Approved changes to climate-related disclosure requirements in Australia

Approved changes to climate-related disclosure requirements in Australia

On 15 December 2025, the Australian Accounting Standards Board (AASB) approved amendments to AASB S2 Climate-related Disclosures, aligning with similar recent amendments to the IFRS® Sustainability Disclosure Standard, IFRS S2. The Australian amendments have been published by the AASB as an amending standard, AASB S2025-1 Amendments to Greenhouse Gas Emissions Disclosures.

This is a welcome development for Group 1 Australian entities and groups that must prepare their first climate-related financial disclosures for periods beginning from 1 January 2025. In particular, in the short-term, groups with jurisdictional emissions reporting obligations in parts of their organisation won’t have to calculate greenhouse gas (GHG) emissions twice. From the second year of reporting, the amendments reduce the reporting burden for the disaggregated Scope 3 disclosures by entities participating in financial activities, such as asset management, commercial banking, and insurance.

When do the amendments apply?

The amendments apply to annual periods beginning on or after 1 January 2027.

Can the amendments be adopted early?

Yes. Entities can choose to early adopt the amendments provided that:

- The directors document their decision for early adoption in writing (see section 336A of the Corporations Act 2001), and

- The sustainability report discloses the fact that the amendments have been adopted early (see paragraph C1B of AASB S2).

Are there any transitional requirements?

There are three transitional requirements that apply to first-time adoption of these amendments:

- If the entity has changed the way it measures GHG emissions as a result of applying the relief in amendments 1. (jurisdictional relief) and 2. (global warming potentials) below, it must adjust comparative information for the preceding period.

- If the entity disclosed Scope 3 GHG emissions in the previous period, it must adjust the comparative information, providing the total Category 15 emissions as well as the subtotal of financed emissions included in this total (see amendment 3. below).

- If the entity disclosed disaggregated financed emission information by industry in the preceding period, it must adjust the comparative information to reflect the industry classification system it selected for the current period (see amendment 4. below).

Is it worth early adopting the amendments for Group 1 entities?

We recommend that Group 1 entities adopt these amendments early, as failing to do so will result in complex and duplicative reporting in the first year. In addition, emissions measurements and disclosures will need to be updated from 1 January 2027 anyway, and comparatives will have to be restated on transition.

Early adoption from 1 January 2025 sets the scene for consistent emissions measurement going forward and will alleviate the need for restatement if only adopted from 1 January 2027.

In addition, we expect that Group 1 entities will apply the transitional relief, and therefore will not disclose Scope 3 emissions in the first year ending 31 December 2025. Adopting these amendments early means that Scope 3 emissions will be measured and disclosed as noted in amendments 3. and 4. below for the year ending 31 December 2026, alleviating the need for comparative restatement if the changes were only adopted from 1 January 2027.

Four amendments

The four amendments are discussed briefly below:

- When to use jurisdictional requirements for measuring GHG emissions rather than the GHG Protocol

- Using global warming potential (GWP) values other than those from the latest Intergovernmental Panel on Climate Change assessment

- Measuring Scope 3 Category 15 GHG emissions

- Use of classification systems for disclosing industry information about financed emissions.

1. When to use jurisdictional requirements rather than the GHG protocol

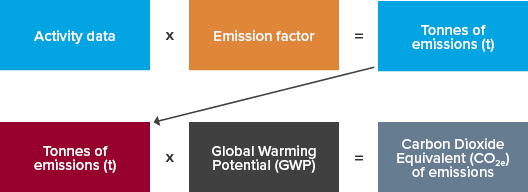

Entities reporting climate-related financial information under AASB S2 must disclose their absolute gross GHG emissions generated during the reporting period, expressed as metric tonnes of CO2 equivalent. The absolute gross emissions must be disclosed separately for Scope 1, Scope 2 and Scope 3 emissions.

Paragraph 29(a)(ii) requires GHG emissions to be measured in accordance with the Greenhouse Gas Protocol: A Corporate Accounting and Reporting Standard (the GHG Protocol). This applies unless a jurisdictional authority or listed exchange requires the use of a different method (alternative method). This implies an ‘all or nothing’ approach such that an entity must either apply the GHG Protocol, or an alternative method to the whole entity.

What’s changed?

Entities will be able to measure GHG emissions using the GHG Protocol for some parts of their business and an alternative method required by a jurisdictional authority or listed exchange for other parts.

How will the amendment impact Australian entities?

Heavy emitters currently reporting their Scope 1 and Scope 2 emissions under the National Greenhouse and Energy Reporting Act 2007 (NGER reporters) for a particular facility will be able to report GHG emissions under AASB S2 using the methodology set out in the National Greenhouse and Energy Reporting (Measurement) Determination 2008 because this measurement approach is required by a jurisdictional authority.

However, they will use the GHG Protocol to measure:

- Scope 3 emissions for these heavy emitters because the National Greenhouse and Energy Reporting Act 2007 does not address Scope 3, and

- Scope 1, Scope 2 and Scope 3 emissions for parts of the business that are not NGER reporters.

2. Using global warming potential (GWP) values other than those from the latest Intergovernmental Panel on Climate Change assessment

As noted above, entities reporting climate-related financial information under AASB S2 must disclose the absolute gross GHG emissions generated during the reporting period, expressed as metric tonnes of CO2 equivalent. This involves converting the six constituent greenhouse gases into CO2 equivalent values, in order to add to the seventh greenhouse gas (CO2).

