Ten things to remember when preparing 31 December 2021 annual and half-year financial reports

The good news for most preparers is that there are only minor changes to accounting standards for 31 December 2021 reporting. However, you need to bear in mind several other recent developments when preparing your 31 December half-year or annual reports. This article summarises ten key things to remember.

Please refer to our recent webinar, Getting Ready for 31 December 2021 for more information. Our Illustrative Financial Statements for the Year Ended 31 December 2021 and 31 December 2021 Illustrative IFRS Disclosures – COVID Supplement may also assist when preparing your 31 December 2021 financial statements.

- Are you transitioning to Simplified Disclosures early?

- New standards

- Rent concessions

- New IFRIC agenda decisions – SAAS, supply chain financing arrangements and more

- ASIC focus areas and FAQs (including impairment and amortisation of bed licences)

- Listed entities

- Casual entitlements – do you need to reverse provisions created at 31 December 2020?

- COVID-19 government stimulus measures

- Climate-related matters reporting

- Not-for-profit entities (NFPs).

Are you transitioning to Simplified Disclosures early?

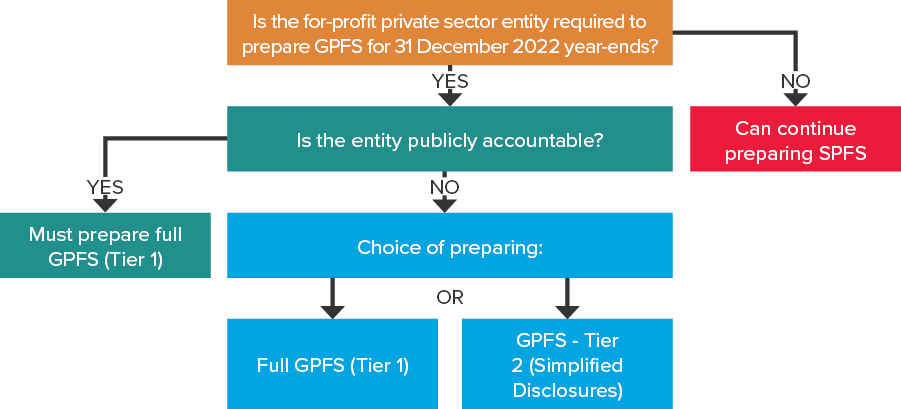

While not mandatory for 31 December 2021, some for-profit private sector entities that previously prepared special purpose financial statements (SPFS) will have to prepare general purpose financial statements (GPFS) for 31 December 2022 (refer to February 2021 Accounting News article for more information on which for-profit private sector entities must prepare GPFS from 2022).

If the entity is not a ‘publicly accountable entity’, these GPFS can be prepared according to the new Tier 2 regime for general purpose financial reporting called ‘Simplified Disclosures’.

‘Publicly accountable’ entities include listed entities, unlisted disclosing entities, entities holding assets in a fiduciary capacity for a broad range of outsiders as one of its primary businesses (e.g. banks, credit unions, insurance companies, etc.), co-operatives that issue debentures, registered managed investment schemes and APRA-registered superannuation funds.

The following types of entities that previously prepared SPFS will need to prepare GFPS for the year ending 31 December 2022:

- Unlisted public companies

- Large proprietary companies (including ‘grandfathered entities’)

- Small proprietary companies raising money via crowd-sourced funding

- Small foreign controlled proprietary companies preparing financial statements under Chapter 2M of the Corporations Act 2001

- Certain AFS licensees reporting under Chapter 7 of the Corporations Act 2001.

- Foreign registered companies with no overseas requirement to prepare financial statements (section 601CK(5), (5A) and (6) of the Corporations Act 2001).

These entities are not usually ‘publicly accountable’ so have the option to prepare Tier 2 general purpose financial statements using the Simplified Disclosures contained in AASB 1060 General Purpose Financial Statements – Simplified Disclosures for For-Profit and Not-for-Profit Tier 2 Entities.

Advantages of early adopting Simplified Disclosures

There are significant advantages for entities moving to Simplified Disclosures early (i.e. for the year ending 31 December 2021), including relief from presenting all comparative disclosures, as well as (in some circumstances) not having to restate comparatives in the primary financial statements. Refer to the following Accounting News articles for more information:

- Why you should consider transitioning from special purpose to Tier 2 general purpose financial statements one year early

- Comparatives when for-profit entities transition to Simplified Disclosures.

