Preparing your first mandatory sustainability report: Bringing it all together

Preparing your first mandatory sustainability report: Bringing it all together

BDO’s sustainability webinar series breaks down the complex world of sustainability, making it a little easier for you to understand the basics and begin driving change within your organisation.

November’s webinar focused on pulling together all elements for your first mandatory sustainability report under AASB S2 Climate-related Disclosures (AASB S2).

For some Group 1 entities, the clock is ticking with reporting deadlines of 31 December 2025. The good news?

AASB S2 offers transitional relief and flexibility to make this process more manageable. From temporary exemptions, like excluding Scope 3 emissions and comparatives in the first year, to practical ways of applying requirements based on your resources, these measures are designed to provide flexibility without compromising compliance, helping entities manage the complexity of AASB S2 reporting.

What matters most: Materiality and transparency

AASB S2 is designed to ensure climate-related risks and opportunities are disclosed in a way that enables stakeholders to make informed decisions. The focus is on risks and opportunities that could reasonably affect your organisation’s prospects, such as cash flow, access to finance, or capital costs, over the short, medium, or long term.

Disclosures should reflect market expectations, not just internal views. Even if a risk is considered low-impact, explain why and outline the controls in place to monitor and mitigate any potential changes. This transparency builds trust and demonstrates a proactive approach.

Key reliefs and mechanisms for first-time preparers

In the first year of application, transitional reliefs provide a “soft landing” to help organisations implement new reporting practices without being overwhelmed.

This means in the first year:

- Scope 3 disclosures are not enforced

- No comparative figures are required

- Existing frameworks (e.g., ISO) are accepted for measuring greenhouse gas (GHG) emissions.

Proportionality mechanisms also support organisations facing resource or data limitations. They don’t add new disclosure requirements or excuse compliance; instead, they allow entities to apply AASB S2 in a way that reflects available skills and capabilities. This flexibility helps organisations navigate complexity during the initial reporting period.

Proportionality in practice

These mechanisms help entities meet disclosure requirements in a way that reflects their capabilities.

| AASB S2 requirement | Reasonable and supportable information available without undue cost or effort | Commensurate with the skills, capabilities and resources that are available to the entity |

|---|---|---|

| Identification of climate-related risks and opportunities | ✓ | |

| Scope of the value chain | ✓ | |

| Anticipated financial effects | ✓ | ✓ |

| Approach to climate-related scenario analysis | ✓ | ✓ |

| Measurement of Scope 3 greenhouse gas emissions | ✓ | |

| Metrics in cross-industry metric categories | ✓ |

Reporting greenhouse gas emissions: Key requirements

A key focus area is understanding the requirements for disclosing greenhouse gas emissions under AASB S2. Here’s what first-time preparers need to keep in mind:

- Scope 1 and 2 emissions: You’ll need to report these in detail, disaggregating between your consolidated accounting group (parent and subsidiaries) and other investees (such as associates). For Scope 2, only location-based emissions are required; you should also include any relevant contractual instruments.

- Scope 3 emissions: For your first report, you’re required to provide the total Scope 3 emissions and list the categories included (but you don’t need to break down emissions by category). If you’re in asset management, commercial banking, or insurance, there are additional requirements for financed emissions.

- Reporting approach matters: The way you define your reporting boundary—whether you use an operational control or financial control approach—affects what gets included.

Scenario analysis and climate resilience

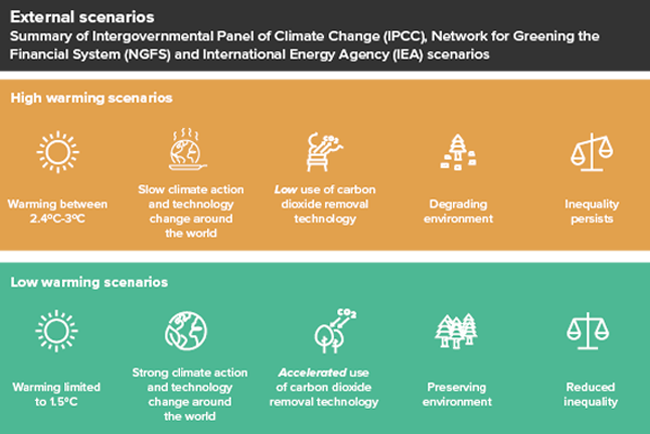

A key requirement under both the Corporations Act and AASB S2 is for entities to assess their climate resilience using scenario analysis. This means evaluating how the organisation would fare under at least two climate scenarios:

- High global warming scenario: Global average temperature rises by 2.5°C or more.

- Low global warming scenario: Global average temperature rise is limited to 1.5°C.

The purpose of this analysis is to test the resilience of the entity’s strategy and operations against a range of plausible climate futures. Entities must disclose the outcome of this resilience assessment—summarising how their business would be impacted under each scenario and what this means for their long-term prospects. However, they are not required to publish the full technical details or modelling behind the analysis.

Importantly, the scenarios used should be based on credible, publicly available sources, such as the Intergovernmental Panel of Climate Change (IPCC), Network for Greening the Financial System (NGFS), or International Energy Agency (IEA), and the assessment should cover both physical and transition risks. The focus is on providing stakeholders with a clear understanding of the organisation’s preparedness for climate-related risks and opportunities, rather than on the technical process itself.

Current and anticipated financial effects

When preparing your sustainability report, it’s essential to consider how climate-related risks and opportunities could impact your financial statements, such as profit and loss, cash flow, and the balance sheet. These impacts may be short, medium or long-term, and should inform both your resilience and strategic planning.

Even if calculating exact figures is challenging, you are still required to disclose relevant information. Where precise data isn’t available, explain the assumptions made, why certain data is missing and any potential effects on your financial statements. This level of transparency not only supports compliance with AASB S2 but also helps stakeholders understand and assess any potential impacts.

Practical tips for your first sustainability report

1. Make your report easy to navigate

Clearly label each disclosure and cross-reference it to the relevant AASB S2 requirements. This helps stakeholders and auditors quickly find information and demonstrates your commitment to transparency.

2. Focus on what’s material

Prioritise disclosures that reflect the most significant climate-related risks and opportunities for your organisation. Don’t get bogged down in immaterial details—clarity and relevance are key.

3. Be transparent about limitations

If you don’t have all the data or if estimates are required, explain your assumptions, any gaps, and how you plan to improve data quality over time. Transparency builds trust and supports compliance. For example, if you are unable to provide precise Scope 3 emissions data due to supplier data gaps, state this clearly in your report and outline your plan to improve data collection in future reporting periods.

4. Use credible scenario sources

When conducting scenario analysis, base your assessment on publicly available, reputable scenarios, such as those from the Intergovernmental Panel on Climate Change (IPCC), Network for Greening the Financial System (NGFS), or International Energy Agency (IEA). Summarise the outcomes clearly, even if you don’t include all the technical details.

5. Leverage transitional relief and proportionality mechanisms

Take advantage of the flexibility offered in the first year—such as exemptions for Scope 3 emissions and comparatives—and apply proportionality mechanisms where resources or data are limited.

6. Keep your process iterative

Treat your first report as a foundation. Plan to revisit and refine your disclosures as your organisation’s capabilities, data, and understanding of climate risks evolve.

Ready to prepare your first mandatory sustainability report?

Our national sustainability team can help. We’re here to guide you through every step, from understanding the AASB S2 requirements to scenario analysis and disclosures.

Contact our national sustainability team to chat about how we can help you create reporting that is clear, complies with AASB S2, and will support your company’s climate goals.