The seven constituent greenhouse gases are carbon dioxide (CO2), methane (CH4), nitrous oxide (N2O), hydrofluorocarbons (HFCs), perfluorocarbons (PFCs), sulphur hexafluoride (SF6), and nitrogen trifluoride (NF3).

Entities using direct measurement methods to calculate their GHG emissions will convert the seven constituent greenhouse gases into a CO2 equivalent as follows:

Global warming potential (GWP) values are based on a 100-year time horizon contained in the latest Intergovernmental Panel on Climate Change (IPCC) assessment available at the reporting date. At the time of writing, this refers to the IPCC Sixth Assessment Report.

What’s changed?

Entities required, in whole or in part, by a jurisdictional authority or a listed exchange to use different GWP values for converting the seven constituent gases into CO2 equivalent values will be permitted to do so. In all other instances, entities must use the latest IPCC assessment available (currently the IPCC Sixth Assessment Report).

How will the amendment impact Australian entities?

Legislation governing NGER reporters currently contains GWP values from the IPCC Fifth Assessment Report, which is embedded in Section 2.02 of the National Greenhouse and Energy Reporting Regulations 2008. Without this amendment, NGER reporters would have to measure GHG emissions twice: firstly, for NGER reporting using GWP values from the IPCC Fifth Assessment Report; and then again for AASB S2 reporting using GWP values from the IPCC Sixth Assessment Report, resulting in duplicate reporting and the need for two different systems to measure GHG emissions.

3. Measuring Scope 3 Category 15 GHG emissions

Entities must include all 15 categories referenced in the GHG Protocol when measuring the absolute gross Scope 3 GHG emissions generated during the reporting period.

Category 15 Scope 3 emissions are GHG emissions arising from an entity’s financial investments (including loans) that are not already included in its Scope 1 or Scope 2 emissions. These are also referred to as ‘financed emissions’ in AASB S2. Entities participating in financial activities such as asset management, commercial banking and insurance, would be expected to have significant Category 15 Scope 3 emissions.

AASB S2 requires additional disclosures about Category 15 Scope 3 GHG emissions for entities whose activities include asset management, commercial banking, and insurance, including breaking them down into the Scope 1, Scope 2, and Scope 3 emissions of related investees and borrowers.

The Basis for Conclusions to IFRS S2, paragraphs BC127-BC129, notes that disclosure of GHG emissions relating to derivatives, facilitated emissions and insurance-associated emissions is not required. However, there is a potential conflict with the requirement in paragraph 29(a)(i)(3) to measure the absolute gross Scope 3 emissions, including Category 15 emissions. Paragraph 29(a)(i)(3) is silent on whether derivatives and facilitated and insurance-associated emissions must be included or excluded when measuring Scope 3 Category 15 GHG emissions.

What’s changed?

The amendment addresses the inconsistency described above for entities involved in asset management, commercial banking, and insurance activities.

Firstly, entities will be able to measure and disclose the gross absolute Scope 3 Category 15 emissions under paragraph 29(a)(i)(3) by:

- Including only financed emissions (facilitated emissions and insurance-associated emissions may be excluded)

- Excluding emissions associated with derivatives.

Financed emissions include emissions relating to loans and investments made by the entity to investees or counterparties, including loans, project finance, bonds, equity instruments and undrawn loan commitments. For an entity that participates in asset management, it also includes emissions attributed to assets under management.

Additional disclosure is required as follows:

- A description of the financial activities excluded from its measure of Scope 3 Category 15 GHG emissions (e.g. facilitated emissions from investment banking activities and emissions from insurance underwriting activities)

- Explanation of what the entity has treated as excluded derivatives. For example, the entity could explain that it treated items as derivatives that meet the definition of a derivative in accordance with IFRS® Accounting Standards or other applicable generally accepted accounting principles or practices (GAAP) when preparing the related financial statements

- The total Category 15 emissions and the subtotal of financed emissions included in the total Category 15 emissions.

Secondly, the amendments clarify that the additional disaggregated disclosures about investees’ emissions in Category 15, Scope 3 GHG emissions, are limited to only financed emissions.

4. Use of classification systems for disclosing industry information about financed emissions

AASB S2 requires entities involved in commercial banking and insurance activities to disclose disaggregated information about the Scope 1, Scope 2 and Scope 3 emissions of investees for each industry (paragraphs B62-B63). Industry classification is based on the latest version of the Global Industry Classification Standard (GICS) available at the reporting date. Some of these entities may not currently use GICS as an industry-based classification system, which could result in additional licensing costs and duplicative reporting.

What’s changed?

Commercial banking and insurance entities will not have to automatically use GICS to determine industry classifications. Instead, these entities must select an industry classification system that enables them to classify investees or counterparties, allowing users to understand the entity’s exposure to climate-related transition risks. Key points to note in this regard:

- A classification system that is commonly used by other entities in the same industry or jurisdiction (commonly used system) is more likely to support the comparability of information between entities than a system used only by the entity (entity-specific system).

- If a commonly used system enables the entity to provide useful information about its exposure to climate-related transition risks, the entity would usually prioritise that system.

- An entity can use different classification systems to classify investees or counterparties for its commercial banking and insurance activities.

Entities will also have to disclose which industry-classification system they used to disaggregate financed emissions, as well as provide information for users to understand how the classification system chosen fulfils the above requirements.

More information

Our previous article answers your questions about mandatory sustainability reporting, and our website contains additional resources for sustainability reporting and measuring your carbon footprint.

Need help?

Our sustainability reporting and carbon accounting experts are always available to assist with your sustainability reporting journey. Contact us for help.

Subscribe to receive the latest BDO News and Insights

SUBSCRIBE