How the statement of profit or loss differs when expenses are presented by nature, function, or both

How the statement of profit or loss differs when expenses are presented by nature, function, or both

In previous editions of Corporate Reporting Insights, we discussed how IFRS 18 Presentation and Disclosure in Financial Statements, the new financial statements presentation standard that replaces IAS 1 Presentation of Financial Statements, will result in entities having to classify income and expenses in the statement of profit or loss in one of five categories, with special rules for the investing and financing categories of entities with specified main business activities.

The five categories for classifying income and expenses in the statement of profit or loss are:

- Operating (this is a residual category if items don’t belong in any of the other four categories)

- Investing

- Financing

- Discontinued operations

- Income taxes.

Present expenses in the operating category by nature, function or both

Unlike IAS 1 Presentation of Financial Statements, IFRS 18 permits a mixed presentation of expenses in the operating category. Entities must classify and present expenses in separate line items to provide the most useful structured summary. This can be done using one or both of the following characteristics:

- Nature of the expenses, or

- Function of the expenses within the entity.

Example illustrating expenses by nature, by function, or using a mixed presentation

Example 4.4-2 in our publication shows how the operating category in the statement of profit or loss will differ, depending on whether the entity determines that a by nature, function, or mixed presentation format provides the most useful structured summary of expenses.

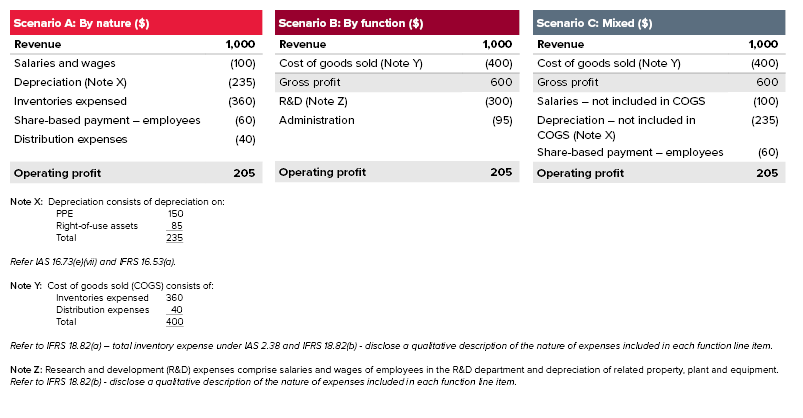

Fact pattern

Retail Entity D has applied the classification requirements of IFRS 18 and classified the following expenses into the operating category (all amounts in thousands of $):

- Salaries and wages (IAS 19) 100

- Depreciation (IAS 16) 150

- Inventories expensed (IAS 2) 360

- Distribution expenses (shipping goods to customers) 40

- Share-based payments to employees (IFRS 2) 60

- Depreciation of right-of-use assets (IFRS 16) 85

Entity D also earned $1,000 of revenue.

Analysis

The diagram below reflects a summary of the operating category in the statement of profit loss, under three mutually exclusive scenarios:

- Scenario A: All expenses are presented by nature

- Scenario B: All expenses are presented by function

- Scenario C: Cost of goods sold is presented by function, with all other expenses presented by nature.

Retail Entity D does not have a free choice of which presentation method to use; however, these scenarios are included to demonstrate the effect of the different presentation methods, as well as judgements made by Retail Entity D in determining how much information to present in the statement of profit or loss and the corresponding notes.

There are a few key observations to note regarding the above three scenarios:

There are a few key observations to note regarding the above three scenarios:

- Operating profit is always the same at an amount of $205

- Gross profit in Scenarios B and C is also the same, as that section of the operating category is presented by function in both instances

- Gross profit is an optional additional sub-total. Only ‘operating profit or loss’ is mandatory under paragraph 69(a) of IFRS 18

- Salaries, depreciation and share-based payment expense are the same across both Scenarios A and C, as that section of the operating category is presented by nature in both cases

- As Retail Entity D is a retail entity, it is assumed that ‘cost of goods sold’ comprises the only purchase cost of finished goods inventories ($360) as well as distribution expenses ($40). In other words, there is no manufacturing, and therefore, no allocation of salaries and depreciation to the ‘cost of goods sold’ expense.

Scenario A: All expenses by nature

The following additional disclosures are required by other IFRS® Accounting Standards (if material):

- IAS 16 Property, Plant and Equipment, paragraph 73(e)(vii): Disaggregated information about the depreciation expense for each class of property, plant and equipment. Refer to Note X in the diagram above. This is not an IFRS 18 requirement

- IAS 2 Inventories, paragraph 36(d): Amount of inventories recognised as an expense during the period (this has been shown on the face of the statement of profit or loss).

However, the disclosures in paragraphs 82 and 83 of IFRS 18 are not required because Retail Entity D is not presenting any line items in the operating category that comprise expenses classified by function.

Scenario B: All expenses by function

In this scenario, Retail Entity D discloses all its expenses by function, so it must also disclose:

- In the ‘cost of goods sold’ line in the statement of profit or loss, the total of inventory expense described in paragraph 38 of IAS 2 (refer paragraph 82(a) of IFRS 18). This is the total of:

- Costs previously included in the measurement of inventory that have now been sold

- Unallocated production overheads and abnormal amounts of production costs of inventories (N/A in this case, as Retail Entity D does not manufacture goods)

- If the circumstances warrant, other amounts, such as for distribution costs

- A qualitative (narrative) description of the nature (types) of expenses included in each function line item required by paragraph 82(b) of IFRS 18 (refer to Note Y for the cost of goods sold function and Note Z for the R&D function)

- In a single note, the total for each of the following expenses recognised in the operating category for each function: i.e. depreciation; amortisation; employee benefits; impairment losses and reversals; and write-downs of inventories and reversals. This disclosure is required by paragraph 83 of IFRS 18 but has not been illustrated here. Please refer to Example 2 in our previous article for an illustration of this.

Scenario C: Mixed presentation

If applicable, the relevant additional disclosures referred to in Scenarios A and B must be included, for example:

- Total inventory expense and a narrative description of the nature of expenses included in the cost of goods sold function (refer to Note Y above)

- Depreciation disclosures required by IAS 16 (refer Note X above).

However, as Retail Entity D is a retail entity, and it is assumed that there is no manufacturing, and therefore, no allocation of salaries and depreciation to the ‘cost of goods sold’ expense, the additional by nature disclosure of salaries, depreciation, etc. in a single note (paragraph 83) is not required because there is no allocation of these expenses across functions.

More information

You can find more articles about IFRS 18 challenges on our IFRS 18 topic page. Additionally, our publication and webinars will help you on your IFRS 18 implementation journey.

Need help

Our recent articles on IFRS 18 demonstrate the complexity of applying IFRS 18 in practice. Reach out to our team of experts for assistance with understanding the latest requirements in IFRS 18.