GHG Protocol - Overview of Scope 3 emissions

GHG Protocol - Overview of Scope 3 emissions

In the second half of 2023, our sustainability webinar series walks step-by-step through the GHG Protocol. Aletta Boshoff and Dylan Byrne summarise the key messages from the second part of our September event, which provides an overview of Scope 3 emissions.

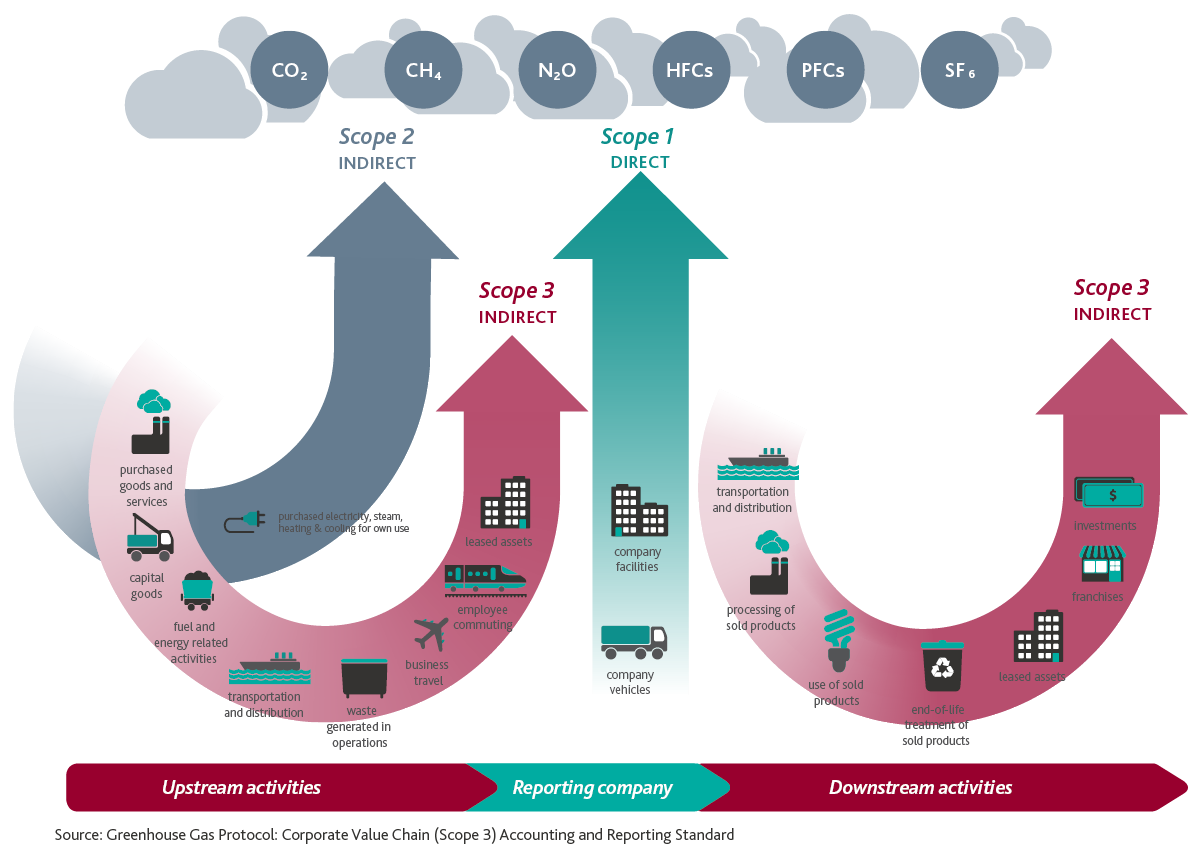

Upstream versus downstream emissions

When entities quote their Scope 3 emissions as part of their carbon footprint, it is important to understand the difference between upstream and downstream Scope 3 emissions. Whilst both are indirect emissions, if you are providing Scope 3 emissions data on a ‘cradle to gate’ basis, you will only be considering your upstream emissions. However, if using a ‘cradle to grave’ method, you will be looking at both your upstream and downstream emissions.

There are a total of fifteen possible categories of Scope 3 emissions – eight upstream and seven downstream:

Upstream emissions

- Purchased goods and services (catch-all category if emission does not belong in categories 2-7)

- Capital goods (includes intangible assets)

- Fuel and energy-related activities that are not included in Scope 1 or Scope 2

- Upstream transportation and distribution for products purchased that are not transported in company vehicles (when company vehicles are used, they are classified as mobile combustion Scope 1 emissions)

- Waste generated in operations

- Business travel

- Employee commuting

- Upstream leased assets (as lessee).

Downstream emissions

- Downstream transportation and distribution

- Processing of sold products

- Use of sold products

- End-of-life treatment of sold products

- Downstream leased assets (as lessor, emissions when lessee uses our assets)

- Franchises’ emissions

- Investments (emissions of investees).

Time boundaries

The GHG Protocol is designed to account for all emissions related to the reporting company’s activities in the reporting year (e.g. emissions related to products purchased or sold in the reporting year).

For some Scope 3 categories, emissions occur simultaneously with the activity (e.g. from combustion of energy), so emissions occur in the same year as the company’s activities.

However, for other Scope 3 categories, emissions may have occurred in previous years or may be expected to occur in future years because the activities in the reporting year have long-term emissions impacts. For these categories, reported emissions have not yet happened, but are expected to happen when waste is generated, investments are made, and products are sold in the reporting year. For these categories, the reported data should not be interpreted to mean that emissions have already occurred, but that emissions are expected to occur due to activities that happened in the reporting year.

Want to understand more about the GHG Protocol?

Register now for the remaining events in BDO's sustainability webinar series.

If you need a hand in identifying and measuring your Scope 3 emissions, our national sustainability team can help. Contact us today.