Aletta Boshoff

Leader, IFRS & Corporate Reporting

Leader, Sustainability Reporting

Partner, Advisory

Leader, Sustainability Reporting

Partner, Advisory

From 1 January 2025, certain entities submitting financial reports to ASIC under Chapter 2M of the Corporations Act 2001 will be required to make mandatory climate disclosures.

Click to expand

Click to expand

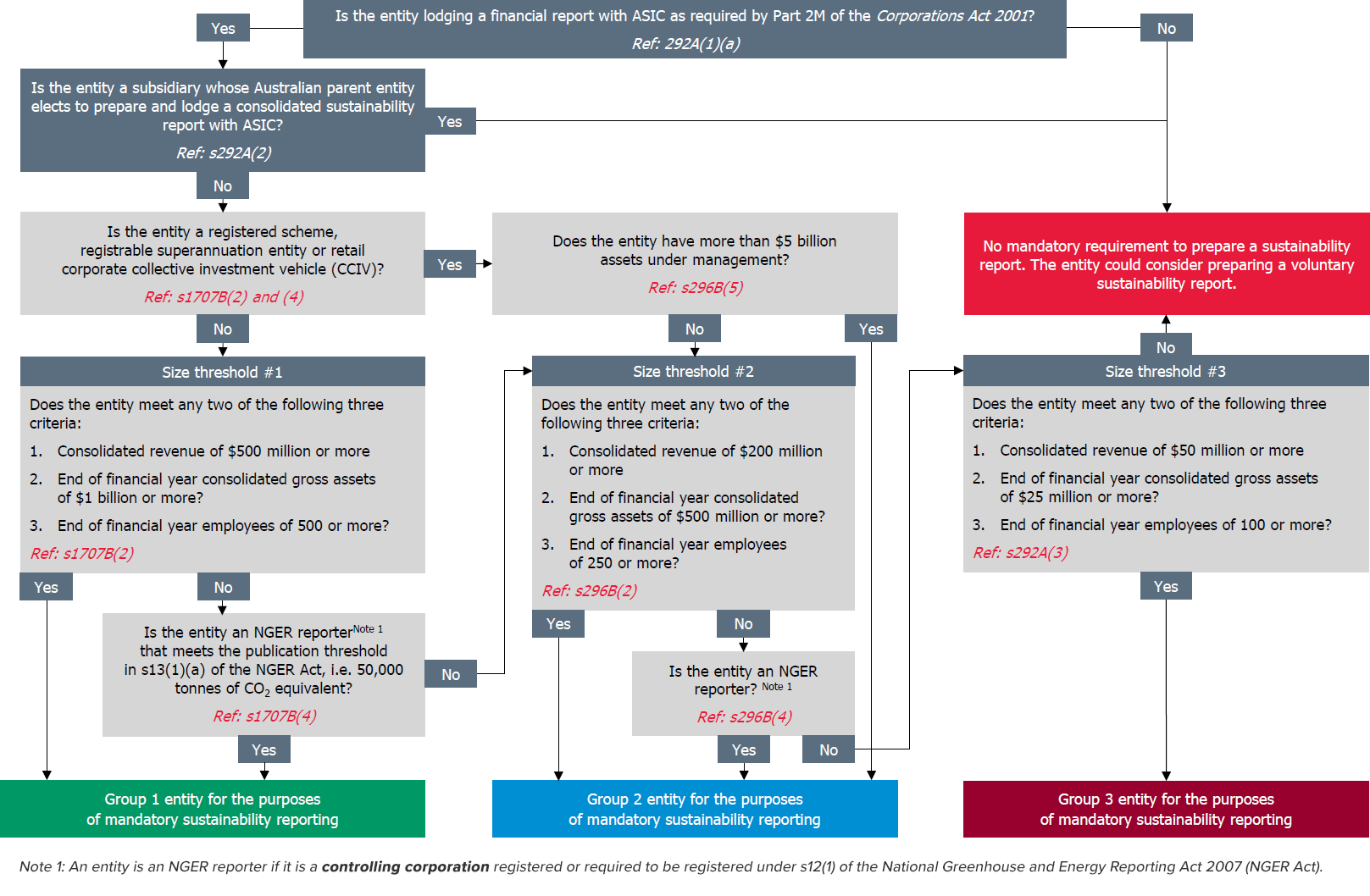

Australian entities required to prepare and lodge a financial report with the Australian Securities and Investments Commission (ASIC) under Chapter 2M of the Corporations Act 2001 must prepare a sustainability report if they meet certain criteria.

Our decision tree diagram will assist you in determining whether your entity is subject to mandatory sustainability reporting, and which of the three groups your entity falls into.

The Corporations Act 2001 outlines the start dates, based on the group your entity falls into:

The Australian Accounting Standards Board (AASB) has approved its first sustainability reporting standards, bringing climate reporting closer for Australian entities.

There are two new standards to be aware of:

Yes, an audit is required. Here’s what you need to know:

While the whole sustainability report must be audited for financial years beginning on or after 1 July 2030, there will be a phase-in period before this date during which different sections of the report will be subject to varying levels of assurance.

BDO and Chartered Accountants Australia and New Zealand (CA ANZ) have teamed up to create a practical roadmap for Groups 1, 2 and 3 entities. This guide helps finance professionals navigate the evolving landscape of climate-related financial disclosures in Australia.

Our TCFD checklist consolidates the 11 recommended disclosures and guidance for all sectors to help organisations perform a gap analysis as they embark on TCFD reporting. This resource covers key areas like governance, strategy, risk management and metrics, providing essential guidelines for effective climate-related financial disclosures.

This practical guide can help organisations develop a sustainability roadmap in six steps, including assessing, prioritising, committing, measuring, reporting, and improving business sustainability.

This sustainability report includes illustrations of the disclosure requirements of IFRS S1 and S2, however, this publication only addresses sustainability-related risks and opportunities relating to climate change, which are addressed by IFRS S2.

While mandatory sustainability reporting is on the horizon for some entities, many organisations are choosing to produce voluntary sustainability reports. This proactive approach reflects a commitment to transparency and continuous improvement.

Embarking on a voluntary sustainability reporting journey can be daunting, but breaking it down into manageable steps can make the process more achievable. For example:

We understand that navigating the new sustainability reporting legislation probably feels daunting. Determining which entities must report and by when may be a difficult and time-consuming exercise. Our expert sustainability reporting team is ready to guide you through the process and ensure your organisation meets all requirements.

Contact us

Contact our team to discuss your needs using the request for service form.

Alternatively, call 1300 138 991 to speak with an adviser in your nearest BDO office.

Aletta Boshoff

Kevin Frohbus

Tom Hogbin