Inclusion of assets under management in an entity’s value chain

Inclusion of assets under management in an entity’s value chain

Asset management entities (also referred to as fund managers) don’t typically operate businesses themselves. Instead, they pool funds invested by individual and/or institutional investors and manage those funds by investing in assets such as equity shares, debt instruments, commodities and real estate. Fund managers are responsible for choosing suitable investments to meet the investors’ risk and other objectives, and to comply with legal and regulatory requirements.

Typically, fund managers do not consolidate the funds that they manage for accounting purposes. As a result, the assets that they manage are not usually recognised in their statement of financial position.

Question

When preparing a sustainability report in accordance with AASB S2 Climate-related Disclosures for a fund manager, should assets under management that are not recognised in the statement of financial position be included in the fund manager’s value chain?

Example

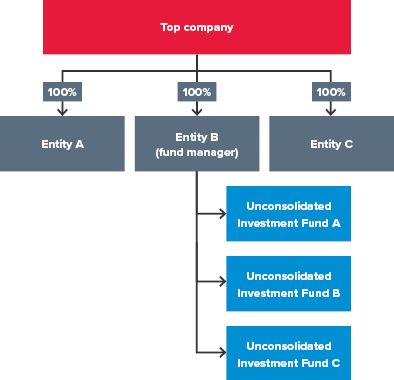

Assume the following group structure:

Entity B (the fund manager) is wholly owned by Top Company.

Investment funds A, B and C (the funds) are entities (e.g., special-purpose entities, legal entities, etc.) that hold certain financial assets.

Entity B performs the service of managing the underlying assets in the funds. Entity B does not consolidate the funds because it does not control them in accordance with IFRS 10 Consolidated Financial Statements.

Analysis

AASB S2, Appendix A, defines the term ‘value chain’ to include:

‘The full range of interactions, resources and relationships related to a reporting entity’s business model and the external environment in which it operates. A value chain encompasses the interactions, resources and relationships an entity uses and depends on to create its products or services…’

A fund manager’s business model relies on assets under management. Sustainability-related risks and opportunities that affect the performance of the assets under management also impact the asset manager through direct performance-based fees and reputational association.

In the above scenario, Entity B uses and depends on its assets under management to perform its functions of buying, selling and managing investments for its customers with the objective of generating profit/value on the underlying assets. Therefore, the assets under management (Unconsolidated Investment Funds A, B and C) could reasonably be expected to affect Entity B’s prospects. The assets under management are, therefore, a key component of Entity B’s business model.

Since assets under management are resources related to Entity B’s business model, and it uses and depends on these resources to perform its services, they form part of the value chain of a fund manager.

In accordance with the requirements of AASB S2, Appendix D, paragraph 17, materiality must still be assessed and considered when determining the sustainability-related risks and opportunities related to the assets under management that could reasonably be expected to affect the asset manager’s prospects.

It should also be noted that AASB S2, paragraph B61 requires entities that participate in asset management activities to provide additional disclosures. In particular, AASB S2, paragraph B61(b) requires disclosure of the amounts of assets under management.

How BDO can help

Preparing climate-related disclosures under AASB S2 requires careful judgement, particularly when assessing value chain boundaries, materiality and the treatment of assets under management.

Contact our sustainability reporting team to discuss how we can support your carbon accounting and AASB S2 reporting journey.