NFPs - Allocating the transaction price to performance obligations under AASB 15

For annual periods beginning on or after 1 January 2019, not-for-profit entities (NFPs) will need to reassess all grant contracts and other receipts to determine whether these should be accounted for as revenue under the new revenue standard, AASB 15 Revenue from Contracts with Customers, or as income under the new income standard, AASB 1058 Income of Not-for-Profit Entities.

| Revenue (AASB 15) | OR | Income (AASB 1058) |

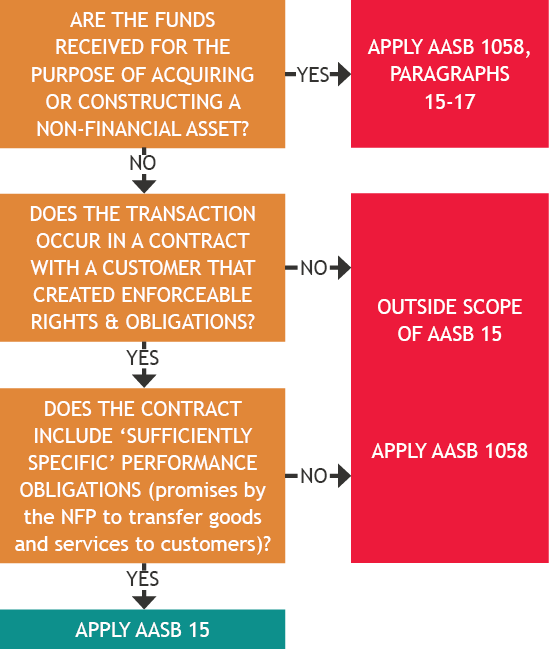

If the funds are granted for the purpose of constructing a non-financial asset, the transaction is accounted for under the specific requirements in AASB 1058, paragraphs 15-17. The receipt is initially recognised as a liability and transferred to income when (or as) the NFP satisfies its obligation to build the non-financial asset.

However, if the NFP satisfies the remaining two criteria on the above diagram, i.e. there is an enforceable contract with a customer, and the contract contains ‘sufficiently specific’ performance obligations, then the grant is accounted for under AASB 15.

To date, Accounting News has included the following articles on accounting under AASB 15 vs AASB 1058:

| Topic | Accounting News… |

| Is there an enforceable contract with a customer? | November 2018 |

| How to identify ‘sufficiently specific’ performance obligations when assessing whether AASB 15 or AASB 1058 applies | February 2019 |

| Grants to NFPs to deliver IP to a customer | April 2019 |

| Grants to NFPs to transfer a licence to a customer | May 2019 |

| Grants to NFPs to transfer research findings to a customer | June 2019 |

| Grants to NFPs to transfer research findings to a customer | July 2019 |

Once established that a grant should be accounted for under AASB 15, we need to consider how the transaction price is allocated to the various performance obligations (Step 4 of the five-step revenue recognition model in AASB 15).

More than one performance obligation

Where a NFP receives a grant containing more than one ‘sufficiently specific’ performance obligation, it applies the same ‘for-profit’ principles for allocating the transaction price to performance obligations contained in IFRS 15, paragraphs 73-90. For more information on this allocation process, please refer to our articles in June and July 2019 Accounting News. However, things become tricky when grants are received for a dual purpose.

Dual purpose grants

Sometimes customers may enter into contracts with NFPs with a dual purpose, i.e. to obtain goods and services, and also to help the NFP achieve its objectives.

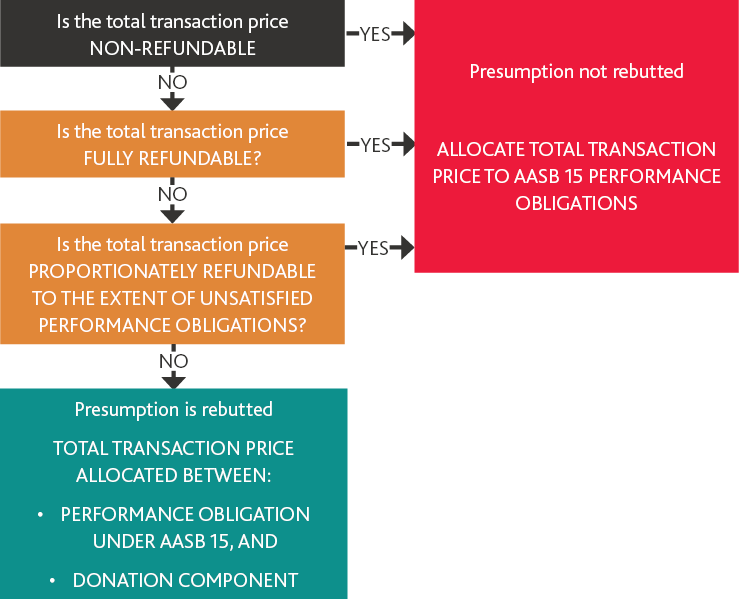

The NFP will allocate the transaction price between performance obligations in a way that depicts consideration to which the NFP expects to be entitled in return for transferring the promised goods or services.

However, there is a rebuttable presumption that the transaction price is wholly related to the transfer of goods or services.

The presumption is only rebutted where the transaction price is partially refundable in the event the entity does not deliver the promised goods and services (AASB 15, Appendix F, paragraph F29). That is, paragraph F29 suggests that only the non-refundable component of the transaction price could be accounted for under AASB 1058 as a donation.