Not just a disclosure exercise

While transitioning to Simplified Disclosures may simply be a ‘disclosure exercise’ for entities currently applying all recognition and measurement requirements of Australian Accounting Standards (including presenting consolidated financial statements if applicable), it is a complex process for other entities. If you did not previously comply with all the recognition and measurement requirements, you will need to make decisions regarding the best transition method (i.e. applying IAS 8 or IFRS 1), as well as the various transition exemptions.

Need help?

If you require assistance, refer to our Five steps to successful GPFS transition. Following these five simple steps can help to ensure you avoid unnecessary speed bumps in your GPFS transition journey. Our team of IFRS specialists across Australia can help you take the wheel, and guide your entity to its destination.

More information

For more information, please refer to our recent webinar Applying IFRS 1 to transition to general purpose financial statements and our February 2021 Accounting News article, Key questions to ask when getting ready for general purpose financial statements.

New standards

The table below highlights amending standards that apply for the first time to annual and half-year periods ending 31 December 2021.

Standard number | Standard name | Applies to periods | Annual | Half-year periods |

AASB 2020-4 | Amendments to Australian Accounting Standards – COVID-19-Related Rent Concessions | Beginning on or after 1 June 2020 | ✓ | × |

AASB 2021-3 | Amendments to Australian Accounting Standards – COVID-19-Related Rent Concessions beyond 30 June 2021 | Beginning on or after 1 April 2021 | Recommend to adopt early for 31 December 2021 | ✓ |

AASB 2020-8 | Amendments to Australian Accounting Standards – Interest Rate Benchmark Reform – Phase 2 | Beginning on or after 1 January 2021 | ✓ | × |

AASB 2021-4 | Amendments to Australian Accounting Standards – Modified Retrospective Transition Approach for Service Concession Grantors | Ending on or after 30 June 2021 | ✓ | - |

We expect to see the amendments for rent concessions affecting a number of entities given the extended lockdowns experienced in New South Wales and Victoria during 2021. For more information, refer to discussion at Rent concessions below.

Rent concessions

Many lessors granted rent concessions to lessees during this COVID-19 pandemic period, resulting in either the waiver or deferral of lease payments (or both).

Implications for lessees

The original practical expedient contained in IFRS 16, paragraph 46A, only permitted lessees to avoid having to apply modification accounting to leases where the reduction in lease payments as a result of COVID-19 rent concessions affected lease payments originally due on or before 30 June 2021. Applying the original practical expedient would have resulted in adjustments to the lease liability recognised in profit or loss rather than against the right-of-use asset, and no change to the discount rate.

After subsequent ‘waves’ of COVID-19 restrictions and lockdowns, many lessors provided rent concessions extending beyond 30 June 2021. The IASB therefore extended the practical expedient to apply to rent concessions affecting lease payments originally due on or before 30 June 2022.

Note that the extended practical expedient must be applied consistently to eligible contracts with similar contracts and in similar circumstances, regardless of whether the rent concession becomes eligible because of the original practical expedient or the extended practical expedient. Our Accounting News article includes examples of when the extended practical expedient would and wouldn’t apply.

The following Accounting News articles provide worked examples to explain the accounting for different types of rent concessions. These could apply equally to the initial or extended practical expedient:

- Example – Waiver of rentals (June 2020)

- Example – Deferral of lease payments (June 2020)

- Example – Lessee choose to pay half rental during COVID-19 period, with waiver only formally agreed by lessor at a later date (June 2020)

- Example – Deferral of rental payments for six months and lease term extended by six months (July 2020)

- Example - Deferral of rental payments for six months – recouped over remainder of lease with additional interest on deferred payments to compensate for time value of money (July 2020)

More information is also available in our International Financial Reporting Bulletins:

- IFRB 2020/08 IASB issues amendments to IFRS 16: COVID-19-related rent concessions

- IFRB 2020/11 Accounting for rent concessions: Lessee FAQs

Our Accounting News article, IASB extends practical expedient for COVID-19 rent concessions until 30 June 2022 and International Financial Reporting Bulletin, IFRB 2021/08 COVID-19-related rent concessions beyond 30 June 2021: Extension of practical expedient – Additional FAQs provide more information regarding the extended practical expedient.

Implications for lessors

COVID-19 rent concessions also cause headaches for landlords trying to grapple with the appropriate accounting under IFRS 16. The following Accounting News articles summarise BDO’s FAQs to assist in accounting for rent concessions within the context of existing IFRS 16 requirements and ASIC’s comments noted in its FAQ 9B<.

