NFPs – Refund obligations are not automatically ‘sufficiently specific’ performance obligations under AASB 15

For annual periods beginning on or after 1 January 2019, not-for-profit entities (NFPs) will need to reassess all grant contracts and other receipts to determine whether these should be accounted for as revenue under the new revenue standard, AASB 15 Revenue from Contracts with Customers, or as income under the new income standard, AASB 1058 Income of Not-for-Profit Entities.

Revenue (AASB 15) | OR | Income (AASB 1058) |

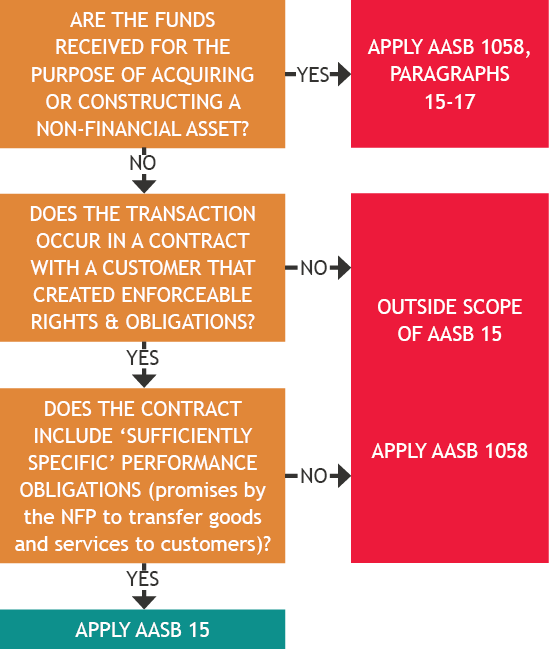

If the funds are granted for the purpose of constructing a non-financial asset, the transaction is accounted for under the specific requirements in AASB 1058, paragraphs 15-17. The receipt is initially recognised as a liability and transferred to income when (or as) the NFP satisfies its obligation to build the non-financial asset.

However, if the funds are granted for a purpose other than to acquire or construct a non-financial asset, using the above decision tree, NFPs will need to determine whether these are accounted for under:

- AASB 15 as revenue from contracts with customers (i.e. there is an enforceable contract with a customer, and the contract includes ‘sufficiently specific’ performance obligations), or

- AASB 1058 (as income).

Please refer to the following previous articles in Accounting News for more information on what we mean by ‘sufficiently specific’ performance obligations.

| Topic | Accounting News… |

| Is there an enforceable contract with a customer? | November 2018 |

| How to identify ‘sufficiently specific’ performance obligations when assessing whether AASB 15 or AASB 1058 applies - overview | February 2019 |

| Grants to NFPs to deliver IP to a customer | April 2019 |

| Grants to NFPs to transfer a licence to a customer | May 2019 |

| Grants to NFPs to transfer research findings to a customer | June 2019 |

| Grants to NFPs to transfer research findings to a customer | July 2019 |

| Allocating the transaction price to performance obligations under AASB 1058 | August 2019 |

What is a refund obligation?

Many grant contracts currently include a refund obligation whereby the recipient is obligated to return any unspent grant funds to the grantor in the following types of scenarios:

- Grant monies have not been spent by a particular date, and/or

- Grant monies have not been spent for the purpose set out in the contract.

How have grants with refund obligations been accounted for to date?

Under AASB 1004 Contributions and/or AASB 118 Revenue, many NFPs recognise grants received on a deferred basis.

What’s changed?

AASB 1058, paragraph B14 articulates that simply having a refund obligation in a grant contract does not automatically mean grant income is deferred and recognised over an extended period of time. This concept is particularly important for NFPs receiving upfront cash for multi-year grants. The rationale for this is that the NFP always has the discretion whether to spend the money or not, and therefore a liability does not exist unless the breach has occurred or is expected to occur.

An entity typically has the ability, through its own actions, to avoid the circumstances that would give rise to a breach of conditions or requirements in an agreement necessitating a return of funds received. In such cases, liabilities recognised in accordance with other Standards do not include refund obligations that apply in the event of a breach, unless the breach has occurred or is expected to occur. For example, a grant agreement may require the funds provided to an entity to be spent only in a particular period, failing which repayment to the grantor will be required. As the entity has the discretion whether to spend funds received in advance of the specified period, a refund liability is not recognised unless the entity breaches the condition or a breach is expected.

AASB 1058, paragraph B14Implications

Depending on whether NFPs use the full retrospective transition method or the modified retrospective method, balances of ‘deferred revenue’ at 1 January 2018/1 July 2018 for the full retrospective method, or 1 January 2019/1 July 2019 for the modified retrospective method, will need to be reassessed on those dates to determine if the ‘deferred revenue’ meets the requirements in AASB 15 of having an enforceable contract with a customer which includes ‘sufficiently specific’ performance obligations.

While the refund obligation may render the contract enforceable (AASB 15, Appendix F, paragraph F12(a)), it does not automatically mean that the contract contains ‘sufficiently specific’ performance obligations.