Assuming the contract is enforceable (regardless of whether there is a refund obligation or not), and there are ‘sufficiently specific’ performance obligations, the following decision tree illustrates how this rebuttable presumption works when allocating the transaction price under AASB 15:

Where the presumption is rebutted (i.e. the grant is partially refundable), NFPs will need to disaggregate the transaction price between the component that relates to the transfer of promised goods and services, and the remainder is accounted for as a donation under AASB 1058 (the non-refundable component).

Indicators that the grant may include elements that are not related to the promised goods or services, and therefore more likely to be for the purpose of the NFP furthering its objectives are:

- Part of the transaction price is non-refundable

- The NFP has ‘deductible gift recipient’ status (the donor can claim part of the transaction price as a tax deduction for a donation).

Example 1 (Based on AASB 15, Appendix F, paragraph F32) – Donation component

NFP Heritage Foundation sells on-line subscriptions for $250 that provide access for 12 months to particular heritage sites (promised service to each customer).

Prior to finalising their payments for these on-line subscriptions, subscribers are also invited to donate $10 (which is non-refundable) to assist the foundation in pursuing its mission.

Because the price for the annual subscription is separately identifiable from the price for the donation, in this case, NFP will account for the transaction as follows:

- The on-line subscription purchase as revenue under AASB 15 over the 12-month period, and

- The donation as income under AASB 1058.

Example 1A (Based on AASB 15, Appendix F, paragraph F32) – Presumption not rebutted - No donation component

NFP Heritage Foundation sells on-line subscriptions for $250 that provide access for 12 months to particular heritage sites (promised service to each customer).

Prior to finalising their payments for these on-line subscriptions, subscribers are also invited to donate $10 to assist the foundation in pursuing its mission.

Both amounts are refundable if access is not provided to the heritage sites.

In this case, the presumption in paragraph F28 cannot be rebutted because both amounts are fully refundable.

The total transaction price for the on-line subscription purchase is therefore $260.

It should be noted that the presumption is also not rebutted (and therefore no donation recognised) where:

- Both elements are equally proportionately refundable to acknowledge access already provided during the year, or

- Neither element were refundable.

Example 2 (Based on AASB 15, Appendix F, Illustrative Example 6) – Presumption not rebutted - No donation component

Kids Dance School sells chocolates in a fundraising drive to raise money for costumes for the annual Christmas concert.

Chocolates are sold for a greater margin than a supermarket would typically generate by selling chocolates, however, customers are often motivated by the dance school’s benevolent aims.

Customers are entitled to a full refund if the chocolates were ordered and paid for in advance, and either the chocolates were spoiled or Kids Dance School was unable to deliver them.

Kids Dance School determines that this transaction is accounted for under AASB 15 because:

- There is an enforceable contract with a customer due to the return obligation, and

- The requirement to transfer chocolates to the customer is a ‘sufficiently specific’ performance obligation which is satisfied at the time of delivery.

The presumption in paragraph F28 cannot be rebutted because the transaction price is not partially refundable. Therefore the entire proceeds, including the proceeds from the additional margin, form part of the transaction price that is allocated to the performance obligation (delivery of chocolates).

Example 3 (Based on AASB 15, Appendix F, Illustrative Example 7) – Presumption rebutted – Includes a donation component

The Children’s Hospital holds an annual fundraising dinner.

The ticket price is $600 per head. If the dinner is cancelled, customers will receive a refund of $300 per ticket.

The retail price of the dinner at a local restaurant is $200 per ticket.

Hosting the dinner also provides customers with the benefit of socialising with a wide range of celebrities and high profile business identities (including networking). The amount of consideration to which The Children’s Hospital expects to be entitled in exchange for transferring the promised goods or services (the dinner and networking) to the customer is $250.

The Children’s Hospital determines that this transaction is accounted for under AASB 15 because:

- There is an enforceable contract with a customer due to the return obligation, and

- The requirement to provide the dinner and networking to the customer is a ‘sufficiently specific’ performance obligation which is satisfied at the point in time when provided.

The presumption in paragraph F28 is rebutted because there is a partial refund in the event of non-performance (i.e. a $300 refund) and the element not related to the performance obligation is considered material.

For each ticket sold, The Children’s Hospital recognises:

- A contract liability of $250 in accordance with AASB 15 (representing future delivery of the dinner and networking), and

- Income recognised immediately of $350 in accordance with AASB 1058 because the consideration provided by the entity of $250 (dinner and networking) is significantly less than the fair value of the $600 cash received, principally to enable the entity to further its objectives and therefore AASB 1058 applies.

The journal entry to recognise the receipt when tickets are purchased is:

| Dr ($) | Cr ($) | |

| Cash | 600 | |

| Contract liability | 250 | |

| Income – AASB 1058 | 350 |

On the date that the dinner is held and the networking provided, The Children’s Hospital will recognise the following journal entry:

| Dr ($) | Cr ($) | |

Contract liability | 250 | |

Revenue – AASB 15 | 250 |

A refund obligation for the $300 per ticket is recognised only to the extent that the entity does not expect to retain the refundable amount, for example, because the dinner is cancelled. In that case, the subsequent journal entry to recognise the refund is:

| Dr ($) | Cr ($) | |

| Contract liability | 250 | |

| Income – AASB 1058 | 50 | |

| Cash | 300 |

This results in a net donation of $300 per ticket, reflecting the net cash received after each ticket refund has been made.

Concluding thoughts

From 1 January 2019, NFPs will need to undergo a formal assessment of all income streams to assess whether recognition under AASB 1058 or AASB 15 is appropriate. Where it is concluded that AASB 15 applies, additional work will be required to allocate the transaction price to ‘sufficiently specific’ performance obligations, and in some cases, to donation income as well.

This is analysis is neither a quick nor simple exercise. We therefore recommend that management of NFPs commence a detailed review of all contracts and agreements as soon as possible.