Article | Topic | Title | Source – Accounting News |

1 | FAQs to assist in accounting for rent concessions | Implications of COVID-19 for lessors - Your questions answered | July 2020 |

2 | Amendment to BDO’s FAQ 1.2 in article 1 above | February 2021 |

New IFRIC agenda decisions – SAAS, supply chain financing arrangements and more

Entities should not overlook two important agenda decisions made by the IFRS Interpretations Committee over the past year that could have a material impact on your 31 December 2021 financial statements (annual or half-year). These are:

- Configuration or customisation costs in a cloud computing arrangement (April 2021)

- Supply chain financing (reverse factoring) arrangements (December 2020).

Configuration or customisation costs in a cloud computing arrangement

Entities using cloud-based software in a Software as a Service (SaaS) arrangement may incur significant costs in relation to configuration and customisation of the supplier’s application software to which they receives access.

SaaS arrangements are usually accounted for as service contracts and not as intangible assets (refer IFRIC agenda decision – March 2019). Even though an intangible asset is not recognised in the balance sheet for the SaaS arrangement, in the past, some companies have nevertheless capitalised configuration and customisation costs relating to these arrangements as ‘intangible assets’.

These retrospective adjustments are treated as a change in accounting policy because the IFRIC decision is merely clarifying the accounting treatment for a transaction that was previously contentious, i.e. it is not accounted for as an error. However, ASIC’s FAQ 9D notes that where only some amounts were identified and expensed at 30 June 2021 as a change in accounting policy (for example, in 30 June 2021 half-year financial statements), any further amounts identified and expensed at 31 December 2021 would be treated as errors (i.e. you can only have a change in accounting policy once).

Refer to our May 2021 Accounting News article for an explanation of the April 2021 IFRIC agenda decision regarding configuration and customisation costs in a SaaS arrangement.

Supply chain financing (reverse factoring) arrangements

This December 2020 IFRIC agenda decision outlines how IFRS standards already provide guidance on the appropriate accounting classification and disclosures for reverse factoring arrangements and considers the following questions:

- Should the reverse factoring arrangements be classified as trade payables or as borrowings in the balance sheet?

- How should these arrangements be presented in the cash flow statement?

- What additional disclosures are required about reverse factoring arrangements?

Refer to our April 2021 Accounting News article for more information.

Other IFRIC agenda decisions

Entities may also need to consider whether other IFRIC agenda decisions could affect 31 December 2021 financial statements:

| Decision | Accounting News articles & other resources |

Non-refundable value added taxes on leases | Non-refundable value added taxes on leases (November 2021) |

Accounting for warrants that are classified as financial liabilities on initial recognition | Accounting for warrants that are classified as financial liabilities on initial recognition (November 2021) |

Costs necessary to sell inventories | Latest IFRIC agenda decisions – Costs necessary to sell inventories & non-going concern financial statements (July 2021) |

Non-going concern financial statements | Latest IFRIC agenda decisions – Costs necessary to sell inventories & non-going concern financial statements (July 2021) |

ASIC focus areas and FAQs (including impairment and amortisation of bed licences)

Preparers should also take note of ASIC’s focus areas for its surveillance of 31 December 2021 financial reports that include:

- Asset values - including impairment of non-financial assets, values of property assets, expected credit losses on loans and receivables, and values of other assets such as inventories (and whether all expected estimated costs of completion and costs necessary to make the sale have been taken into account in determining net realisable value)

- Provisions - including make good/restoration provisions, and provisions for onerous contracts, financial guarantees and restructuring

- Solvency and going concern assessments

- Subsequent events

- Disclosures in the financial report and the Operating and Financial Review (OFR) – non-IFRS financial information should not be presented in a potentially misleading manner, and for material amounts of COVID support received such as JobKeeper, land tax relief, loan deferrals, rent concessions, etc., the dates and amounts involved must be disclosed

- SAAS costs - capitalised costs relating to configuring and/or customising supplier’s application software should be written off if required by the recent IFRIC agenda decision (as noted above)

- Off-balance sheet arrangements and whether exposures should be recognised on the balance sheet

- Future services to be provided by a vendor in a business combination

- Written put options over non-controlling interests in a subsidiary.

Further information is included in ASIC’s Media Release MR21-342 ASIC highlights focus areas for 31 December 2021 financial reports under COVID-19 conditions.

ASIC has also published FAQs regarding COVID-19 implications for financial reporting and audit. Given the decision by the Australian Government to scrap the need for bed licences by 1 July 2024, aged care providers need to take note of ASIC’s comments in FAQ 9D regarding amortisation and impairment of bed licences. Please refer to our October 2021 Accounting News article for more information.

Listed entities

We remind listed entities that received JobKeeper payments during the 31 December 2021 financial year to submit your s323DB JobKeeper notice with the ASX within 60 days of lodging your 31 December 2021 annual report.

