending on the outcome of that judgement. As a result, identifying an entity’s specified main business activities sits at the core of IFRS 18 implementation, influencing how performance is communicated in the statement of profit or loss.

This article builds on the themes explored in that webinar and outlines why specified main business activities are so significant, how entities assess whether they have one, and why conclusions may differ across entities within the same corporate group.

Identifying and assessing an entity’s specified main business activities

If an entity has one or both of the specified main business activities identified in IFRS 18, some of the general classification requirements for income and expenses in the statement of profit or loss will not apply. Instead, IFRS 18 includes specific presentation requirements for these entities that reflect the nature of their operating activities.

These requirements are designed to ensure that income and expenses that entities — and users of their financial statements — regard as part of ordinary operations are presented within operating results, rather than remaining in the investing or financing categories.

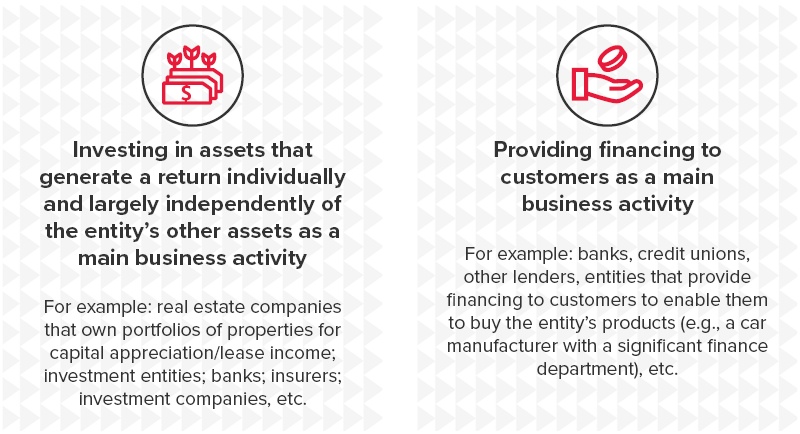

The following diagram illustrates the nature of the two specified main business activities.

The International Accounting Standards Board (IASB) introduced separate rules for entities with specified main business activities because applying the general IFRS 18 classification model would, in some cases, result in income and expense items being presented outside operating results, even if those items arise from activities the entity considers to be part of its core operations.

Such an outcome would be inconsistent with how these entities have historically reported performance, and with how users of their financial statements expect that performance to be presented.

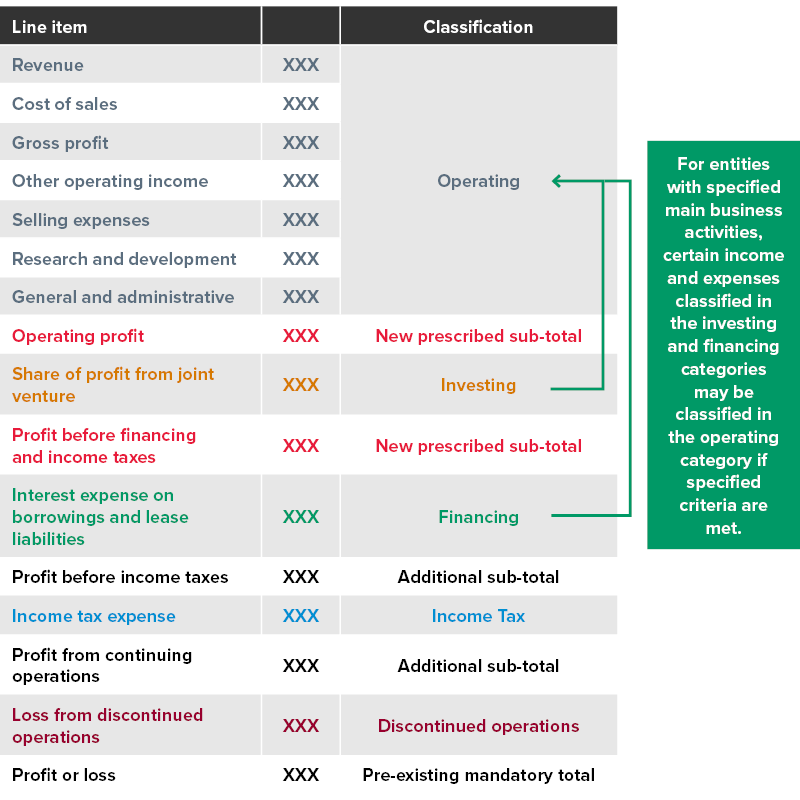

The following diagram demonstrates the potential impact of an entity having both of the specified main business activities on its classification of income and expense items under IFRS 18.