If there are no ‘sufficiently specific’ performance obligations, NFPs will need to make adjustments to derecognise deferred revenue on transition date. This could result in ‘lumpy’ profit or loss statements post 1 January 2019 where grant receipts are recognised as income under AASB 1058 in periods earlier than those when funds are spent.

Example 1 – No ‘sufficiently specific’ performance obligations

Fact pattern

Literacy NFP is given a three-year grant by the State Government to ‘improve literacy in the XYZ Community’.

Literacy NFP receives $1 million on 31 December 2019 in cash to cover the three-year contract period.

There are no conditions specified in the grant contract as to how Literacy NFP should spend the grant funds, other than the requirement to return any unspent funds at the end of the three-year contract, 31 December 2022.

The grant contract does not specify any particular tasks, goods or services that Literacy NFP needs to perform or deliver during the three-year contract period.

Question

Can Literacy NFP recognise the $1 million cash received on 31 December 2019 as deferred revenue?

Analysis

Using the decision tree above, Literacy NFP was not granted the funds for the purpose of constructing a non-financial asset.

Working down the left hand side of the decision tree, we then consider whether the grant transaction occurs in a contract that creates enforceable rights and obligations. AASB 15, Appendix F, paragraph F12(a) notes that an agreement is typically enforceable when the terms require a refund in cash when the agreed specific performance has not occurred. In this example, the contract requires Literacy NFP to refund any unspent funds to the State Government at the end of the contract period, therefore the contract as a whole is considered enforceable.

Continuing down the decision tree, we then assess whether the contract includes ‘sufficiently specific’ performance obligations whereby Literacy NFP is obligated to transfer goods or services to customers. Because the contract does not specify any goods or services to be transferred to customers, there are no ‘sufficiently specific’ performance obligations because it is not possible to determine WHEN THE PERFORMANCE OBLIGATION HAS BEEN SATISFIED.

- the nature or type of the goods or services;

- the cost or value of the goods or services;

- the quantity of the goods or services; and

- the period over which the goods or services must be transferred.

AASB 15, Appendix F, paragraph F20

Example 2– ‘Sufficiently specific’ performance obligations

Literacy NFP is given a three-year grant by the State Government to improve literacy in a community.

Literacy NFP receives $1 million on 31 December 2019 in cash, to cover the three-year contract.

Any unspent monies need to be refunded to State Government at the end of the three-year period.

The contract stipulates that the money must be used as follows:

- Employ 2 specialist teachers for the first year (FY20) to develop specialised reading programs for Years K-2 (cost of $200,000)

- Purchase special reading books and workbooks to use during lessons ($50,000 budgeted to be spent during FY20, $70,000 during FY21 and $80,000 during FY22)

- Employ 3 specialist teachers to be available three afternoons per week during school terms in FY21 and FY22 to run face-to-face teaching sessions at the XYZ primary School for all children from public schools in Suburb XYZ (cost of $100,000 per teacher per year, total of $600,000).

Question

Can Literacy NFP recognise the $1 million cash received on 31 December 2019 as deferred revenue?

Analysis

As per Example 1 above:

- Literacy NFP was not granted the funds for the purpose of constructing a non-financial asset

- The contact requires Literacy NFP to refund any unspent funds to the State Government at the end of the contract period, therefore the contract as a whole is considered enforceable.

Continuing down the decision tree, we then assess whether the contract includes ‘sufficiently specific’ performance obligations, whereby Literacy NFP is obligated to transfer goods or services to customers.

The requirement in the contract to employ 3 specialist teachers to be available three afternoons per week during school terms in FY21 and FY22 to run face-to-face teaching sessions could be considered ‘sufficiently specific’ performance obligations because it is possible to determine WHEN THESE PERFORMANCE OBLIGATIONS HAVE BEEN SATISFIED. That is, each week it is possible to determine if each of the three teachers taught a class three times.

It is important to note that the following tasks would not be considered ‘sufficiently specific’ performance obligations:

- The need to employ two specialist teachers for the first year (FY20) to develop the specialised reading programs which will be taught in Years 2 and 3, and

- The requirement to purchase special reading books and workbooks to use during lessons.

These requirements are merely types of activities that Literacy NFP must undertake to fulfil the contract and do not involve the transfer of any good or service to the customer (State Government).

Note: Having established that this contract contains sufficiently specific performance obligations, the cash received on 31 December 2019 will be recognised as a contract liability. As performance obligations (face to face teaching hours) are only delivered during Years 2 and 3 (FY21 and FY22), revenue will only be recognised during those years. No revenue will be recognised during the first year (FY20) because tasks undertaken to develop the training program and purchase materials did not result in any services being transferred to the customer (State Government).

Concluding thoughts

From 1 January 2019, NFPs will need to undergo a detailed review of all grant contracts to assess whether recognition under AASB 1058 or AASB 15 is appropriate. This is a difficult and time-consuming process and involves judgement. NFPs should not assume that revenue deferred under superseded standards will automatically qualify for deferral under AASB 15 simply because they include refund obligations.