We also draw your attention to a new disclosure requirement for your remuneration report that stems from ASX Listing Rule 10.15.11, rather than s300A of the Corporations Act 2001. Where securities (shares/options/rights) were granted to a director or a person in a position of significant influence during the year, the remuneration report must disclose that these grants were approved at an AGM under ASX Listing Rule 10.14.

Casual entitlements – do you need to reverse provisions created at 31 December 2020?

Good news for employers with a large casual workforce: you may be able to remove provisions for employee entitlements from the balance sheet that were previously recognised under IAS 37 Provisions, Contingent Liabilities and Contingent Assets because of the WorkPac Pty Ltd v Rossato case (Rossato decision). This is due to two recent events, i.e. recent legislation and a High Court decision, which may result in some entities no longer needing these provisions in December 2021 financial statements. Please refer to our August 2021 Accounting News article for more information.

COVID-19 government stimulus measures

A number of government stimulus measures have been on offer for businesses during the COVID-19 pandemic and these may present accounting challenges. Please refer to past Accounting News articles for more information on how to account for these different types of stimulus measures in your 31 December 2021 financial statements:

| Topic | Title | Source – Accounting News |

Loss carry backs | May 2021 | |

Instant asset write-offs | ‘Instant asset write-offs’ and interaction with accounting for research and development incentives | May 2021 |

SME loan guarantee scheme | Accounting for COVID-19 government stimulus measures – COVID SME Guarantee Scheme | August 2020 |

May 2021 | ||

JobMaker | Accounting for Federal Budget economic recovery stimulus measures – JobMaker Hiring Credit | November 2020 |

December 2020 | ||

Land tax rebates (Queensland) | Accounting for land tax rebates received by landlords and the impact on outgoings audits | October 2020 |

JobKeeper | May 2020 | |

Accounting for JobKeeper and JobMaker where employee costs have been capitalised | December 2020 |

Climate-related matters

Even though IFRS standards do not refer explicitly to climate-related matters, there is increasing awareness that such issues may have an impact on financial reporting. With this in mind, the IASB released educational materials summarising how companies must consider climate-related matters when applying IFRS standards.

Businesses should consider the educational materials when preparing 31 December 2021 financial statements because these matters may have a material impact, including when determining values for assets, liabilities and provisions, and well as when making disclosures regarding estimates and judgements.

Please refer to BDO's IFRB 2020/14 for a summary of these materials.

Not-for-profit entities (NFPs)

In addition to the above matters, NFPs should consider the following when preparing 31 December 2021 financial statements.

Simplified Disclosures for Tier 2 general purpose financial statements (GPFS)

For years ending 31 December 2022 onwards, NFPs preparing Tier 2 GPFS using the Reduced Disclosure Requirements (RDR) will need to transition to Simplified Disclosures. There may be some Simplified Disclosures not required for RDR, so additional information might be needed, including for comparative note disclosures.

Refer to our May 2021 Accounting News article, Transitional relief now available for NFPs moving from RDR to Simplified Disclosures for more information.

Recognition and measurement disclosure

NFPs continuing to prepare SPFS must disclose the extent to which they have complied with the recognition and measurement requirements of Australian Accounting Standards. Refer to AASB 1054, paragraph 9A for more details.

ACNC Best Practice revenue disclosures

Almost half of the revenue recognised in the charity sector comes from government. In order to improve transparency, the Australian Charities and Not-for-Profits Commission (ACNC) published a Best Practice Guide that recommends the following three best practice disclosures regarding government funding:

- If 10% or more of total revenue received is from government, information about sources of government revenue as follows:

- Total revenue from each level of government (e.g. Commonwealth, State, Local Council)

- Amount of revenue received from each government department/agency (including name, up to a maximum of 10 lines else provide in an Appendix)

- Revenue from providing goods/services to beneficiaries who receive related financial assistance from government (e.g. from NDIS)

- Economic dependency on government revenue

- Funding received from government not yet recognised as revenue.

For more information, please refer to the Best Practice Guide and our February 2021 Accounting News article, ACNC’s best practice financial report disclosures – start the new year on the right foot.

Portable long service leave provisions

In some circumstances, NFPs operating in the community services sector may be required to recognise long service leave provisions in their balance sheet, despite the fact that all, or a portion of long service leave entitlements may be recoverable from the portable long service leave authority. Please refer to our Accounting News article for more information.

Need help?

If you require assistance with your year-end reporting, please contact a member of BDO’s IFRS & Corporate Reporting team.