The assessment of whether an entity has specified main business activities is a matter of fact and not an assertion or an accounting policy choice. For those familiar with the investment entity classification in IFRS 10 Consolidated Financial Statements, the assessment of whether an entity has a specified main business is similar in the sense that it’s not optional for an entity to choose whether it has specified main business activities. If an entity concludes that it does have a specified main business activity, it must apply the requirements for entities with specified main business activities.

IFRS 18 identifies two key sources of evidence that entities consider when assessing whether they have one or both specified main business activities:

- Use of subtotals as an indicator of operating performance, including indicators used outside of the financial statements, and

- Operating segments identified under IFRS 8 Operating Segments.

Use of subtotals

With regards to the use of subtotals, IFRS 18 does not prescribe specific subtotals that conclusively demonstrate the existence of a specified main business activity. Nevertheless, subtotals similar to ‘gross profit’ are commonly used in some industries.

For example, banking and lending institutions often use a subtotal of interest income less interest expense, commonly referred to as ‘net financial margin’ or ‘net interest income’. Similarly, subtotals such as ‘net investment returns’ may indicate an entity’s focus on investing in particular classes of assets.

The use of such subtotals in external or internal communications may also indicate that an entity has one or both of the specified main business activities.

Operating segments

With regard to the role of operating segments for providing evidence of specified main business activities, IFRS 18 clarifies that:

- If a reportable segment comprises a single business activity, this indicates that the performance of the reportable segment is an important indicator of the entity’s operating performance and that the business activity of the reportable segment is a main business activity, and

- If an operating segment comprises a single business activity, this indicates that the business activity might be a main business activity of the entity if the performance of the operating segment is an important indicator of the entity’s operating performance.

Accordingly, operating segments may provide an important source of evidence of an entity’s main business activities, particularly where reportable segments comprise a single business activity and segment performance is an important indicator of operating performance.

In practice, however, judgement will often be required, particularly for entities that do not apply IFRS 8 or whose segments encompass multiple business activities.

Implications of specified main business activities for the preparation of individual, separate and consolidated financial statements

When assessing the existence of one or both of the specified main business activities, an entity is required to perform the assessment at the ‘reporting entity’ level. For some entities, particularly those within a wider corporate group that undertakes similar business activities, the conclusion might be consistent across the group. For others, however, the conclusion may change as the analysis moves up the corporate structure and incorporates additional entities.

Entities, therefore, need to be aware that:

- The group to which they belong may comprise different main business activities, some of which may be specified and some not, and

- Individual entities and subgroups within the wider corporate group may be required to present their profit or loss statement differently under IFRS 18 as compared to the way the entire group presents its consolidated profit or loss statement under IFRS 18.

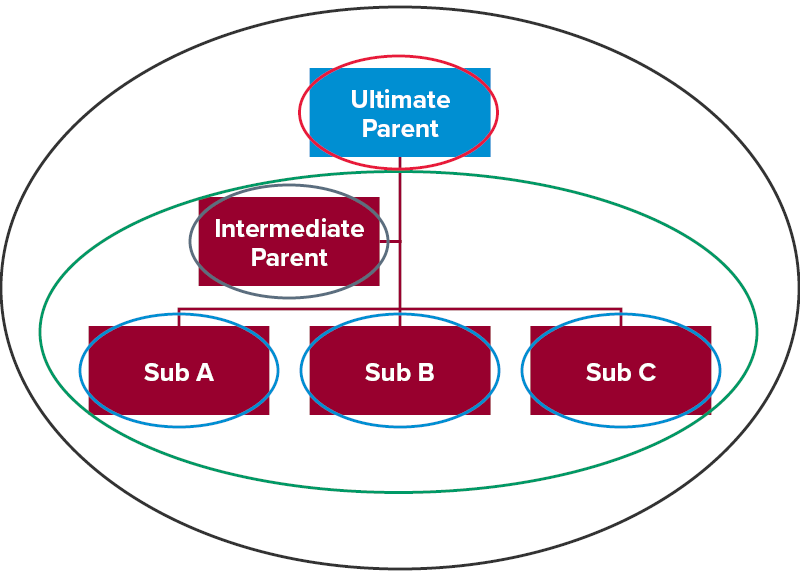

As a first step in assessing specified main business activities, a group should identify its reporting structure and determine whether it prepares:

- One set of group financial statements only

- Group financial statements plus one or more sets of consolidated financial statements for a subgroup

- Group financial statements plus separate (i.e., parent only) financial statements

- One of the above, plus individual financial statements for any or all group entities that are not parent entities.

The following diagram depicts the high-level implications of these decisions. Note that each circle represents a separate reporting entity, and therefore, a separate assessment of the entity’s main business activity is required for each.

Having identified all reporting entities within the group, the next step is to assess whether any of those entities have one or both of the specified main business activities.

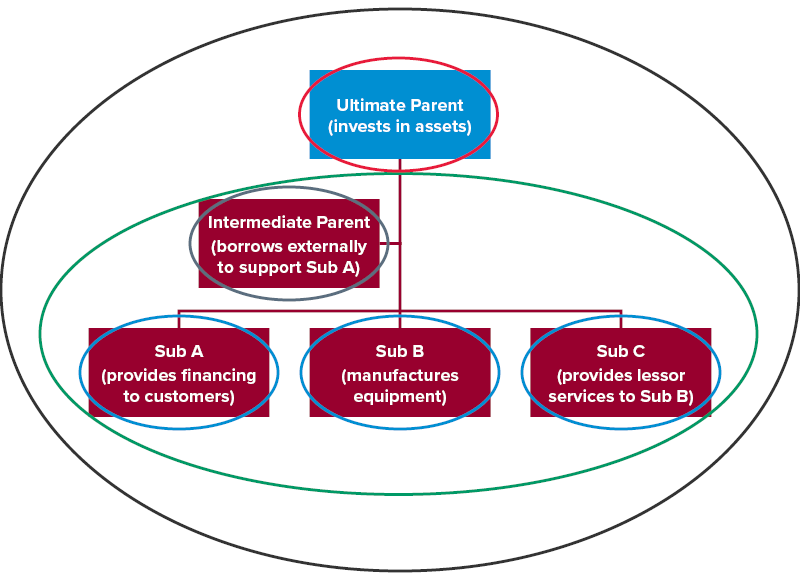

Each circle in the following diagram represents a separate reporting entity, and therefore, a separate assessment of the relevant entity’s main business activity is required.

Based on the diagram above, it might be concluded that:

- Sub A and Intermediate Parent both have the specified main business activity of providing financing to customers

- Sub B and Sub C have no specified main business activities

- Ultimate Parent has a specified main business activity of investing in subsidiaries

- The sub-group comprising Intermediate Parent and Sub A, Sub B and Sub C does not have a specified main business activity because providing financing to customers is not currently considered to be an important component of the operating performance of the group as a whole, and

- The group as a whole does not have a specified main business activity for the same reasons as outlined directly above.

This analysis can result in different presentation outcomes under IFRS 18, including:

- Presenting different profit or loss statements for the Ultimate Parent, Intermediate Parent and Sub A as compared to Sub B and Sub C and the group as a whole, and

- Restating the profit or loss presentations used by Ultimate Parent, Intermediate Parent and Sub A in line with those used by Sub B and Sub C and the group as a whole.

Implications of specified main business activities for the investing and financing categories

Please read our previous articles for a summary of investing and financing category differences for entities with specified main business activities.

Need help?

Preparing for IFRS 18 requires careful judgement, particularly when assessing specified main business activities and their impact on the presentation of financial performance.

We provide specialist support to entities preparing for audits or developing accounting position papers. Contact BDO’s IFRS & Corporate Reporting team to discuss how we can assist with assessing business activities, developing accounting policies and implementing IFRS 18 requirements.

We have also announced a series of IFRS 18 virtual masterclasses designed to support entities through key aspects of transition during 2026. These sessions focus on practical implementation considerations and worked examples.